Brazil’s residential real estate market stands at a pivotal moment in 2026. As monetary policy shifts and innovative financing models emerge, developers and homebuyers alike are witnessing a transformation that could reshape the nation’s housing landscape. The relationship between SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026 represents more than just economic data—it signals a fundamental change in how Brazilians access homeownership and how developers plan their construction pipelines. 🏗️

The Brazilian Central Bank’s management of the SELIC rate, combined with the growing adoption of fixed-rate mortgage products, has created unprecedented opportunities in the mid-tier housing segment. This convergence of favorable monetary conditions and financial innovation is driving a remarkable 14% expansion in mortgage credit availability, enabling developers to accelerate their residential projects with greater confidence than seen in recent years.

Key Takeaways

- SELIC rate stabilization at current levels creates predictable financing costs for both developers and homebuyers, reducing market uncertainty

- Fixed-rate mortgage adoption protects borrowers from interest rate volatility, expanding the pool of qualified buyers for new residential launches

- 14% credit expansion in mortgage lending enables developers to target mid-tier housing segments with accelerated construction timelines

- Developer confidence has increased significantly, with residential launches expected to surge as financing accessibility improves

- Market timing favors both investors and first-time buyers as the combination of stable rates and innovative financing creates optimal entry conditions

Understanding Brazil’s Current SELIC Rate Environment

The SELIC Rate Trajectory Through 2026

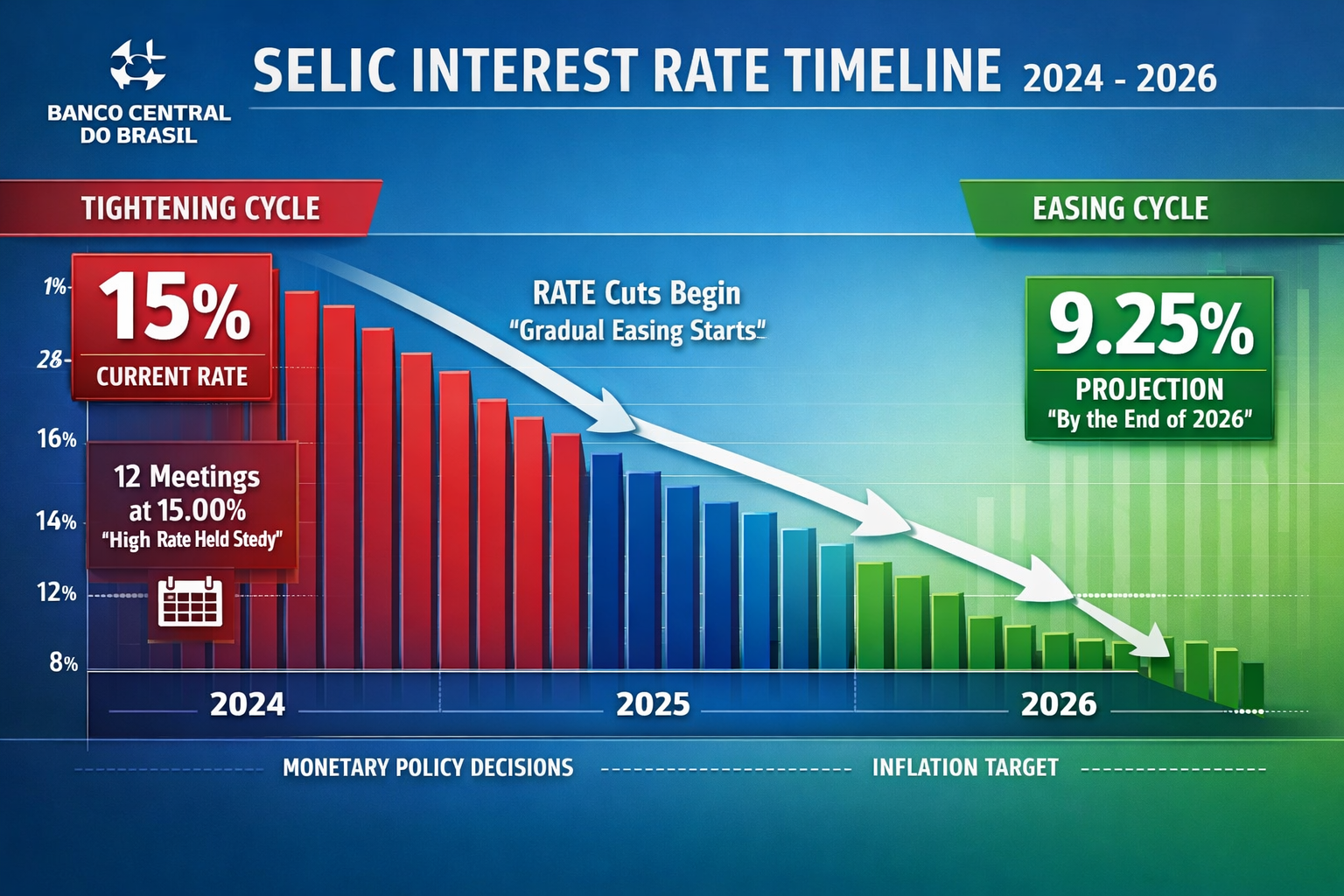

The SELIC rate stood at 15% per annum as of January 30, 2026, maintaining that level since June 2025.[1] This positioning reflects Brazil’s Central Bank strategy to manage inflationary pressures while supporting economic growth. Understanding this rate environment is crucial for anyone involved in Brazil’s property investment market.

Brazil’s central bank policy rate followed a tightening path in 2026, reversing part of the easing implemented in the previous two years.[2] This monetary policy adjustment has significant implications for residential development financing and consumer mortgage costs.

What Market Indicators Suggest for Future Rate Movements

Looking ahead to the Bank of Brazil’s March 2026 monetary policy meeting scheduled for March 16-17, market predictions reveal interesting sentiment. Current forecasts show a 77% probability of a SELIC rate decrease, 22.7% probability of no change, and less than 1% probability of an increase.[3]

