Brazil’s housing deficit stood at 5,773,983 units as recently as 2024, yet the most persistent gap is not where most people assume it to be. [5] The families earning between R$ 4,000 and R$ 13,000 per month — too prosperous to qualify for the deepest subsidies, too financially stretched to absorb luxury pricing — are the segment that the market has consistently underserved. The conversation about Affordable Housing in Brazil Beyond MCMV: Where Mid-Income Demand Is Most Underserved in 2026 is no longer a niche policy debate. It is a real estate strategy question with direct implications for developers, investors, and urban planners navigating one of the most dynamic property markets in Latin America.

Key Takeaways

- Brazil’s April 2026 MCMV expansion to Faixa 4 (incomes up to R$ 13,000; properties up to R$ 600,000) created a new policy bridge, but product supply has not yet caught up with demand in most cities.

- The mid-income segment — roughly R$ 4,000 to R$ 13,000 monthly household income — remains the least served by both public programs and private developers in secondary urban corridors.

- Metropolitan fringes and fast-growing secondary cities such as Florianopolis, Campinas, Goiania, and Cuiaba show the highest absorption risk for mid-income units because supply pipelines are thin relative to population growth.

- Pricing bands between R$ 300,000 and R$ 600,000 represent the critical product zone where positioning errors — too basic or too premium — create unsold inventory.

- Developers who understand income segmentation, local absorption rates, and infrastructure trajectories will capture outsized returns in this underserved band.

The MCMV Expansion of 2026 and What It Actually Covers

The Minha Casa Minha Vida (MCMV) program has been the cornerstone of Brazilian social housing policy for over a decade. In April 2026, the government significantly restructured the program. A new Faixa 4 was introduced, extending eligibility to families earning up to R$ 13,000 per month and allowing financing of properties valued up to R$ 600,000. [1] Banco do Brasil and Caixa Econômica Federal began operating under these new rules as of April 22, 2026. [1]

Simultaneously, the income and property value limits across existing brackets were revised. Faixa 1 now covers families earning up to R$ 3,200 monthly, while the ceiling for Faixa 3 properties rose to R$ 400,000. [3] The Fundo Social injected an additional R$ 20 billion into MCMV, bringing the 2026 total budget to R$ 45 billion, with a target of 1 million new housing units by year-end. [2] The Conselho Curador do FGTS had already set the stage in November 2025 by approving a record R$ 144.5 billion for housing in 2026. [4]

These are significant numbers. But policy expansion and physical supply are two different things. The critical question for anyone analyzing Affordable Housing in Brazil Beyond MCMV: Where Mid-Income Demand Is Most Underserved in 2026 is this: where does the new policy framework still leave households without viable product options?

The Gap Between Eligibility and Available Inventory

Eligibility for a financing bracket does not guarantee that suitable properties exist at that price point in a given city. The real estate sector recorded a 5.4% increase in sales volume and a 6.2% rise in final unit offers between 2024 and 2025, predominantly in the apartment segment. [8] However, this growth has been concentrated in established metropolitan markets and in the luxury-to-upper-mid tier. The R$ 300,000 to R$ 600,000 band — the natural habitat of the newly eligible Faixa 4 buyer — remains thin in supply across most secondary cities.

Experts have flagged another complication: the inclusion of the middle class in MCMV is likely to increase demand pressure and could drive property prices upward, potentially eroding the affordability gains the expansion was designed to create. [7] This price-push dynamic is especially acute in markets where land costs are rising and construction timelines are long.

