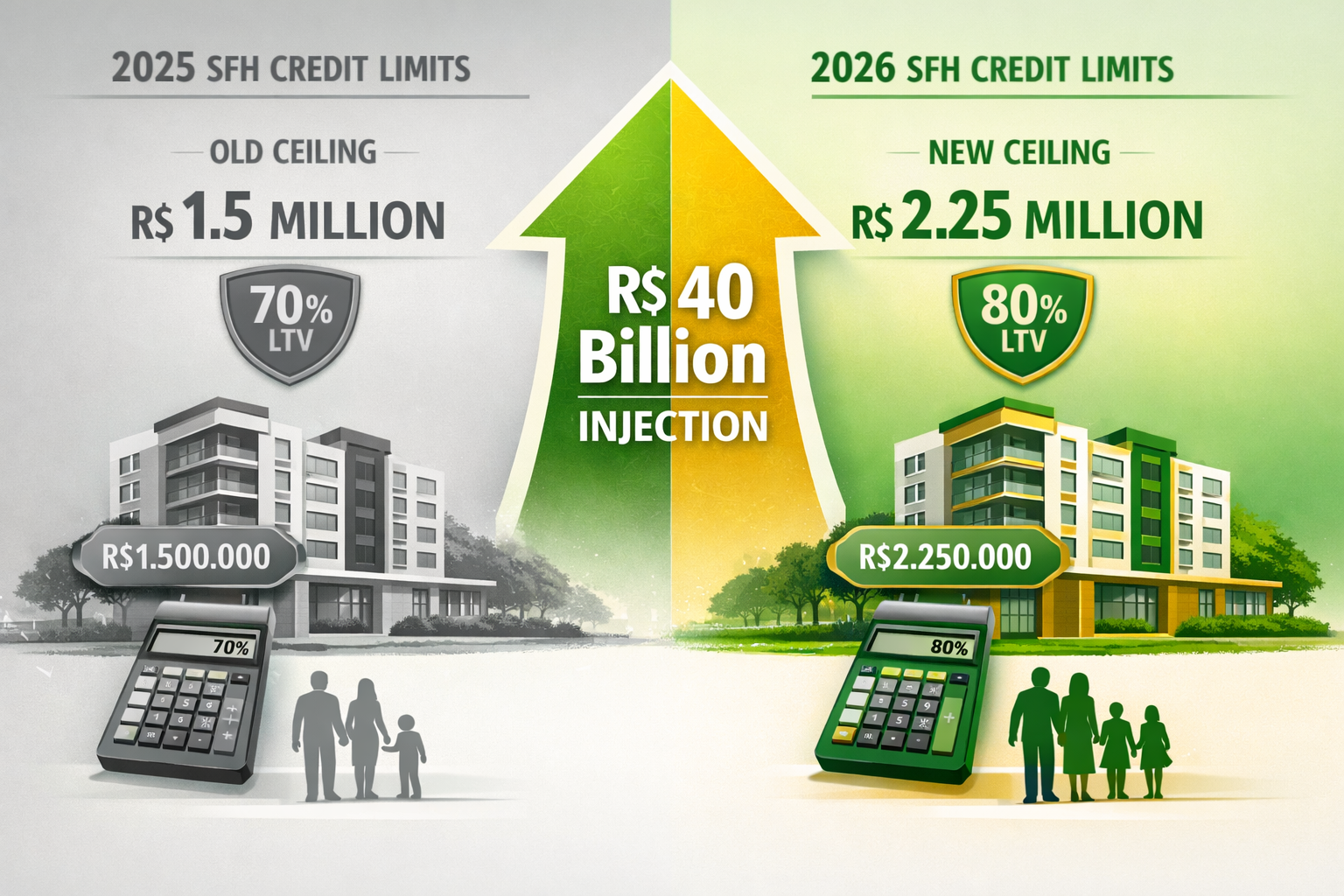

Brazil’s housing finance landscape underwent a seismic shift in October 2025 when federal authorities announced a comprehensive reform package injecting R$40 billion into the Sistema Financeiro de Habitação (SFH). This unprecedented expansion raised property-value ceilings from R$1.5 million to R$2.25 million while simultaneously increasing loan-to-value (LTV) ratios to 80%—a move projected to finance an additional 80,000 residential units across the country. The New SFH Credit Expansion 2026: Scaling Launches with 80% LTV and R$2.25M Ceiling for Mid-Range Condos represents the most significant overhaul of Brazil’s subsidized housing credit system in over a decade, fundamentally reshaping how developers plan unit mixes in densifying urban corridors.