This anticipated easing creates a favorable environment for the connection between SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026. As rates potentially decline toward the 9.25% range, the impact on mortgage affordability becomes substantial.

How SELIC Rates Impact Residential Development

The SELIC rate influences residential development through multiple channels:

- Construction financing costs: Lower rates reduce developer borrowing expenses

- Land acquisition leverage: More affordable capital for property purchases

- Project timeline decisions: Stable rates enable longer-term planning

- Profit margin calculations: Predictable interest environments improve feasibility studies

- Consumer purchasing power: Lower rates translate to affordable monthly payments

For developers operating in regions like Florianópolis, understanding these rate dynamics is essential for timing new launches and pricing strategies.

The Fixed-Rate Mortgage Revolution in Brazil

Traditional Variable-Rate vs. New Fixed-Rate Products

Historically, Brazilian mortgages have predominantly featured variable-rate structures tied to indices like the TR (Taxa Referencial) or IPCA (inflation index). These products exposed borrowers to significant payment uncertainty, particularly during periods of monetary tightening.

The emergence of fixed-rate mortgage products represents a paradigm shift in Brazil’s housing finance landscape. These products offer:

✅ Payment predictability throughout the loan term ✅ Protection against interest rate increases ✅ Simplified budgeting for household finances ✅ Reduced default risk during economic volatility ✅ Increased borrower confidence in long-term commitments

| Mortgage Type | Interest Rate Structure | Payment Stability | Inflation Protection | Typical Term |

|---|---|---|---|---|

| Traditional Variable | TR + spread (8-12%) | Low | Partial | 20-30 years |

| IPCA-Linked | IPCA + 3-6% | Moderate | Yes | 20-35 years |

| Fixed-Rate | 9-11% fixed | High | No | 15-25 years |

Why Fixed-Rate Mortgages Enable Credit Expansion

The relationship between SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026 becomes clear when examining lender behavior. Financial institutions can more accurately price risk with fixed-rate products, enabling them to:

- Expand lending portfolios with greater confidence

- Offer competitive rates to qualified borrowers

- Reduce provisioning requirements for potential defaults

- Securitize mortgage portfolios more effectively

- Attract institutional investors to housing finance

This 14% credit expansion isn’t merely about volume—it represents a qualitative improvement in mortgage accessibility for middle-income Brazilians who previously faced barriers to homeownership.