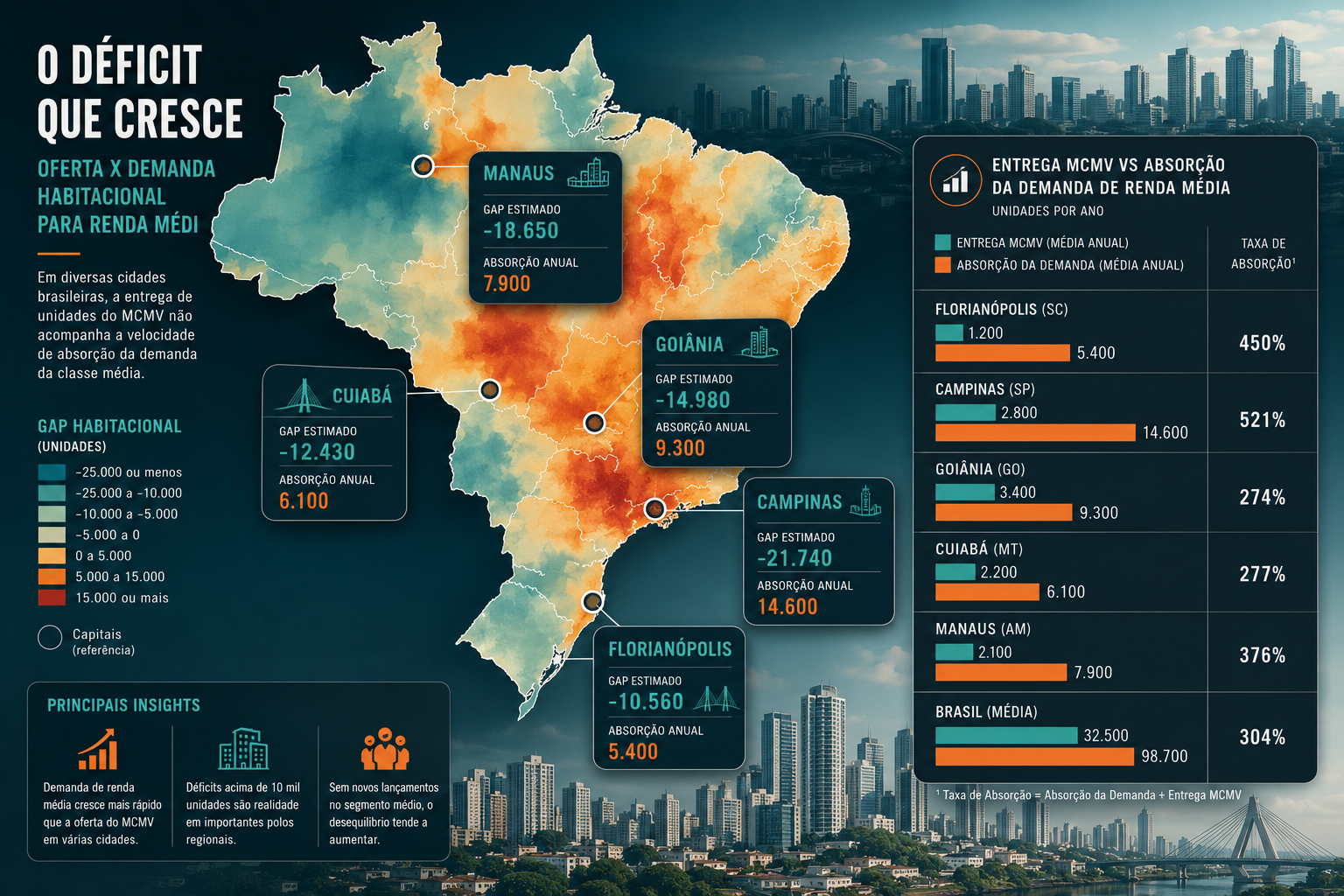

Where Mid-Income Demand Is Most Underserved: A Regional Breakdown

Understanding which cities and corridors carry the highest unmet demand requires looking at three intersecting variables: population growth rate, current housing supply pipeline, and median household income distribution. The following table summarizes the most underserved markets in 2026.

