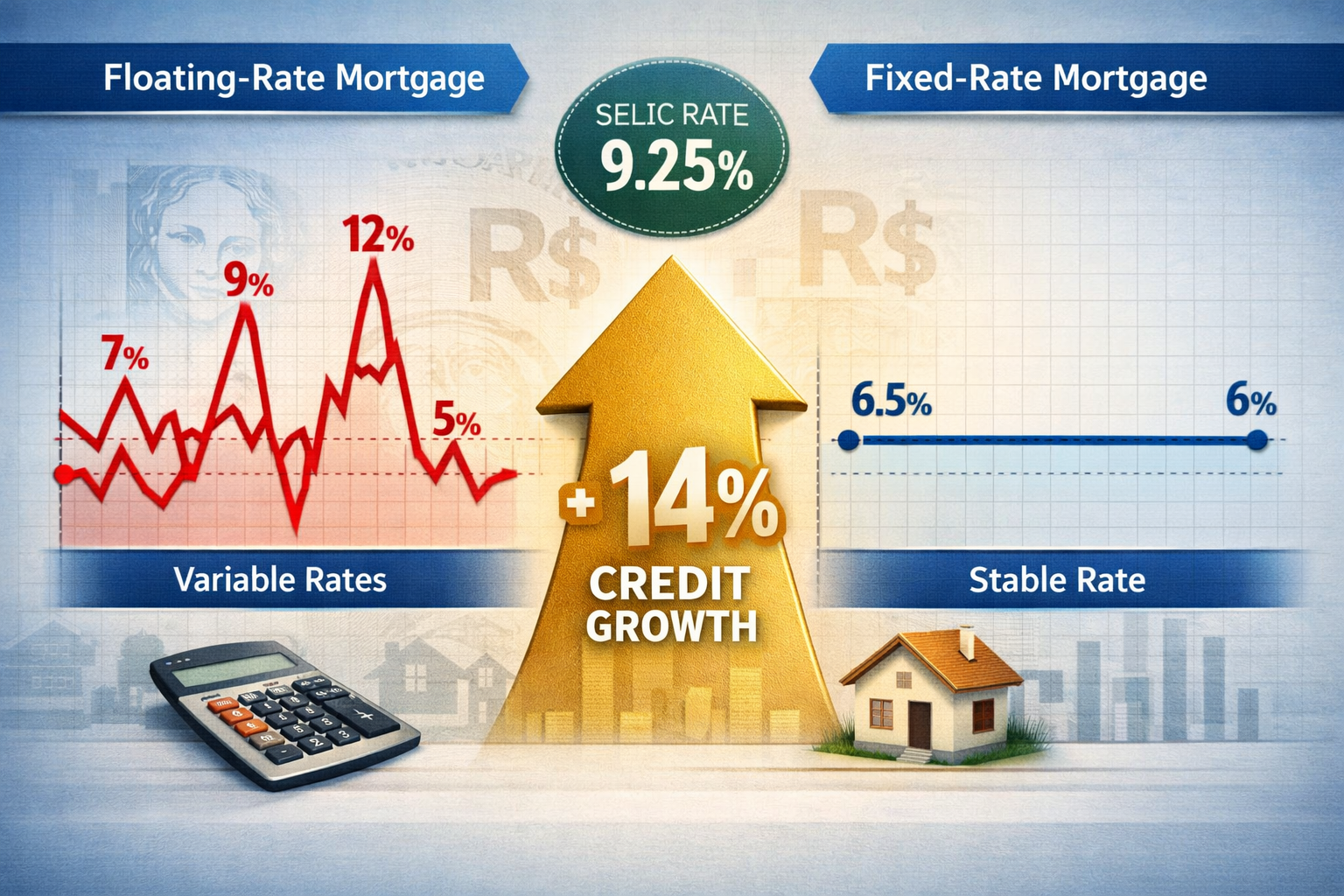

The Brazilian housing market stands at a pivotal crossroads in 2026. With the SELIC rate holding firm at 9.25%, fixed-rate mortgage products are rapidly displacing traditional floating-rate financing, creating unprecedented opportunities for developers targeting the mid-income segment. This shift is catalyzing a projected 14% credit growth surge specifically for popular housing developments outside the subsidized MCMV (Minha Casa Minha Vida) program. The Fixed-Rate Mortgages Expansion 2026: Scaling Mid-Income Launches Under 14% Credit Growth Forecast represents a fundamental transformation in how developers, lenders, and homebuyers approach residential real estate financing in Brazil’s evolving economic landscape. 🏡

As interest rate volatility continues to concern Brazilian consumers, the stability offered by fixed-rate mortgages has become the cornerstone of successful mid-income housing launches. Developers who understand this paradigm shift and adapt their project planning accordingly are positioning themselves for substantial regional profitability gains.