The Mid-Tier Housing Segment: Primary Beneficiary

The mid-tier housing segment, typically priced between R$300,000 and R$800,000, stands to benefit most from this financing transformation. These properties attract:

- First-time homebuyers transitioning from rental markets

- Young professionals with stable employment

- Growing families seeking larger living spaces

- Investors targeting rental income opportunities

Developers focusing on mid-tier residential projects can now plan launches with greater certainty about buyer financing availability, directly contributing to accelerated pipeline development.

How 14% Credit Expansion Transforms Developer Strategies

Accelerated Construction Timelines and Launch Schedules

With mortgage credit expanding by 14%, developers gain confidence to accelerate construction schedules and bring projects to market faster. This expansion affects multiple aspects of development strategy:

Pre-Launch Planning: Developers can now commit to projects earlier in the planning cycle, knowing that qualified buyers will have financing access when units become available.

Phased Development: Multi-phase projects become more viable as each phase’s success doesn’t depend on extraordinarily tight credit conditions.

Geographic Expansion: Developers can explore emerging markets and secondary cities where infrastructure development supports residential growth.

Targeting the Sweet Spot: Mid-Tier Residential Projects

The convergence of SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026 creates an optimal environment for mid-tier developments. These projects typically feature:

- 2-3 bedroom apartments ranging from 55-85 square meters

- Moderate amenities including fitness centers, co-working spaces, and leisure areas

- Strategic locations balancing accessibility and affordability

- Price points aligned with financing program limits

- Quality construction meeting modern building standards

Developers who position projects in this segment can capture demand from the expanded pool of mortgage-qualified buyers while maintaining healthy profit margins.

Risk Management in an Expanding Credit Environment

While credit expansion creates opportunities, sophisticated developers implement risk management strategies:

🛡️ Diversified buyer profiles: Targeting multiple demographic segments reduces concentration risk

🛡️ Flexible payment structures: Offering various down payment and installment options accommodates different buyer situations

🛡️ Strategic partnerships: Collaborating with multiple financial institutions ensures financing availability

🛡️ Market research: Continuous monitoring of absorption rates and buyer preferences guides project adjustments

🛡️ Contingency planning: Building flexibility into construction schedules accommodates potential market shifts

For investors considering pre-construction opportunities, understanding these developer strategies provides insight into project viability and potential returns.

Regional Market Dynamics: Where Growth Concentrates

São Paulo and Rio de Janeiro: Traditional Powerhouses

Brazil’s largest metropolitan areas continue dominating residential launches, but the relationship between SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026 affects these markets differently than emerging regions.

In São Paulo, the credit expansion enables:

- Vertical development in established neighborhoods

- Transit-oriented development projects

- Mixed-use complexes combining residential and commercial space

- Renovation and redevelopment of older properties

Rio de Janeiro sees opportunities in:

- Coastal neighborhood redevelopment

- Suburban expansion along transit corridors

- Affordable housing in peripheral districts

- Tourism-adjacent residential projects

Emerging Markets: Florianópolis and Secondary Cities

Secondary cities experience disproportionate benefits from improved mortgage accessibility. Florianópolis, in particular, demonstrates strong growth dynamics driven by:

- Quality of life factors attracting remote workers and retirees

- Technology sector growth creating high-income employment

- Tourism infrastructure supporting seasonal and permanent residents

- Educational institutions generating student housing demand

- Natural amenities commanding premium pricing for well-located properties

Other emerging markets benefiting from credit expansion include Curitiba, Belo Horizonte, Porto Alegre, and Brasília—each with unique demand drivers but all sharing improved financing accessibility.