| City / Region | Population Growth Driver | Mid-Income Supply Gap | Key Risk Factor |

|---|---|---|---|

| Florianopolis metro | Tech sector, tourism | High | Land scarcity, permitting delays |

| Campinas (SP interior) | Industrial expansion | High | Competing luxury supply |

| Goiania (Center-West) | Agribusiness wealth | Moderate-High | Infrastructure lag |

| Cuiaba / Mato Grosso | Agricultural boom | High | Limited developer presence |

| Manaus metro | Industrial zone growth | Moderate | Logistics costs |

| Recife / Caruaru corridor | Service sector expansion | Moderate | Income volatility |

| Belo Horizonte fringes | Urban sprawl | Moderate-High | Absorption rate uncertainty |

Florianopolis and the Southern Corridor

Florianopolis is a textbook case of demand outpacing supply in the mid-income band. The city’s technology and tourism sectors have sustained above-average income growth, yet the housing market has historically bifurcated between subsidized low-income units and premium coastal developments. The real estate market in Greater Florianopolis has been trending upward, with strong absorption rates even for off-plan purchases.

For buyers and investors, the logic of buying off-plan in Florianopolis is compelling precisely because mid-income product in well-located sub-markets appreciates before delivery. The northern coastal expansion zone, including the Ingleses region, exemplifies this dynamic. Growth in the Ingleses area has been driven by quality-of-life migration from larger metros, creating sustained demand from households in the R$ 6,000 to R$ 12,000 monthly income range — precisely the segment that Faixa 4 now targets.

The Center-West and Agricultural Wealth Corridor

Goiania, Cuiaba, and the broader Center-West corridor represent a different but equally compelling case. Agribusiness wealth has created a substantial mid-income professional class — agronomists, logistics managers, financial services workers — whose housing needs are not met by either MCMV’s lower brackets or the limited luxury supply that exists in these markets. The absence of major national developers in these cities creates a structural opportunity for regional and mid-size incorporadoras willing to position product correctly.

São Paulo’s Interior and the Campinas Effect

Campinas and the broader São Paulo interior (Ribeirão Preto, São José dos Campos, Sorocaba) have seen industrial and technology sector growth that has lifted median household incomes significantly. Yet the housing supply in the R$ 350,000 to R$ 550,000 range has not kept pace. Developers in these markets face a specific challenge: the proximity to São Paulo attracts luxury-tier product positioning, but the actual demand profile of local residents skews firmly toward the mid-income band.

Product Positioning, Pricing Bands, and Absorption Risk

The central strategic challenge for developers targeting the mid-income segment is product differentiation without price escalation. This is harder than it sounds. The R$ 300,000 to R$ 600,000 pricing band is wide enough to accommodate very different product types, but the wrong positioning within that band creates serious absorption risk.

What Mid-Income Buyers Actually Want

Mid-income buyers in Brazil’s secondary cities and metropolitan fringes in 2026 share a consistent set of priorities:

- Location relative to employment corridors: Proximity to industrial parks, technology hubs, or commercial centers matters more than proximity to luxury amenities.

- Functional amenities over prestige features: Co-working spaces, covered parking, and reliable internet infrastructure rank higher than rooftop pools or concierge services.

- Unit size efficiency: Two- and three-bedroom units in the 55-80 square meter range represent the sweet spot. Studios are relevant in university and tech-hub sub-markets, as explored in the context of studio investment advantages in Florianopolis.

- Financing compatibility: With Faixa 4 now covering properties up to R$ 600,000, buyers are acutely aware of the ceiling and will resist pricing above it, even marginally.

“The mid-income buyer in 2026 is not looking for luxury at a discount. They are looking for quality, location, and financing certainty. Developers who conflate these two profiles will carry unsold inventory.”

The Absorption Risk Equation

Absorption risk — the probability that units remain unsold after launch — is highest when three conditions align: oversupply of a specific product type, income volatility in the target demographic, and infrastructure gaps that reduce actual livability despite nominal location advantages.