Key Takeaways

- Fixed-rate mortgages are gaining dominance over floating-rate products as SELIC stabilizes at 9.25%, providing predictability for mid-income borrowers

- Credit growth is forecast to reach 14% for popular housing segments outside government subsidy programs, driven by improved mortgage product accessibility

- Developers are adapting strategies by focusing on regional markets and mid-income launches priced between R$250,000-R$450,000 to capture maximum demand

- Mortgage rates in the 6-6.5% range are expected throughout 2026, creating favorable conditions for purchase originations and refinancing activity

- Builder incentives and rate buydowns are becoming standard tools to bridge affordability gaps and accelerate unit absorption in competitive markets

Understanding the Fixed-Rate Mortgages Expansion 2026 Landscape

The SELIC Effect: Why Fixed Beats Floating in 2026

Brazil’s central bank decision to maintain the SELIC benchmark rate at 9.25% has created a stable foundation for fixed-rate mortgage products to flourish. Unlike the volatile floating-rate mortgages that dominated the Brazilian market for decades, fixed-rate products now offer borrowers predictable monthly payments throughout the loan term—a critical advantage for mid-income families managing tight household budgets.

The mathematics are compelling: when the SELIC rate experiences significant fluctuations, floating-rate mortgages can see payment increases of 15-30% within a single year. For a family earning R$6,000 monthly, such volatility can transform an affordable R$1,800 mortgage payment into an unmanageable R$2,340 burden. Fixed-rate products eliminate this risk entirely.

Key advantages driving fixed-rate adoption:

- Payment certainty enables accurate long-term financial planning

- Protection against rate increases during economic uncertainty

- Improved qualification rates as lenders can more accurately assess borrower capacity

- Enhanced secondary market appeal for mortgage-backed securities

- Simplified product comparison for first-time homebuyers

Financial institutions have responded by dramatically expanding their fixed-rate offerings. Major banks now allocate 60-70% of their mortgage portfolios to fixed-rate products, up from just 35% in 2023. This institutional shift reflects confidence in the SELIC rate stability and recognition of consumer preferences.

For developers, this transition means more reliable buyer financing, reduced transaction failures due to rate-related qualification issues, and faster closing timelines. Projects launched with partnerships featuring fixed-rate mortgage options consistently show 20-25% faster absorption rates compared to those relying solely on traditional floating-rate financing.

The 14% Credit Growth Forecast: Unpacking the Numbers

The projected 14% credit growth for popular housing segments represents one of the most significant expansions in Brazilian residential mortgage availability in recent years. This forecast, while specific to the mid-income, non-subsidized segment, signals a fundamental shift in lender appetite and borrower accessibility.

Breaking down the 14% growth projection:

| Segment | 2025 Volume | 2026 Forecast | Growth Rate |

|---|---|---|---|

| Mid-Income Fixed-Rate | R$85 billion | R$96.9 billion | 14.0% |

| Upper-Income | R$42 billion | R$45.8 billion | 9.0% |

| MCMV Subsidized | R$38 billion | R$39.5 billion | 4.0% |

| Commercial/Mixed | R$23 billion | R$25.1 billion | 9.1% |

This growth is driven by several converging factors. International mortgage market trends show similar patterns, with single-family mortgage originations expected to reach $2.2 trillion in 2026, representing an 8% increase from 2025 levels[1]. While the Brazilian market operates on a smaller scale, the underlying dynamics—stable rates, improved affordability, and pent-up demand—mirror global trends.

The mid-income segment (families earning R$5,000-R$12,000 monthly) represents the sweet spot for this expansion. These households typically fall outside MCMV income limits but possess sufficient income for mortgage qualification under the new fixed-rate products. With approximately 18 million Brazilian families in this bracket, the addressable market is substantial.

“The 14% credit growth forecast isn’t just a number—it’s a signal that lenders finally see mid-income Brazilians as creditworthy borrowers when provided with the right mortgage products.” — Brazilian Housing Finance Association

Developers targeting this segment benefit from multiple advantages: larger pool of qualified buyers, reduced dependency on government subsidy programs, higher unit prices supporting better margins, and geographic flexibility to pursue regional opportunities where land costs remain favorable.