Infrastructure Development as a Catalyst

The relationship between infrastructure investment and residential development cannot be overstated. Credit expansion enables developers to pursue projects in areas where:

- New transit lines improve accessibility

- Commercial development creates employment centers

- Educational facilities attract families

- Healthcare infrastructure serves growing populations

- Retail and entertainment enhance livability

These infrastructure catalysts, combined with favorable financing conditions, create high-return investment opportunities for those who identify emerging neighborhoods early.

Buyer Demographics and Changing Demand Patterns

First-Time Homebuyers: The Primary Growth Segment

Fixed-rate mortgages particularly benefit first-time homebuyers who previously faced barriers including:

- Payment uncertainty with variable-rate products

- Qualification challenges during high-interest environments

- Limited financial literacy regarding mortgage products

- Risk aversion preventing long-term commitments

The 14% credit expansion directly addresses these barriers, expanding the first-time buyer pool significantly. These buyers typically seek:

- Turnkey properties requiring minimal additional investment

- Established neighborhoods with proven infrastructure

- Proximity to employment minimizing commute times

- Future appreciation potential building long-term wealth

- Community amenities enhancing quality of life

Investors and Second-Home Buyers

Beyond primary residence seekers, the favorable financing environment attracts investors pursuing:

Rental Income Strategies: Fixed-rate mortgages enable precise cash flow calculations, making studio apartments and small units attractive for rental portfolios.

Vacation Properties: Coastal and resort markets benefit from buyers financing second homes with predictable payments.

Portfolio Diversification: Real estate becomes more accessible for investors seeking alternatives to equities and fixed income.

Retirement Planning: Pre-retirees invest in properties they’ll occupy later while generating rental income in the interim.

Demographic Shifts Driving Long-Term Demand

Several demographic trends reinforce the positive outlook for residential launches:

- Urbanization: Continued migration to cities creates structural housing demand

- Household formation: Younger generations establishing independent households

- Remote work adoption: Geographic flexibility enabling lifestyle-driven location choices

- Aging population: Demand for accessible, amenity-rich properties

- Income growth: Expanding middle class with homeownership aspirations

Financial Institutions and Mortgage Product Innovation

Banks Competing for Market Share

The 14% credit expansion reflects competitive dynamics among Brazilian financial institutions. Major banks including Caixa Econômica Federal, Banco do Brasil, Itaú, Bradesco, and Santander are:

- Developing new fixed-rate products with competitive terms

- Streamlining approval processes to capture market share

- Investing in digital platforms for faster loan processing

- Partnering with developers for exclusive financing arrangements

- Offering promotional rates to attract qualified borrowers

This competition benefits consumers through improved terms and accelerated approval timelines.

Government Programs Supporting Homeownership

Government initiatives complement private sector lending through:

Minha Casa, Minha Vida: Subsidized financing for low and middle-income families, expanding access to homeownership for previously excluded segments.

FGTS (Fundo de Garantia do Tempo de Serviço): Enabling workers to use employment fund balances for down payments and loan payments, reducing upfront capital requirements.

Tax Incentives: Deductions and benefits for homeowners and developers meeting specific criteria, improving project economics.

These programs work synergistically with the private mortgage market, amplifying the impact of the 14% credit expansion.

Technology and Digital Mortgage Platforms

Financial technology innovations accelerate mortgage processing through:

- Automated underwriting: AI-driven credit analysis reducing approval times

- Digital documentation: Paperless applications improving efficiency

- Blockchain verification: Secure property title and identity confirmation

- Mobile applications: Convenient access to mortgage management tools

- Integrated platforms: Seamless connections between buyers, developers, and lenders

These technological advances complement the favorable rate environment, making the connection between SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026 even more powerful.