In markets like Cuiaba and Manaus, the risk is primarily infrastructure-related. Roads, schools, and healthcare access in newer residential zones often lag behind unit delivery by two to four years, which depresses resale values and slows absorption even when headline demand metrics look strong.

In markets like Campinas and Belo Horizonte’s fringes, the risk is more about product mix. Developers launching mid-income projects must carefully analyze whether competing supply in the same pricing band is already absorbing the available buyer pool. The best locations for high returns in Brazilian property analysis consistently shows that sub-market specificity — not just city-level data — determines absorption outcomes.

Pricing Band Discipline

The most common developer error in the mid-income segment is price creep driven by construction cost increases. When a project budgeted for the R$ 380,000 to R$ 450,000 range drifts to R$ 520,000 to R$ 580,000 at launch due to input cost escalation, it enters a more competitive tier where buyers have more options and financing terms become less favorable. Maintaining pricing discipline requires locking in land costs early, phasing construction strategically, and using standardized unit designs that reduce per-square-meter build costs without sacrificing perceived quality.

For a practical illustration of how phased construction can maintain project momentum while managing cost risk, the progress on developments like Tramonto demonstrates how disciplined execution translates to buyer confidence and sustained absorption.

Policy Gaps That Private Developers Must Fill

The April 2026 MCMV expansion is a meaningful step, but several structural gaps remain that private sector actors must address if the mid-income demand is to be served effectively.

The North Region Subsidy Increase

The government’s decision in November 2025 to raise the maximum subsidy for families in the North Region from R$ 55,000 to R$ 65,000 acknowledges that regional construction costs and land prices create different affordability thresholds. [4] However, subsidy increases alone do not create product. In Manaus and other Northern cities, the developer ecosystem is thin, construction logistics are expensive, and mid-income product pipelines remain inadequate relative to demand.

The Rural-Urban Transition Zone

In June 2026, the government announced the selection of proposals for 85,000 new MCMV units, with 50,000 designated for rural areas and 35,000 for urban zones, surpassing initial projections by 66%. [6] This rural emphasis reflects real demand but also highlights a gap: the peri-urban transition zones — areas that are neither formally rural nor fully urbanized — are where mid-income families often settle when urban prices exclude them. These zones need infrastructure investment and zoning clarity before private developers can operate at scale.

Interest Rate Sensitivity

Mid-income buyers are more sensitive to interest rate movements than either the lowest-income bracket (which benefits from deep subsidies) or the highest-income bracket (which can absorb rate changes). The FGTS-linked financing rates available under MCMV’s new structure provide some insulation, but market-rate components of hybrid financing deals remain exposed to Brazil’s broader monetary policy environment. Developers and buyers alike should monitor Selic rate trajectories as a key variable in mid-income housing viability through 2026 and beyond.

Strategic Implications for Developers and Investors

For developers and investors focused on the mid-income segment, the 2026 landscape presents a clear set of strategic priorities:

Prioritize secondary cities with strong employment fundamentals. Goiania, Campinas, Florianopolis, and Cuiaba offer the best combination of demand depth and supply scarcity. Avoid markets where luxury supply is already crowding the upper end of the mid-income pricing band.

Design for the Faixa 4 ceiling. With financing available for properties up to R$ 600,000, units priced at R$ 480,000 to R$ 570,000 sit in the optimal zone — affordable under the new rules but with enough margin to absorb construction cost variability.

Invest in infrastructure due diligence. A unit that is nominally affordable but located in a zone with inadequate roads, schools, or public transit will face chronic absorption problems. Infrastructure timelines must be part of the feasibility analysis, not an afterthought.

Use phased launches to manage absorption risk. Releasing units in tranches allows developers to calibrate pricing to real-time market feedback and avoid the trap of launching an entire project into a market that absorbs more slowly than projected.

Monitor the price-push effect. As experts have noted, MCMV expansion may increase demand pressure and drive property prices upward across the mid-income band. [7] Developers who lock in land and construction costs before this price pressure fully materializes will have a structural cost advantage over later entrants.