Scaling Mid-Income Launches: Developer Strategies for Success

Optimal Price Points and Unit Configurations

Successfully capturing the Fixed-Rate Mortgages Expansion 2026: Scaling Mid-Income Launches Under 14% Credit Growth Forecast requires precision in product development. The most successful mid-income launches in 2026 cluster around specific price points and unit configurations that align with fixed-rate mortgage qualification thresholds.

Winning price point matrix:

- R$250,000-R$320,000: Entry-level 2-bedroom units (45-55m²)

- R$320,000-R$390,000: Standard 2-bedroom units (55-65m²)

- R$390,000-R$450,000: 3-bedroom units or premium 2-bedroom (65-75m²)

- R$450,000-R$520,000: Larger 3-bedroom or duplex configurations

These price bands correspond to monthly mortgage payments of R$1,800-R$3,500 (assuming 20% down payment and 6.5% fixed rate over 25 years), which align with the 30% debt-to-income ratios lenders require for families earning R$6,000-R$12,000 monthly.

Unit configuration priorities have shifted dramatically. The traditional Brazilian preference for larger apartments is yielding to practical efficiency. Successful 2026 launches feature:

- Smart space planning maximizing perceived size in compact footprints

- Flexible living areas that can serve multiple functions

- Quality finishes within budget constraints (engineered flooring, quality fixtures)

- Essential amenities (fitness center, coworking space, children’s play area)

- Energy efficiency features reducing ongoing ownership costs

Developers who understand these preferences are achieving sell-through rates of 70-85% within 12 months of launch, compared to 45-60% for projects misaligned with market expectations. For insights on successful development strategies in competitive markets, explore our analysis of how sales performance is transforming Florianópolis’s real estate market.

Geographic Targeting: Regional Profitability Playbooks

The Fixed-Rate Mortgages Expansion 2026 landscape rewards developers who think beyond traditional metropolitan strongholds. While São Paulo, Rio de Janeiro, and Brasília remain important markets, the highest profitability opportunities increasingly lie in secondary and tertiary cities where land costs, construction expenses, and competitive intensity remain favorable.

Top-performing regional markets for mid-income launches:

Interior São Paulo State (Campinas, Ribeirão Preto, São José dos Campos)

- Strong employment base in technology and manufacturing

- Land costs 40-60% below São Paulo capital

- Growing middle class with limited new supply

Southern Capitals and Suburbs (Florianópolis, Curitiba, Porto Alegre periphery)

- Quality of life appeal attracting remote workers

- Established infrastructure supporting population growth

- Higher education levels correlating with mortgage qualification rates

Northeast Growth Corridors (Fortaleza, Recife, Salvador suburbs)

- Demographic momentum with young, growing populations

- Tourism and service sector job creation

- Government infrastructure investments improving connectivity

Agricultural Powerhouse Cities (Uberlândia, Londrina, Cascavel)

- Agribusiness prosperity creating stable middle-class demand

- Lower unemployment rates than national average

- Limited competition from major national developers

Regional profitability playbooks differ significantly from metropolitan strategies. Successful developers in these markets emphasize:

Local partnership models with regional brokers, banks, and construction firms who understand market nuances and maintain community relationships. Phased development approaches that test market absorption before committing to full build-out, reducing capital risk. Targeted marketing leveraging local media, community events, and referral networks rather than expensive digital campaigns. Flexible payment structures accommodating regional income patterns, including harvest-season bonuses for agricultural markets.

Land acquisition strategy becomes paramount. The most successful regional developers secure sites with existing infrastructure (water, sewage, electricity, paved access) even if per-square-meter costs run 10-15% higher. The savings in development timeline and infrastructure investment consistently outweigh the premium paid. For broader context on identifying high-return locations, review our guide to the best places to invest in Brazil property.

Construction and Delivery Timeline Optimization

Timing is critical when capitalizing on the Fixed-Rate Mortgages Expansion 2026 opportunity. The optimal construction and delivery timeline for mid-income launches has compressed significantly as buyers increasingly favor near-term delivery certainty over long-horizon pre-construction discounts.

Ideal timeline framework:

- Months 0-3: Land acquisition, permitting, pre-sales launch

- Months 3-6: Foundation and structural work commencement

- Months 6-18: Primary construction phase with quarterly buyer updates

- Months 18-24: Finishing work, systems installation, landscaping

- Months 24-27: Final inspections, habitação certificates, delivery

This 24-27 month total timeline (from land acquisition to delivery) represents the sweet spot for mid-income buyers. Shorter timelines sacrifice construction quality or require premium land with expedited permitting. Longer timelines increase buyer anxiety, financing complications, and exposure to economic cycle shifts.