Investment Considerations for 2026 and Beyond

Timing the Market: Current Opportunities

The current environment presents compelling opportunities for multiple investor types:

Pre-Construction Investors: Purchasing units during early launch phases captures maximum appreciation potential as projects progress toward completion.

Value Investors: Identifying underpriced properties in emerging neighborhoods before infrastructure improvements drive values higher.

Income Investors: Acquiring rental properties with favorable financing terms generating positive cash flow from day one.

Development Partners: Participating in joint ventures with established developers leveraging industry expertise and market access.

Risk Factors to Monitor

Despite favorable conditions, prudent investors monitor potential risks:

⚠️ Interest rate volatility: While trends suggest stabilization, unexpected economic shocks could alter the trajectory

⚠️ Regulatory changes: Government policy shifts affecting mortgage programs or real estate taxation

⚠️ Economic conditions: Employment trends and income growth supporting continued housing demand

⚠️ Supply dynamics: Oversupply in specific segments or locations creating downward price pressure

⚠️ Construction costs: Material and labor inflation affecting project economics

Due Diligence Best Practices

Successful investors implement thorough due diligence processes:

- Developer track record: Research completion history, financial stability, and reputation

- Location analysis: Evaluate infrastructure, amenities, and growth catalysts

- Comparative market analysis: Assess pricing relative to comparable properties

- Legal verification: Confirm clear title, proper permits, and regulatory compliance

- Financial modeling: Project cash flows, appreciation, and total returns under various scenarios

Working with experienced real estate professionals who understand local market dynamics significantly improves investment outcomes.

Developer Perspectives: Capitalizing on Market Conditions

Project Selection and Feasibility Analysis

Developers evaluating new projects in the context of SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026 focus on:

Market Demand Assessment: Analyzing demographic trends, employment growth, and buyer preferences to identify underserved segments.

Financial Feasibility: Modeling project economics under various interest rate and absorption scenarios to ensure viability.

Competitive Positioning: Differentiating projects through location, design, amenities, or pricing strategies.

Financing Structure: Securing construction financing at favorable terms while the rate environment remains supportive.

Exit Strategy: Planning for unit sales, portfolio retention, or project refinancing based on market conditions.

Marketing and Sales Strategies

Effective marketing in an expanding credit environment emphasizes:

- Financing partnerships: Highlighting preferred lender relationships offering competitive rates

- Payment flexibility: Structuring down payment and installment options accommodating various buyer situations

- Value proposition: Communicating location benefits, design quality, and lifestyle advantages

- Digital presence: Leveraging online platforms for virtual tours and remote sales processes

- Community building: Creating buyer communities fostering word-of-mouth referrals

Construction and Delivery Excellence

Developer reputation depends heavily on execution quality:

✨ Timeline adherence: Meeting promised delivery dates builds trust and supports future sales

✨ Quality standards: Exceeding buyer expectations creates positive reviews and referrals

✨ Communication: Regular updates keeping buyers informed throughout construction

✨ Warranty support: Responsive post-delivery service addressing any issues promptly

✨ Community activation: Facilitating resident integration and community development

Projects like Tramonto and Solis demonstrate these principles in action, building developer credibility in competitive markets.

Economic Outlook and Long-Term Projections

Macroeconomic Factors Supporting Continued Growth

Several macroeconomic trends support optimism about Brazil’s residential market:

GDP Growth: Economic expansion creating employment and income growth supporting housing demand.

Inflation Management: Central Bank credibility maintaining price stability and enabling lower interest rates.

Foreign Investment: International capital flows seeking emerging market real estate opportunities.

Commodity Prices: Brazil’s export strength supporting currency stability and economic confidence.

Political Stability: Predictable policy environment encouraging long-term investment planning.

Potential Scenarios Through 2027-2028

Projecting forward, several scenarios merit consideration:

Base Case (60% probability): SELIC gradually declines to 8-9% range, credit expansion continues at 10-15% annually, residential launches increase 20-25% compared to 2025 levels.

