Brazil’s benchmark interest rate stood at 15% at the close of 2025 — one of the highest real interest rates among major emerging economies — yet financial market analysts are already pricing in a 275-basis-point decline that would bring the Selic to 12.25% by the end of 2026 [2][3]. That single forecast is quietly reshaping how developers, investors, and buyers think about mid-market real estate launches this year.

The Selic Drop to 12.25% Forecast 2026: Pipeline Timing for Mid-Market Launches is not just a macroeconomic data point. It is a strategic signal — one that determines when to break ground, when to open sales tables, and how to structure financing incentives for the mid-tier buyer segment that responds most acutely to mortgage rate movements.

This article unpacks the rate trajectory, the optimal launch windows it creates, and the risk-hedging strategies developers can deploy to protect margins while capturing demand.

Key Takeaways

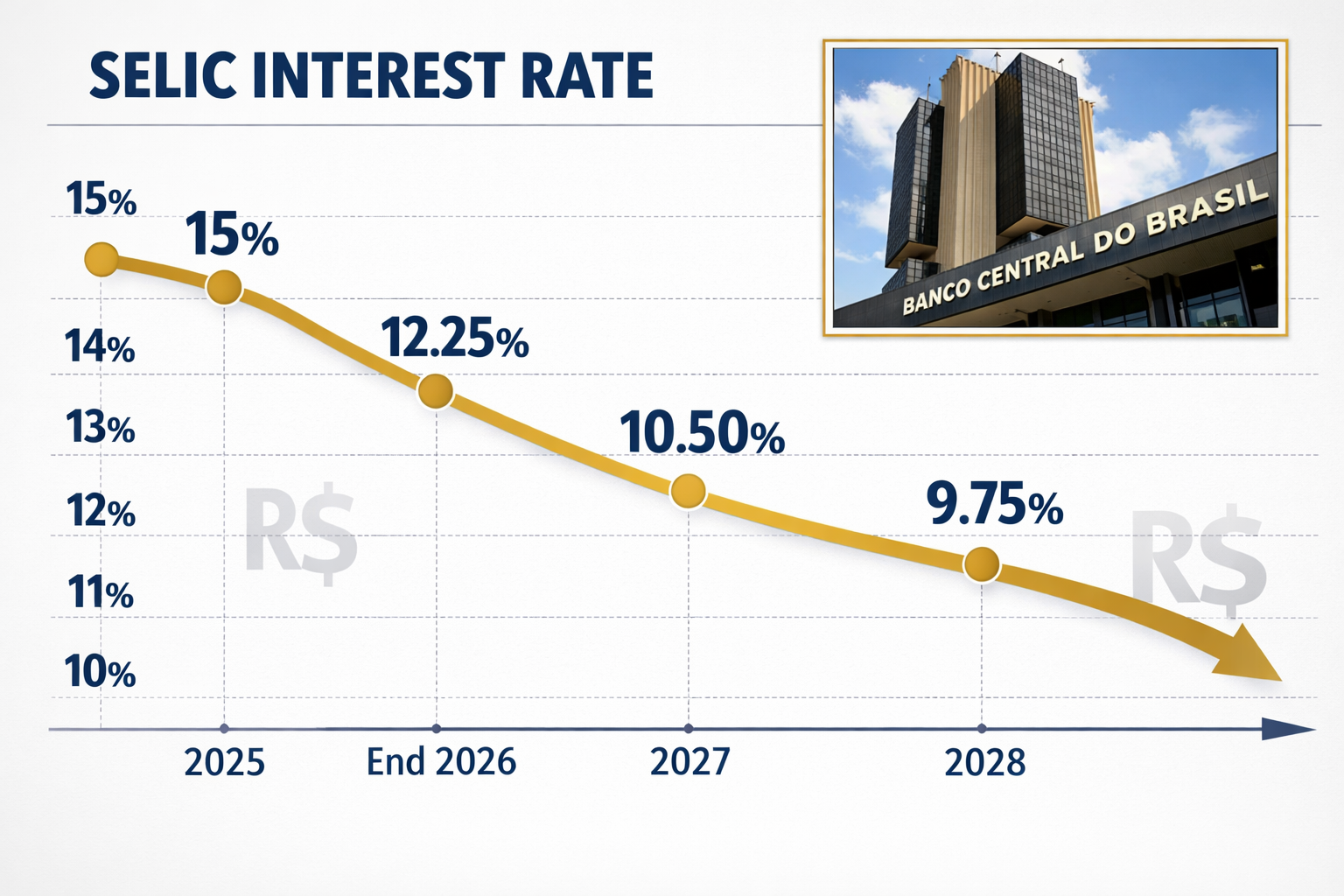

- 🏦 The Selic is forecast to fall from 15% (end-2025) to 12.25% by end-2026, a 275-basis-point reduction that directly lowers mortgage costs [2][3].

- 📅 Mid-market launch windows are most favorable in Q3–Q4 2026, when rate cuts are expected to be most visible to buyers.

- 🏗️ Pipeline timing matters: projects launched too early miss the affordability tailwind; launched too late, they face rising land and input costs.

- 🛡️ Government program tie-ins (such as Minha Casa Minha Vida) can hedge fiscal risk during the transition period when rates are still elevated.

- 📊 Inflation near 4.06% and GDP growth at 1.8% create a nuanced backdrop — opportunity is real, but margin discipline is essential [3].

Understanding the Rate Trajectory: From 15% to 12.25%

Where the Selic Stands in 2026

The Brazilian Central Bank (Banco Central do Brasil) closed 2025 with the Selic at 15%, a level reflecting persistent inflation-fighting pressure [2]. As of late January 2026, market analysts surveyed in the Focus Report — Brazil’s authoritative weekly consensus poll — were projecting a steady, managed descent throughout the year [3].

“The Focus Report opened 2026 with inflation near the ceiling and rates still heavy — but the direction of travel is unmistakably downward.” [3]

The projected path looks like this:

| Year-End | Forecast Selic Rate | Change vs. Prior Year |

|---|---|---|

| 2025 (actual) | 15.00% | — |

| 2026 (forecast) | 12.25% | −275 bps |

| 2027 (forecast) | 10.50% | −175 bps |

| 2028 (forecast) | 9.75% | −75 bps |

Sources: [2][3]

Why the Pace Matters More Than the Destination

A drop from 15% to 12.25% sounds dramatic, but the pace of cuts is what shapes developer strategy. If the Central Bank front-loads reductions in H1 2026, buyers feel relief earlier and sales velocity accelerates mid-year. If cuts are back-loaded to H2 2026, the optimal launch window shifts toward Q4.

Inflation is a key variable. The Focus Report projects consumer price growth at approximately 4.06% for 2026 — within Brazil’s official target band of 3% (±1.5 percentage points) but uncomfortably close to the 4.5% ceiling [3]. That proximity gives the Central Bank reason to move cautiously, suggesting a gradual, back-half-weighted cutting cycle is the more likely scenario.

GDP growth of 1.8% for 2026 adds another layer [2][3]. Modest expansion means employment holds up enough to support buyer qualification, but it is not robust enough to generate speculative demand. Mid-market developers must earn each sale through pricing discipline and financing creativity — not market exuberance.

Selic Drop to 12.25% Forecast 2026: Pipeline Timing for Mid-Market Launches — The Strategic Framework

Why Mid-Market Is the Focal Segment

The mid-market segment — broadly defined as units priced between R$350,000 and R$800,000 in major Brazilian metros — is uniquely sensitive to the Selic rate for three reasons:

- Mortgage dependency: Unlike luxury buyers who often purchase with equity, mid-market buyers rely heavily on bank financing. Every 100-basis-point rate cut can meaningfully reduce monthly payments and expand the qualifying buyer pool.

- Government program adjacency: Many mid-market projects can be structured to qualify for subsidized programs, creating a natural hedge against rate volatility.

- Demand depth: This segment represents the largest share of latent demand in Brazilian cities, particularly in growth markets like Florianópolis.

For developers tracking market performance in Florianópolis, the mid-market opportunity is already visible in sales velocity data from 2025 — and the Selic decline is expected to amplify it significantly.

The Launch Window Matrix

Timing a mid-market launch is not simply about waiting for the lowest possible rate. It involves balancing buyer readiness, construction cost escalation, land pricing, and competitive inventory. The table below maps these variables against the expected rate environment:

| Launch Quarter | Expected Selic Range | Buyer Sentiment | Land/Input Cost Risk | Recommended Action |

|---|---|---|---|---|

| Q1 2026 | ~14.25–14.75% | Cautious | Moderate | Pre-launch sales, VGV lock-in |

| Q2 2026 | ~13.50–14.00% | Improving | Moderate-High | Soft launch, early adopter pricing |

| Q3 2026 | ~12.75–13.25% | Positive | High | Full launch, marketing push |

| Q4 2026 | ~12.25–12.75% | Strong | High | Velocity phase, close pipeline |

Key insight: The Q3–Q4 2026 window aligns the highest buyer confidence with the most visible rate relief — making it the prime launch corridor for mid-tier condominiums.

Pre-Launch Preparation: What Must Happen Now

Developers targeting a Q3 2026 launch need to be in active preparation today. A standard mid-market condominium project requires:

- ✅ Licensing and permits: 12–18 months minimum lead time

- ✅ Land acquisition: Prices typically rise as rate optimism builds — secure land before the narrative fully shifts

- ✅ Sales team training: Mortgage calculators and financing scenario tools must be ready before the rate cuts materialize

- ✅ Government program qualification: Determine eligibility thresholds early to build program tie-ins into the product design

For a closer look at how buying off-plan can amplify investor returns, the pre-launch phase is where the most significant value is created — for both developer and buyer.

Hedging Fiscal Risk: Government Program Tie-Ins and Structural Safeguards

The Case for Program Integration

Even with the Selic Drop to 12.25% Forecast 2026 providing a favorable macro backdrop, fiscal risks remain. Inflation near the target ceiling [3] means the Central Bank could pause or slow cuts if price pressures re-accelerate. A developer who has structured their entire business model around a smooth rate decline is exposed.

Government program tie-ins are the most effective hedge available. Programs like Minha Casa Minha Vida (MCMV) provide:

- 🏠 Subsidized interest rates that are independent of the Selic cycle

- 📋 Pre-qualified buyer pools with government-backed financing

- 💰 Guaranteed off-take for a portion of units, reducing sales risk

- 🔒 Fixed-rate financing that insulates buyers from rate volatility

Mid-market developers can structure projects with a blended approach: a portion of units at market rates (capturing upside from Selic declines) and a portion within program thresholds (providing a sales floor regardless of macro conditions).

Risk Scenarios to Model

Responsible pipeline planning requires stress-testing against at least three scenarios:

Scenario A — Base Case (Most Likely) Selic reaches 12.25% by December 2026. Inflation stays near 4%. GDP grows 1.8%. Mid-market demand recovers steadily through H2 2026. Launch in Q3 captures the demand wave.

Scenario B — Hawkish Pause Inflation spikes toward 4.5%, forcing the Central Bank to pause cuts at ~13.5%. Buyer sentiment softens. Program-tied units absorb the shortfall; market-rate units face slower absorption.

Scenario C — Accelerated Easing Global conditions improve, inflation falls below 3.5%, and the Selic reaches 12.25% by mid-2026. Demand accelerates ahead of forecast. Developers who launched in Q2 capture outsized velocity.

Modeling all three scenarios before committing to a launch date is not optional — it is the minimum standard of professional project management.

The Role of Alternative Financing Structures

Beyond government programs, developers are increasingly exploring innovative capital structures. The intersection of cryptocurrency and real estate development represents one frontier — tokenized receivables and blockchain-based escrow can reduce developer financing costs independently of the Selic trajectory.

Studio and compact-format units also offer a structural hedge: lower absolute prices mean smaller mortgage requirements, making buyers less sensitive to rate levels. The advantages of investing in studio apartments in Florianópolis illustrate how format innovation can unlock demand even in high-rate environments.