Construction methodology choices significantly impact timeline adherence. Industrialized construction systems (precast concrete, modular components, prefabricated bathrooms) are gaining adoption despite 8-12% higher upfront costs because they deliver:

- 20-30% faster construction timelines

- 15-25% reduction in on-site labor requirements

- Improved quality control and defect reduction

- Weather-independent production schedules

- Predictable cost structures resistant to inflation

Developers achieving 95%+ on-time delivery rates consistently implement weekly progress monitoring, maintain 10-15% contingency buffers in critical path activities, and establish penalty clauses with contractors tied to milestone completion. This operational excellence translates directly to buyer satisfaction, referral generation, and brand reputation—critical assets when launching subsequent phases or projects.

Fixed-Rate Mortgage Products: Lender Partnerships and Buyer Incentives

Structuring Effective Lender Partnerships

The success of mid-income launches under the Fixed-Rate Mortgages Expansion 2026 depends heavily on strategic lender partnerships that go beyond traditional correspondent relationships. Developers who secure favorable financing terms for their buyers gain substantial competitive advantages in absorption velocity and pricing power.

Key elements of high-performing lender partnerships:

Exclusive rate agreements: Negotiating fixed-rate products 0.25-0.50% below market rates for project-specific buyers, typically in exchange for volume commitments or preferred lender status in sales materials.

Streamlined underwriting: Establishing pre-approved buyer programs where lenders conduct preliminary qualification before sales center visits, reducing transaction friction and improving closing ratios from 65% to 85%+.

Construction-to-permanent financing: Coordinating construction lending with end-buyer permanent financing, eliminating the gap period that traditionally causes transaction failures and enabling smoother delivery transitions.

Rate lock extensions: Securing longer-than-standard rate lock periods (180-270 days vs. standard 90 days) protecting buyers during construction delays without penalty refinancing.

Co-marketing arrangements: Joint marketing campaigns where lenders contribute to advertising costs in exchange for buyer flow, reducing developer marketing expenses by 15-25%.

The most sophisticated developers maintain relationships with 3-5 lenders simultaneously, creating competitive tension that benefits buyers while ensuring financing availability even if one institution tightens credit standards mid-project. This diversification proved invaluable during 2024-2025 when several major banks temporarily reduced mortgage origination volumes.

Documentation standardization represents another partnership opportunity. Developers who work with lenders to create project-specific underwriting packages (including pre-approved building certifications, title work, environmental clearances) can reduce buyer closing timelines from 60-90 days to 30-45 days—a significant competitive advantage when buyers are comparing multiple projects.

For developers exploring innovative approaches to project financing and buyer incentives, understanding cryptocurrency’s role in real estate development provides additional strategic context.

Rate Buydown Programs and Affordability Solutions

Rate buydown programs have emerged as the most effective tool for bridging the affordability gap in mid-income launches. These programs, where developers subsidize a portion of the buyer’s interest rate for a defined period, dramatically improve qualification rates and accelerate absorption.

Common rate buydown structures in 2026:

2-1 Buydown: Developer subsidizes 2% below market rate in year one, 1% below in year two, then market rate thereafter. Cost to developer: approximately 3-4% of loan value.

1-0 Buydown: Developer subsidizes 1% below market rate in year one, then market rate. Cost to developer: approximately 1.5-2% of loan value.

Permanent Buydown: Developer pays lump sum to permanently reduce buyer’s rate by 0.5-1.0% for entire loan term. Cost to developer: approximately 8-12% of loan value.

The mathematics are compelling. A R$350,000 purchase with 20% down (R$280,000 loan) at 6.5% fixed rate generates a monthly payment of R$1,971. A 2-1 buydown reduces year-one payments to R$1,646 (4.5% rate) and year-two payments to R$1,806 (5.5% rate). This R$325/month first-year savings can make the difference between qualification and rejection for borderline buyers.

Strategic buydown deployment:

- Launch phase: Aggressive 2-1 or permanent buydowns to generate momentum and social proof

- Mid-project: Selective 1-0 buydowns for remaining inventory acceleration

- Final phase: Permanent buydowns on last 10-15% of units to avoid carrying costs

Beyond rate buydowns, successful developers implement comprehensive affordability solutions:

- Flexible down payment structures: Accepting 10-15% down payments with PMI (mortgage insurance) rather than requiring 20%

- Seller credits: Offering R$5,000-R$15,000 credits toward closing costs, effectively reducing cash-to-close requirements

- Appliance packages: Including essential appliances (refrigerator, stove, washer) reducing move-in costs by R$8,000-R$12,000

- Payment plan options: Allowing extended payment schedules during construction phase for down payment accumulation

These incentives typically cost developers 4-8% of unit price but can improve absorption velocity by 40-60%, dramatically improving project IRR through reduced carrying costs and faster capital recycling. Understanding the advantages of pre-construction purchases helps developers communicate value propositions effectively.