Optimistic Case (25% probability): Aggressive monetary easing drives SELIC below 8%, credit expansion accelerates to 18-20%, residential launches surge 30-35% with broad-based demand.

Pessimistic Case (15% probability): External shocks or domestic policy errors force SELIC increases back toward 12-13%, credit growth slows to 5-8%, residential launches stagnate or decline modestly.

Positioning for Multiple Scenarios

Sophisticated investors and developers position portfolios to perform across scenarios:

- Geographic diversification: Exposure to multiple markets reducing concentration risk

- Product diversification: Mix of price points and property types serving different demand segments

- Financial flexibility: Conservative leverage maintaining capacity to capitalize on opportunities

- Strategic partnerships: Relationships enabling rapid response to changing conditions

- Continuous monitoring: Regular market assessment informing tactical adjustments

Conclusion: Seizing the Moment in Brazil’s Residential Market

The convergence of SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026 represents a generational opportunity in Brazil’s residential real estate market. The stabilization of interest rates, combined with innovative fixed-rate mortgage products, has fundamentally altered the accessibility of homeownership for millions of Brazilians while enabling developers to pursue ambitious construction pipelines with greater confidence.

For homebuyers, this environment offers unprecedented payment predictability and financing accessibility, making the dream of homeownership more attainable than in recent memory. First-time buyers particularly benefit from the expansion of mortgage credit and the protection that fixed-rate products provide against future interest rate uncertainty.

For investors, the combination of favorable financing conditions, expanding demand, and accelerating residential launches creates multiple pathways to attractive returns—whether through pre-construction purchases, rental income strategies, or value-oriented acquisitions in emerging neighborhoods.

For developers, the 14% credit expansion enables accelerated project timelines, reduced market risk, and improved unit absorption rates, particularly in the mid-tier housing segment that serves Brazil’s growing middle class.

Actionable Next Steps

If you’re a prospective homebuyer:

- Get pre-qualified for a fixed-rate mortgage to understand your purchasing power

- Research emerging neighborhoods offering value and growth potential

- Attend developer presentations for upcoming launches in your target areas

- Work with experienced real estate professionals who understand local market dynamics

- Act decisively when you identify properties meeting your criteria—favorable conditions attract competition

If you’re an investor:

- Evaluate pre-construction opportunities in markets with strong growth catalysts

- Analyze cash flow potential for rental income strategies

- Diversify across multiple properties and locations to manage risk

- Establish relationships with reputable developers and financing partners

- Monitor market indicators to time additional acquisitions strategically

If you’re a developer:

- Accelerate feasibility studies for projects in the mid-tier housing segment

- Secure construction financing while rates remain favorable

- Establish partnerships with financial institutions offering competitive mortgage products

- Invest in marketing and sales infrastructure to capitalize on expanding buyer pools

- Focus on execution excellence to build reputation and support future launches

The window of opportunity created by current monetary conditions and financial innovation won’t remain open indefinitely. Those who recognize the significance of SELIC at 9.25% and Fixed-Rate Mortgages: 14% Credit Expansion Boosting Brazil Residential Launches in 2026 and take decisive action will position themselves advantageously in Brazil’s evolving residential landscape.

Explore current residential projects and contact experienced developers to learn how you can participate in this transformative moment in Brazilian real estate. The combination of stable interest rates, innovative financing, and expanding credit access creates conditions that favor both first-time buyers and seasoned investors—making 2026 a pivotal year for Brazil’s residential market. 🏡

References

[1] 30012026 Brazils Central Bank Keeps Benchmark Interest Rate At 15 Per Annum – https://www.eurasiareview.com/30012026-brazils-central-bank-keeps-benchmark-interest-rate-at-15-per-annum/

[2] Brazil Central Bank Policy Rate Monthly – https://www.statista.com/statistics/1643371/brazil-central-bank-policy-rate-monthly/

[3] Bank Of Brazil Decision In March – https://polymarket.com/event/bank-of-brazil-decision-in-march