Location Strategy: Where Mid-Market Demand Is Concentrating

Growth Corridors in 2026

The Selic decline does not lift all markets equally. Demand concentrates in cities with strong employment fundamentals, infrastructure investment, and lifestyle appeal. In 2026, several Brazilian markets stand out:

- Florianópolis and Greater Florianópolis: Tech sector employment, tourism, and quality-of-life migration continue to drive demand. The real estate market in Greater Florianópolis has shown consistent resilience.

- Coastal growth zones: Neighborhoods like Ingleses in Florianópolis are experiencing infrastructure upgrades that directly support property value appreciation.

- Secondary cities with university anchors: Education-driven demand creates stable rental yields that support investor-buyer profiles.

What Mid-Market Buyers Are Looking For in 2026

Understanding buyer psychology in a declining-rate environment is critical to product design:

| Buyer Priority | Implication for Product Design |

|---|---|

| Monthly payment certainty | Offer fixed-rate financing partnerships |

| Amenity quality | Invest in shared spaces over unit size |

| Location connectivity | Prioritize transit access and walkability |

| Delivery timeline confidence | Transparent construction progress reporting |

| Resale potential | Choose locations with documented appreciation history |

Developers with active construction portfolios — and the track record to prove delivery commitments — hold a significant advantage. Buyers in the mid-market segment are sophisticated enough to check construction progress updates before committing to a purchase.

Practical Launch Checklist for Mid-Market Developers in 2026

For developers ready to act on the Selic Drop to 12.25% Forecast 2026: Pipeline Timing for Mid-Market Launches, the following checklist provides a structured action plan:

🗓️ Q1 2026 — Foundation Phase

- Finalize land acquisition in target growth corridors

- Complete government program eligibility assessment

- Engage banking partners for mortgage product design

- Begin permit and licensing submissions

- Develop stress-tested financial models for all three rate scenarios

🏗️ Q2 2026 — Pre-Launch Phase

- Soft-launch to investor database with early-adopter pricing

- Activate digital marketing campaigns targeting buyer personas

- Lock in construction contracts before input cost escalation

- Finalize unit mix based on market research

🚀 Q3–Q4 2026 — Full Launch Phase

- Open public sales with full financing partnerships in place

- Deploy mortgage calculator tools on all digital channels

- Activate program-tied unit sales simultaneously

- Monitor Selic cut announcements and adjust messaging in real time

Conclusion: Turning a Rate Forecast Into a Competitive Advantage

The projected Selic Drop to 12.25% Forecast 2026: Pipeline Timing for Mid-Market Launches represents one of the clearest strategic signals the Brazilian real estate market has produced in years. A 275-basis-point decline in the benchmark rate [2][3] will meaningfully expand the pool of qualified mid-market buyers — but only for developers who are positioned to capture that demand when it peaks.

The key is timing. Launching too early means absorbing high financing costs before buyer sentiment has shifted. Launching too late means competing in a crowded market where land costs have already repriced. The Q3–Q4 2026 window is the sweet spot — and reaching it requires decisions made today.

Actionable next steps for developers and investors:

- Audit your current pipeline against the launch window matrix and identify which projects are positioned for Q3–Q4 2026 delivery.

- Assess government program eligibility for each project and build program tie-ins into the product design now — not after launch.

- Engage banking partners early to develop co-branded mortgage products that can be activated the moment rate cuts make headlines.

- Choose locations with documented demand fundamentals — coastal growth corridors, tech employment hubs, and infrastructure-upgraded neighborhoods.

- Explore current development opportunities through established developers with proven delivery track records and transparent construction progress.

For those evaluating active projects in high-growth Brazilian markets, exploring current real estate developments with strong location fundamentals and transparent delivery timelines is a logical starting point.

The rate cycle is turning. The pipeline window is open. The developers who act with strategic discipline in 2026 will define the mid-market landscape for the rest of the decade.

References

[1] Trading Economics – https://tradingeconomics.com/articles/02222017213352.htm

[2] Xinhua English News – https://english.news.cn/20260127/101ef38a7ad44e02bcc42ee1c7179067/c.html

[3] Brazil’s Focus Report Opens 2026 With Inflation Near The Ceiling Rates Still Heavy – https://www.riotimesonline.com/brazils-focus-report-opens-2026-with-inflation-near-the-ceiling-rates-still-heavy/