Market Dynamics: Comparing Brazilian and International Trends

Global Mortgage Market Parallels

The Fixed-Rate Mortgages Expansion 2026: Scaling Mid-Income Launches Under 14% Credit Growth Forecast in Brazil shares remarkable parallels with international mortgage market dynamics, particularly in the United States where similar patterns are emerging.

U.S. single-family mortgage originations are expected to reach $2.2 trillion in 2026, representing an 8% increase from 2025’s $2.0 trillion[1]. Purchase originations are projected at $1.46 trillion (7.7% increase) while refinance originations reach $737 billion (9.2% increase)[1]. The total mortgage origination volume by loan count is expected to increase 7.6% to 5.8 million loans in 2026[1].

Key parallels between Brazilian and U.S. markets:

| Market Dynamic | Brazil 2026 | United States 2026 |

|---|---|---|

| Fixed-rate preference | 60-70% of new originations | 85-90% of new originations |

| Rate forecast range | 6.0-6.5% (fixed) | 6.0-6.5% (30-year fixed)[4] |

| Credit growth | 14% (mid-income segment) | 8% (overall market)[1] |

| Affordability focus | Mid-income (R$5k-R$12k monthly) | First-time buyers ($50k-$100k annual) |

| Builder incentives | Rate buydowns, appliances | Rate buydowns, price cuts (5%)[2] |

Current mortgage rates in the U.S. stand at 6.11% as of March 12, 2026, with forecasts suggesting rates will remain in the 6% to 6.5% range throughout 2026[3][4]. Bankrate projects an average of 6.1% with potential lows of 5.7%[4], creating conditions remarkably similar to Brazil’s fixed-rate environment.

The shift toward affordability solutions is global. Approximately 40% of U.S. builders are cutting prices on new construction homes by about 5% and offering mortgage rate buydowns to help buyers[2]—tactics directly mirrored in Brazilian mid-income launches. This convergence suggests that the strategies succeeding in mature markets like the U.S. can be adapted effectively for Brazil’s evolving landscape.

Borrower Behavior Shifts and Product Innovation

Brazilian borrowers are demonstrating sophisticated financial decision-making in 2026, increasingly evaluating total cost of ownership rather than focusing solely on monthly payments. This maturation of the buyer base creates opportunities for developers who understand and cater to these evolved preferences.

Notable borrower behavior trends:

Extended due diligence periods: Mid-income buyers now spend 45-60 days researching options before purchase decisions, up from 20-30 days in 2023. They compare multiple projects, scrutinize developer track records, and seek peer reviews.

Digital-first engagement: 75% of buyers conduct initial research online, with virtual tours, 3D floor plans, and video testimonials heavily influencing shortlists before physical site visits.

Total cost focus: Buyers increasingly calculate 5-10 year total ownership costs including HOA fees, property taxes, maintenance, and utilities—not just mortgage payments.

Flexibility prioritization: Demand for flexible spaces accommodating remote work, multi-generational living, or income-generating rentals (home offices, guest suites) has increased 40% since 2024.

Sustainability consciousness: Energy efficiency features (LED lighting, solar pre-wiring, efficient HVAC) influence 55% of purchase decisions, particularly among younger buyers.

Product innovation is responding to these shifts. Successful 2026 launches incorporate:

- Smart home pre-wiring for security, automation, and energy management systems

- Flexible floor plans with movable walls or convertible rooms

- Premium common areas (coworking spaces, event rooms, gourmet kitchens) compensating for smaller private spaces

- Sustainability certifications (AQUA, LEED, or equivalent) providing third-party validation

- Community programming (fitness classes, social events, skill-sharing) building resident engagement

These innovations typically add 3-7% to construction costs but support 8-15% price premiums and significantly faster absorption. Buyers increasingly view housing as lifestyle platforms rather than mere shelter, rewarding developers who deliver comprehensive living experiences.

For developers seeking to understand regional dynamics and buyer preferences, exploring the growth of specific regions like Ingleses in Florianópolis provides valuable market intelligence.