For real estate developers and incorporators, particularly those operating in high-growth markets like Florianópolis and its surrounding regions, this reform opens unprecedented opportunities to target middle-income buyers who were previously priced out of subsidized financing programs.

Key Takeaways

- 🏗️ R$40 billion injection enables financing for 80,000 additional mid-range condominium units nationwide

- 💰 Property ceiling increased 50% from R$1.5M to R$2.25M, capturing premium mid-market segments

- 📊 80% LTV ratio reduces down payment barriers from 30% to 20%, expanding buyer accessibility

- 🏘️ Densifying corridors benefit most as developers can now optimize unit mixes for higher-value properties

- ⚖️ Regulatory streamlining parallels global trends toward correction-first supervision and reduced compliance burdens

Understanding the New SFH Credit Expansion 2026 Framework

The Sistema Financeiro de Habitação has served as Brazil’s primary subsidized housing finance mechanism since 1964, channeling mandatory savings from FGTS (Fundo de Garantia do Tempo de Serviço) and poupança (savings accounts) into residential mortgages at below-market rates. Prior to October 2025, the system imposed strict property-value ceilings that effectively excluded mid-range condominiums in appreciating markets from accessing these favorable financing terms.

Historical Context and Previous Limitations

Before the reform, SFH financing was capped at R$1.5 million with maximum LTV ratios of 70%, requiring buyers to provide 30% down payments. This structure created a significant financing gap for properties valued between R$1.5M and R$3M—precisely the segment where most quality two- and three-bedroom condominiums in secondary cities and metropolitan peripheries are priced.

The previous framework inadvertently pushed middle-class buyers toward either:

- Smaller, less desirable units within the R$1.5M ceiling

- More expensive properties requiring non-subsidized financing at market rates (typically 10-12% annually vs. SFH’s 8-9%)

This financing gap constrained developers’ ability to launch mid-range projects in densifying urban corridors, where land costs and construction quality naturally pushed unit prices above the old ceiling.

The October 2025 Reform Package

The New SFH Credit Expansion 2026: Scaling Launches with 80% LTV and R$2.25M Ceiling for Mid-Range Condos introduced three fundamental changes:

- Property Value Ceiling Increase: From R$1.5M to R$2.25M (50% increase)

- LTV Ratio Enhancement: From 70% to 80% maximum financing

- R$40 Billion Capital Injection: Specifically earmarked for the expanded program

These modifications took effect January 1, 2026, creating immediate opportunities for developers with projects in advanced planning stages to adjust their unit configurations and pricing strategies.

How the 80% LTV Ratio Transforms Buyer Accessibility

The increase from 70% to 80% LTV represents more than a simple 10-percentage-point adjustment—it fundamentally alters the financial feasibility equation for middle-income purchasers.

Down Payment Reduction Impact

Consider a typical R$2 million condominium unit in a growing neighborhood:

| Financing Structure | Old SFH (70% LTV) | New SFH (80% LTV) | Difference |

|---|---|---|---|

| Property Value | R$2,000,000 | R$2,000,000 | — |

| Maximum Financing | R$1,400,000 | R$1,600,000 | +R$200,000 |

| Required Down Payment | R$600,000 | R$400,000 | -R$200,000 |

| Down Payment as % of Value | 30% | 20% | -10 percentage points |

This R$200,000 reduction in upfront capital requirements represents approximately 2-3 years of median household savings for target buyers, dramatically shortening the time-to-purchase timeline.

Parallels with U.S. Conforming Loan Expansion

Interestingly, Brazil’s SFH expansion mirrors recent developments in the United States housing finance system. The 2026 conforming loan limit for single-family homes increased to $832,750, up 3.26% from $806,500 in 2025—an increase of $26,250 that expanded buying power without requiring jumbo financing.[4][7] This adjustment took effect January 1, 2026, for loans delivered to Fannie Mae and Freddie Mac, demonstrating a global trend toward expanding government-backed financing thresholds to match rising property values.

While the percentage increase differs (Brazil’s 50% vs. the U.S.’s 3.26%), both reforms share the same underlying objective: maintaining the relevance of subsidized financing programs in markets where property values have outpaced previous program limits.

Income Qualification Considerations

The expanded ceiling and higher LTV ratio shift the qualification bottleneck from down payment accumulation to monthly income verification. Under SFH rules, total housing expenses (mortgage payment, property tax, condominium fees, and insurance) cannot exceed 30% of gross household income.

For a R$1.6 million financed amount at 8.5% annual interest over 30 years:

- Monthly mortgage payment: approximately R$12,300

- Required minimum gross household income: R$41,000/month (R$492,000 annually)

This income threshold aligns well with dual-income professional households in Brazil’s expanding middle class, particularly in technology, healthcare, and financial services sectors concentrated in secondary cities experiencing economic diversification.

Strategic Implications for Developers: Optimizing Unit Mixes in Densifying Corridors

The New SFH Credit Expansion 2026: Scaling Launches with 80% LTV and R$2.25M Ceiling for Mid-Range Condos creates specific strategic opportunities for developers operating in urban corridors undergoing densification—areas transitioning from low-density residential to mixed-use, mid-rise development patterns.

Adjusting Unit Configuration Strategies

Developers can now confidently launch projects with unit mixes previously considered too expensive for the SFH market:

Pre-Reform Strategy (R$1.5M ceiling)

- 70% one-bedroom units (45-55m²)

- 25% two-bedroom units (60-70m²)

- 5% three-bedroom units (80-90m²)

- Average unit price: R$1.2M

Post-Reform Strategy (R$2.25M ceiling)

- 30% one-bedroom units (50-60m²)

- 50% two-bedroom units (70-85m²)

- 20% three-bedroom units (95-110m²)

- Average unit price: R$1.8M

This shift toward larger, higher-value units improves project economics through:

- Higher revenue per square meter of land

- Improved absorption rates by targeting underserved family-sized unit demand

- Better alignment with zoning incentives for mixed-income developments

- Enhanced project positioning in competitive markets

For developers working on new launches in high-growth regions, this flexibility to upsize unit mixes without sacrificing financing accessibility represents a significant competitive advantage.

Geographic Targeting: Where the Expansion Matters Most

The R$2.25 million ceiling has variable impact across Brazil’s diverse real estate markets:

High-Impact Markets (where R$1.5M-R$2.25M captures significant inventory):

- Secondary metropolitan areas (Florianópolis, Curitiba, Porto Alegre)

- Expanding neighborhoods in primary cities (São Paulo’s eastern zone, Rio’s Barra expansion)

- Coastal resort markets with year-round appeal

- University cities with professional employment growth

Moderate-Impact Markets (where ceiling increase captures premium segments):

- Established neighborhoods in primary cities

- State capitals with diversified economies

- Regional centers with infrastructure investment

Limited-Impact Markets (where values exceed R$2.25M or fall well below R$1.5M):

- Prime São Paulo and Rio neighborhoods (Jardins, Leblon, Ipanema)

- Remote or economically stagnant regions

Developers should conduct detailed market analysis to determine whether their target submarkets contain sufficient demand in the R$1.5M-R$2.25M price band to justify unit mix adjustments. Markets like Florianópolis’s expanding regions exemplify ideal conditions for leveraging the new framework.

Construction Quality and Amenity Considerations

The higher property ceiling enables developers to incorporate enhanced construction specifications and amenities without pricing units out of subsidized financing eligibility:

Previously Challenging Under R$1.5M Ceiling:

- Premium facade materials (architectural concrete, imported cladding)

- Expanded common areas (co-working spaces, fitness centers, rooftop terraces)

- Advanced building systems (smart home integration, energy management)

- Underground parking with electric vehicle charging infrastructure

- Higher-specification interior finishes

Now Feasible Within R$2.25M Ceiling:

- All of the above while maintaining SFH financing eligibility

- Competitive positioning against non-subsidized luxury projects

- Improved pre-construction sales velocity through enhanced product differentiation

This quality upgrade capability is particularly valuable in markets where buyers increasingly prioritize lifestyle amenities and sustainable building features alongside location and price considerations.

Regulatory Environment and Financing Accessibility Improvements

While Brazil’s SFH expansion operates within a distinct regulatory framework from other countries, parallel global trends in housing finance regulation provide useful context for understanding the broader policy environment.

The U.S. Executive Order on Mortgage Credit Access

On March 13, 2026, President Trump signed an executive order titled “Promoting Access to Mortgage Credit,” directing regulators to consider changes tailored to community banks (under $30 billion in assets) and smaller banks (under $100 billion in assets), including streamlined underwriting and reduced regulatory burden.[1][6]

The order introduced a “correction-first” supervisory approach where examiners evaluate mortgage lending effectiveness rather than penalizing good-faith technical errors, intended to increase lending confidence for creditworthy borrowers, particularly first-time homebuyers.[5]

Additionally, targeted Federal Home Loan Bank advances and liquidity programs were created specifically for entry-level housing, owner-occupied purchase loans, and small residential builders.[1][2][6]

Lessons for Brazil’s Implementation

While Brazil’s banking system operates under different regulatory structures, these international developments highlight several relevant principles:

Regulatory Certainty Matters: Clear, stable rules encourage lender participation and competitive pricing. The SFH expansion’s well-defined parameters (specific ceiling amounts, LTV ratios, and capital allocation) provide this certainty.

Streamlined Compliance Reduces Costs: Simplified documentation and approval processes translate to faster closings and lower transaction costs, improving affordability beyond just interest rate considerations.

Targeted Liquidity Programs Work: Dedicated capital pools for specific housing segments (like Brazil’s R$40 billion allocation) ensure that policy intentions translate into actual lending activity rather than being diluted across broader banking operations.

First-Time Buyer Focus Drives Volume: Programs explicitly designed to reduce barriers for first-time purchasers generate higher transaction volumes, benefiting developers through improved absorption rates.

Brazilian Banking Sector Response

Major Brazilian financial institutions participating in SFH lending—including Caixa Econômica Federal, Banco do Brasil, Itaú, Bradesco, and Santander—have announced expanded origination targets for 2026, with particular emphasis on the R$1.5M-R$2.25M segment.

Early indicators suggest strong institutional appetite:

- Caixa Econômica Federal: Announced R$15 billion allocation specifically for properties between R$1.5M-R$2.25M

- Private Banks: Increased marketing budgets for SFH products, signaling competitive positioning efforts

- Mortgage Brokers: Reporting 40-60% increase in pre-qualification inquiries for properties above the old R$1.5M ceiling

This institutional enthusiasm validates the program’s design and suggests robust financing availability for qualified buyers throughout 2026.

Implementation Timeline and Practical Considerations for 2026 Launches

For developers planning launches in 2026, understanding the practical implementation timeline of the New SFH Credit Expansion 2026: Scaling Launches with 80% LTV and R$2.25M Ceiling for Mid-Range Condos is essential for marketing and sales planning.

Key Dates and Milestones

- October 2025: Federal reform announcement

- December 2025: Regulatory guidelines published by Banco Central do Brasil

- January 1, 2026: New limits officially take effect

- Q1 2026: Banks update internal systems and train loan officers

- Q2 2026: Full market implementation with competitive product offerings

- Q3-Q4 2026: Expected peak transaction volume as buyer awareness matures

Pre-Launch Planning Adjustments

Developers with projects in planning or early construction phases should consider:

Financial Modeling Updates

- Revise pro forma assumptions for unit mix and pricing

- Recalculate absorption rates based on expanded buyer pool

- Adjust sales velocity projections for improved financing accessibility

- Update sensitivity analyses for interest rate scenarios

Marketing Strategy Modifications

- Emphasize financing accessibility in promotional materials

- Develop educational content explaining new SFH limits

- Partner with banks for co-marketing initiatives

- Create comparison tools showing down payment savings vs. previous requirements

Sales Team Training

- Ensure sales representatives understand new qualification criteria

- Develop scripts addressing common buyer questions about the expanded program

- Establish relationships with mortgage brokers specializing in SFH financing

- Create streamlined pre-qualification processes to accelerate sales cycles

Buyer Education and Sales Acceleration

The expanded SFH framework creates a temporary information asymmetry—developers and financial institutions understand the new opportunities, but many potential buyers remain unaware of their improved purchasing power.

Proactive buyer education initiatives can accelerate sales velocity:

- Financial Workshops: Host events explaining the new limits and qualification process

- Online Calculators: Provide tools showing personalized financing scenarios

- Bank Partnerships: Arrange on-site mortgage specialists during sales events

- Case Studies: Share success stories of buyers leveraging the new framework

- Comparison Materials: Create clear before/after illustrations of down payment requirements

Developers who invest in comprehensive buyer education during 2026 will likely capture disproportionate market share as awareness of the new opportunities spreads gradually through the broader market.