For investors interested in exploring current mid-income development opportunities in high-growth corridors, reviewing active real estate developments in markets like Florianopolis provides a practical benchmark for what well-positioned mid-income product looks like in 2026.

Conclusion

The expansion of MCMV in 2026 has moved the policy goalposts in a meaningful direction, but it has not solved the fundamental supply problem that defines Affordable Housing in Brazil Beyond MCMV: Where Mid-Income Demand Is Most Underserved in 2026. Families earning between R$ 4,000 and R$ 13,000 per month now have better financing access than at any point in recent history. What they still lack, in most secondary cities and metropolitan fringes, is sufficient product that is correctly priced, well-located, and matched to their actual lifestyle needs.

The opportunity for developers and investors is real and time-sensitive. Secondary cities with strong employment fundamentals, thin supply pipelines, and growing mid-income populations represent the most compelling entry points. The pricing band between R$ 300,000 and R$ 600,000 is where the next wave of Brazilian real estate value creation will occur — provided that developers maintain pricing discipline, invest in thorough sub-market analysis, and resist the temptation to drift upmarket when construction costs rise.

Actionable next steps for developers and investors:

- Commission sub-market absorption studies in target secondary cities before committing to land acquisition.

- Engage with Caixa Econômica Federal and Banco do Brasil early to understand Faixa 4 financing conditions and documentation requirements for buyers.

- Design unit typologies that meet mid-income functional priorities — efficient floor plans, covered parking, reliable connectivity — rather than luxury amenities that inflate costs without improving absorption.

- Build phased launch strategies that allow pricing recalibration between tranches.

- Track infrastructure investment timelines in target zones as a leading indicator of future absorption rates.

The mid-income housing gap in Brazil is not a problem waiting for a government solution. It is a market opportunity waiting for developers with the discipline to serve it correctly.

References

[1] Novas Regras Do Minha Casa Minha Vida Comecam Valer Nesta Quarta 22 – https://agenciagov.ebc.com.br/noticias/202604/novas-regras-do-minha-casa-minha-vida-comecam-valer-nesta-quarta-22?utm_source=openai

[2] Noticia Mcid N 2100 – https://www.gov.br/cidades/pt-br/assuntos/noticias-1/noticia-mcid-n-2100?utm_source=openai

[3] Mcmv Tera Aumento Dos Limites De Faixas E De Valor Dos Imoveis – https://agenciagov.ebc.com.br/noticias/202603/mcmv-tera-aumento-dos-limites-de-faixas-e-de-valor-dos-imoveis?utm_source=openai

[4] Orcamento Recorde Habitacao Contara Com R 144 5 Bilhoes Do Fgts Em 2026 – https://agenciagov.ebc.com.br/noticias/202511/orcamento-recorde-habitacao-contara-com-r-144-5-bilhoes-do-fgts-em-2026?utm_source=openai

[5] Noticia Mcid N 2073 – https://www.gov.br/cidades/pt-br/assuntos/noticias-1/noticia-mcid-n-2073?utm_source=openai

[6] Noticia Mcid N 2252 – https://www.gov.br/cidades/pt-br/assuntos/noticias-1/noticia-mcid-n-2252?utm_source=openai

[7] Ampliacao Do Minha Casa Minha Vida Deve Aquecer Mercado E Pode Pressionar Precos Dos Imoveis – https://veja.abril.com.br/economia/ampliacao-do-minha-casa-minha-vida-deve-aquecer-mercado-e-pode-pressionar-precos-dos-imoveis/?utm_source=openai

[8] Setor Imobiliario Bate Recordes E Projeta Cenario Mais Favoravel Em 2026 – https://www.cnnbrasil.com.br/economia/macroeconomia/setor-imobiliario-bate-recordes-e-projeta-cenario-mais-favoravel-em-2026/?utm_source=openai