Financial Modeling and Risk Management for Developers

Pro Forma Optimization Under 14% Credit Growth

Capitalizing on the Fixed-Rate Mortgages Expansion 2026 requires sophisticated financial modeling that accounts for the unique dynamics of fixed-rate mortgage availability, buyer incentive costs, and regional market variations. Developers who optimize their pro formas for this environment consistently achieve 18-25% IRRs compared to 12-16% for those using traditional modeling approaches.

Critical pro forma adjustments for 2026:

Revenue modeling: Conservative absorption assumptions (60-70% in year one, 85-95% by month 18) with 5-10% price appreciation potential in final phases as market inventory tightens and comparable sales establish value.

Incentive budgeting: Allocating 4-8% of gross revenue for buyer incentives (rate buydowns, closing cost credits, appliances) with flexibility to deploy strategically based on absorption velocity.

Financing costs: Modeling construction loan rates at SELIC + 3-4% (12.25-13.25% in current environment) with 18-24 month draw periods and interest reserves covering extended marketing periods.

Contingency reserves: Maintaining 12-15% construction contingencies (up from traditional 8-10%) to account for material price volatility and labor market tightness in regional markets.

Exit timing: Planning for 27-30 month total project timelines from land acquisition to final delivery, with cash flow modeling accounting for delayed receivables from construction-to-permanent financing transitions.

Sensitivity analysis becomes paramount. Successful developers model multiple scenarios:

- Base case: 14% credit growth materializes, absorption meets projections, costs remain stable

- Upside case: 18-20% credit growth, accelerated absorption, 8-10% price appreciation

- Downside case: 8-10% credit growth, extended absorption (24+ months), 5% cost overruns

Projects should demonstrate positive returns even in downside scenarios, with base case IRRs of 20%+ and upside scenarios reaching 28-32%. This risk-adjusted approach protects against market volatility while positioning for outperformance if conditions exceed expectations.

Key performance metrics to track:

- Absorption velocity: Units sold per month vs. projection

- Qualified buyer ratio: Percentage of prospects receiving mortgage approval

- Average days to contract: Time from first contact to signed purchase agreement

- Financing fallout rate: Percentage of contracts failing due to financing issues

- Construction cost per square meter: Actual vs. budgeted with variance analysis

Monthly variance reporting against these metrics enables rapid course correction, whether through pricing adjustments, enhanced incentives, or marketing strategy shifts.

Risk Mitigation Strategies

The Fixed-Rate Mortgages Expansion 2026 opportunity carries specific risks that sophisticated developers actively mitigate through structured approaches:

Interest rate risk: While fixed-rate mortgages protect buyers from rate volatility, developers remain exposed during construction phases. Hedging strategies include:

- Locking construction loan rates for 12-18 month periods

- Establishing rate buydown budgets assuming 7% fixed rates (above current 6-6.5% levels)

- Maintaining relationships with multiple lenders to source competitive rates if primary partners tighten

Credit tightening risk: If lenders reduce mortgage availability or tighten qualification standards mid-project, absorption can stall. Mitigation approaches:

- Securing lender commitments for project-specific allocation quotas

- Diversifying across 3-5 lending partners rather than single-source dependency

- Maintaining 10-15% of inventory available for cash buyers or alternative financing

Construction cost inflation: Material and labor costs can escalate 15-25% annually in high-growth regional markets. Protection mechanisms:

- Fixed-price contracts with general contractors including material escalation caps

- Early procurement of long-lead items (elevators, windows, major systems)

- Value engineering during design phase identifying cost-reduction opportunities

Regulatory changes: Zoning modifications, environmental requirements, or tax policy shifts can impact project economics. Defensive measures:

- Securing all major permits before land acquisition closing

- Maintaining active relationships with municipal planning departments

- Building regulatory contingency reserves (2-3% of budget) for compliance costs

Market absorption risk: If competing projects launch simultaneously or economic conditions deteriorate, absorption can extend significantly. Countermeasures:

- Phased development approaches limiting initial inventory exposure

- Flexible pricing strategies enabling tactical discounting without brand damage

- Enhanced marketing budgets (5-7% of revenue vs. typical 3-4%) ensuring visibility

Developers who implement comprehensive risk management frameworks consistently outperform those taking aggressive, unhedged positions. In volatile markets, capital preservation matters as much as return maximization. For additional insights on market dynamics and investment strategies, explore our coverage of Florianópolis’s real estate market outlook.

Implementation Roadmap: From Strategy to Execution

Phase 1: Market Selection and Site Acquisition (Months 1-4)

Successful execution of mid-income launches under the Fixed-Rate Mortgages Expansion 2026 begins with disciplined market selection and strategic site acquisition. This foundational phase determines 60-70% of ultimate project success.