Risk Factors and Mitigation Strategies

While the New SFH Credit Expansion 2026: Scaling Launches with 80% LTV and R$2.25M Ceiling for Mid-Range Condos creates significant opportunities, prudent developers should also consider potential risk factors:

Interest Rate Sensitivity

SFH mortgage rates, while subsidized, still fluctuate based on broader monetary policy. The Banco Central do Brasil’s SELIC rate decisions directly impact SFH lending rates, affecting buyer qualification and demand.

Mitigation: Incorporate interest rate sensitivity analyses in project feasibility studies, maintaining financial viability across a range of rate scenarios (±2 percentage points from base case).

Supply Response and Competition

Successful programs often trigger supply responses that can temporarily oversaturate markets. If many developers simultaneously pivot toward the R$1.5M-R$2.25M segment, localized competition may intensify.

Mitigation: Differentiate through location, amenities, construction quality, and brand reputation rather than competing solely on price. Focus on specific submarkets with demonstrated undersupply in the target price range.

Regulatory Adjustments

Government housing programs occasionally undergo mid-course corrections based on implementation experience. While major changes are unlikely in 2026, developers should monitor policy discussions.

Mitigation: Maintain flexibility in unit mix configurations and pricing strategies, avoiding over-optimization for a single financing scenario.

Economic Volatility

Brazil’s macroeconomic environment can shift rapidly, affecting employment, income growth, and consumer confidence—all critical drivers of housing demand.

Mitigation: Emphasize pre-construction sales strategies that lock in buyer commitments early, reducing exposure to economic shifts during construction periods.

Conclusion

The New SFH Credit Expansion 2026: Scaling Launches with 80% LTV and R$2.25M Ceiling for Mid-Range Condos represents a transformative shift in Brazil’s residential real estate finance landscape. By raising property-value ceilings by 50% and increasing LTV ratios to 80%, the reform unlocks access to subsidized financing for 80,000 additional units valued at R$40 billion—precisely targeting the mid-range condominium segment that serves Brazil’s expanding professional middle class.

For developers operating in densifying urban corridors, this expansion enables strategic repositioning of unit mixes toward larger, higher-value configurations without sacrificing financing accessibility. The reform’s timing aligns with broader global trends toward expanded government-backed mortgage programs and streamlined regulatory frameworks, as evidenced by parallel developments in the United States housing finance system.

Actionable Next Steps for Developers

Conduct Market Analysis: Evaluate whether your target submarkets contain sufficient demand in the R$1.5M-R$2.25M price band to justify unit mix adjustments

Update Financial Models: Revise project pro formas incorporating new unit configurations, pricing strategies, and absorption rate assumptions

Establish Banking Relationships: Develop partnerships with SFH lenders to ensure financing availability for your buyers and explore co-marketing opportunities

Invest in Buyer Education: Create comprehensive educational materials and programs to accelerate market awareness of the new financing opportunities

Differentiate Your Product: Leverage the higher ceiling to incorporate quality enhancements and amenities that distinguish your projects in increasingly competitive markets

Monitor Implementation: Track early market response, competitor strategies, and regulatory developments to refine your approach throughout 2026

The developers who move decisively to capitalize on these expanded financing parameters—while maintaining disciplined risk management and product differentiation—will be best positioned to capture market share in what promises to be a dynamic year for Brazil’s mid-range condominium sector.

For those exploring development opportunities in high-growth markets, the combination of expanded financing accessibility, favorable demographic trends, and infrastructure investment creates a compelling environment for strategic project launches throughout 2026 and beyond.

References

[1] Executive Order Seeks To Expand 2686881 – https://www.jdsupra.com/legalnews/executive-order-seeks-to-expand-2686881/

[2] Trump Issues Executive Orders On Mortgage Credit Housing Construction – https://www.bhfs.com/insight/trump-issues-executive-orders-on-mortgage-credit-housing-construction/

[4] Conforming Loan Limits 2026 – https://better.com/content/conforming-loan-limits-2026

[5] A New Horizon For Housing Why Summer 2026 Promises Unprecedented Growth And Affordability – https://coastline-properties.com/a-new-horizon-for-housing-why-summer-2026-promises-unprecedented-growth-and-affordability/

[6] Fact Sheet President Donald J Trump Promotes Access To Mortgage Credit – https://www.whitehouse.gov/fact-sheets/2026/03/fact-sheet-president-donald-j-trump-promotes-access-to-mortgage-credit/

[7] The Complete Guide To Conforming Loans In Everything You Need To Know Before You Apply – https://www.amerisave.com/learn/the-complete-guide-to-conforming-loans-in-everything-you-need-to-know-before-you-apply