Market selection criteria:

✅ Population growth: Target markets with 1.5-3% annual population growth (2-3x national average)

✅ Employment diversity: Markets with 3+ significant employment sectors reducing economic concentration risk

✅ Mortgage penetration: Current mortgage-to-GDP ratios below national average indicating growth potential

✅ Competitive landscape: Markets with fewer than 5 active mid-income projects ensuring demand concentration

✅ Infrastructure investment: Municipal or state infrastructure projects (highways, transit, utilities) supporting growth

Site acquisition checklist:

- Zoning permits 2-3 story residential development with desired density (minimum 80 units/hectare)

- Existing infrastructure connections within 200 meters (water, sewage, electricity, fiber optic)

- Access via paved roads with public transportation within 500 meters

- Proximity to employment centers (15-25 minute commute), schools (within 1km), and retail (within 2km)

- Clear title with no environmental restrictions or indigenous land claims

- Topography suitable for efficient construction (maximum 8% slope preferred)

Financial parameters for land acquisition:

- Land cost should represent 15-20% of final unit sale prices

- Target 25-30% of total project costs for land acquisition

- Negotiate seller financing or extended payment terms reducing upfront capital requirements

- Structure earnest money deposits with permitting contingencies protecting downside

Due diligence should consume 60-90 days, including environmental assessments, geotechnical surveys, title verification, and preliminary architectural studies. Rushing this phase to capture perceived opportunities consistently leads to costly surprises during construction.

Phase 2: Product Development and Pre-Sales (Months 4-8)

With site secured, focus shifts to product optimization and pre-sales launch preparation. This phase establishes the project’s market positioning and generates critical early momentum.

Product development priorities:

Unit mix optimization: Develop 2-3 unit types maximum (typically 2BR/1BA, 2BR/2BA, 3BR/2BA) with 60-70% of inventory in the highest-demand configuration based on market research.

Amenity selection: Focus on 4-6 high-impact amenities rather than spreading budgets across 10+ mediocre offerings. Prioritize fitness center, coworking space, children’s play area, and secure parking.

Finish specifications: Select durable, attractive finishes that photograph well and appeal to target demographics without excessive cost (engineered wood flooring, quartz-style countertops, stainless steel appliances).

Sustainability features: Incorporate LED lighting, low-flow fixtures, efficient HVAC, and solar pre-wiring—features with strong ROI through buyer appeal and ongoing cost savings.

Pre-sales strategy:

Launch pre-sales when project is 20-30% through permitting process and construction financing is secured. Target 30-40% of inventory sold before breaking ground, providing validation and cash flow for construction commencement.

Pricing strategy: Price initial phase units 5-8% below ultimate project pricing to generate momentum. Structure pricing tiers rewarding early buyers while preserving appreciation potential for later phases.

Marketing allocation: Budget 5-7% of projected revenue for pre-sales marketing, emphasizing digital channels (social media, search advertising, property portals) and local partnerships (employers, community organizations, real estate brokers).

Sales center: Invest in professional sales environments (decorated model units, interactive displays, financing calculators) that build confidence and facilitate decision-making. Virtual alternatives work for regional buyers but physical presence remains important for local markets.

For developers seeking inspiration on successful project execution, reviewing case studies like the Tramonto development progress provides valuable insights.

Phase 3: Construction and Ongoing Sales (Months 8-30)

The construction phase demands operational excellence and sustained sales momentum. Projects that maintain consistent progress and communication significantly outperform those with irregular updates or delivery delays.

Construction management best practices:

- Weekly progress meetings with general contractor reviewing schedule, budget, and quality

- Monthly buyer updates including photos, videos, and milestone achievements

- Quarterly site tours for buyers reinforcing purchase decisions and generating referrals

- Proactive problem-solving addressing issues before they impact timeline or budget

- Quality control inspections at each construction phase preventing defects and rework

Ongoing sales execution:

Maintain active sales efforts throughout construction, adjusting tactics based on absorption velocity:

Strong absorption (>8 units/month): Maintain pricing discipline, reduce incentives, emphasize scarcity and final availability

Moderate absorption (4-7 units/month): Continue base strategy with selective incentives for bulk purchases or referrals

Weak absorption (<4 units/month): Implement aggressive incentives (enhanced rate buydowns, price reductions, expanded amenities), increase marketing spend, evaluate pricing strategy

Buyer communication program: Establish structured touchpoints (monthly emails, quarterly events, milestone celebrations) maintaining engagement and reducing buyer’s remorse or contract cancellations.

Referral generation: Implement formal referral programs offering R$5,000-R$10,000 credits for successful referrals, leveraging satisfied buyers as brand ambassadors.

Phase 4: Delivery and Post-Occupancy (Months 30-36)

The final phase transitions from construction to occupancy, requiring meticulous planning and execution to ensure positive buyer experiences that support future projects and referrals.

Delivery preparation:

- Conduct pre-delivery inspections 60 days before completion addressing punch-list items

- Schedule individual buyer walkthroughs 30 days before delivery for final approvals

- Coordinate with lenders ensuring financing closes smoothly without delays

- Prepare comprehensive owner’s manuals and warranty documentation

- Organize community orientation events introducing residents and building relationships

Post-occupancy support:

- Maintain responsive customer service addressing warranty issues within 48 hours

- Conduct 30-day, 90-day, and 12-month follow-ups assessing satisfaction and addressing concerns

- Facilitate HOA formation and transition ensuring professional community management

- Collect testimonials and reviews leveraging satisfied residents for future marketing

- Monitor property values and market conditions informing future project planning

Developers who excel in delivery and post-occupancy phases build brand equity that translates directly into faster absorption and premium pricing on subsequent projects. Reputation in regional markets spreads quickly through social networks and community connections.

Conclusion: Seizing the Fixed-Rate Mortgage Opportunity

The Fixed-Rate Mortgages Expansion 2026: Scaling Mid-Income Launches Under 14% Credit Growth Forecast represents a generational opportunity for Brazilian real estate developers who understand the market dynamics and execute strategically. The convergence of SELIC rate stability at 9.25%, expanded fixed-rate mortgage availability, and pent-up mid-income housing demand creates ideal conditions for well-planned projects in carefully selected markets. 📈

Success requires moving beyond traditional development approaches. Developers must embrace fixed-rate mortgage products as the new standard, structure strategic lender partnerships that provide competitive advantages, and implement buyer incentive programs that bridge affordability gaps without sacrificing profitability. Geographic targeting shifts toward regional markets where land costs, construction expenses, and competitive intensity support superior returns.

The 14% credit growth forecast for popular housing segments outside MCMV subsidies signals that lenders recognize mid-income Brazilians as creditworthy borrowers when provided appropriate mortgage products. This institutional confidence, combined with stable interest rate environments and moderating home price growth, creates a sustainable foundation for market expansion rather than speculative bubble dynamics.

Key action steps for developers:

- Conduct comprehensive market analysis identifying 2-3 target regional markets meeting growth, employment, and competitive criteria

- Establish lender partnerships with 3-5 institutions offering competitive fixed-rate products and streamlined underwriting

- Develop optimized product featuring 2-3 unit types priced at R$250,000-R$450,000 with high-impact amenities

- Implement disciplined financial modeling with conservative absorption assumptions and comprehensive risk mitigation

- Execute professional pre-sales targeting 30-40% absorption before construction commencement

- Maintain operational excellence throughout construction with consistent buyer communication

- Deliver exceptional experiences building brand equity for future project success

The developers who will thrive under this expansion are those who view it not as a temporary opportunity but as a fundamental market evolution. Fixed-rate mortgages are becoming the dominant product in Brazilian residential finance, mid-income buyers are becoming increasingly sophisticated, and regional markets are emerging as profitability centers. These trends will persist well beyond 2026.

For developers ready to scale mid-income launches strategically, the time to act is now. Market conditions are favorable, financing is available, and demand is strong. Those who execute with discipline, creativity, and operational excellence will establish market leadership positions that compound over multiple project cycles.

To explore current development opportunities and learn more about successful project execution, visit our portfolio of developments or contact our team for personalized consultation on your next mid-income housing project.

References

[1] Mba Forecast Total Single Family Mortgage Originations To Increase 8 Percent To 2.2 Trillion In 2026 – https://www.mba.org/news-and-research/newsroom/news/2025/10/19/mba-forecast–total-single-family-mortgage-originations-to-increase-8-percent-to–2.2-trillion-in-2026

[2] 2026 Mortgage Industry Outlook Key Trends Impacting Home Ownership – https://www.fnbo.com/insights/mortgage/2026/2026-mortgage-industry-outlook-key-trends-impacting-home-ownership

[3] Mortgage Rates March 12 2026 – https://www.foxbusiness.com/economy/mortgage-rates-march-12-2026

[4] Mortgage Rates Forecast – https://www.bankrate.com/mortgages/mortgage-rates-forecast/

[5] 2026 Real Estate Outlook What Leading Housing Economists Are Watching – https://www.nar.realtor/magazine/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching