“

The corporate landscape in Brazil is undergoing a dramatic transformation in 2026. As companies seek to reduce operational expenses while maintaining productivity, a strategic shift toward decentralized office hubs is reshaping where businesses locate their back-office functions. Two cities stand out in this movement: Alphaville and Curitiba—both offering compelling cost advantages, robust infrastructure, and attractive yields for developers entering these secondary markets.

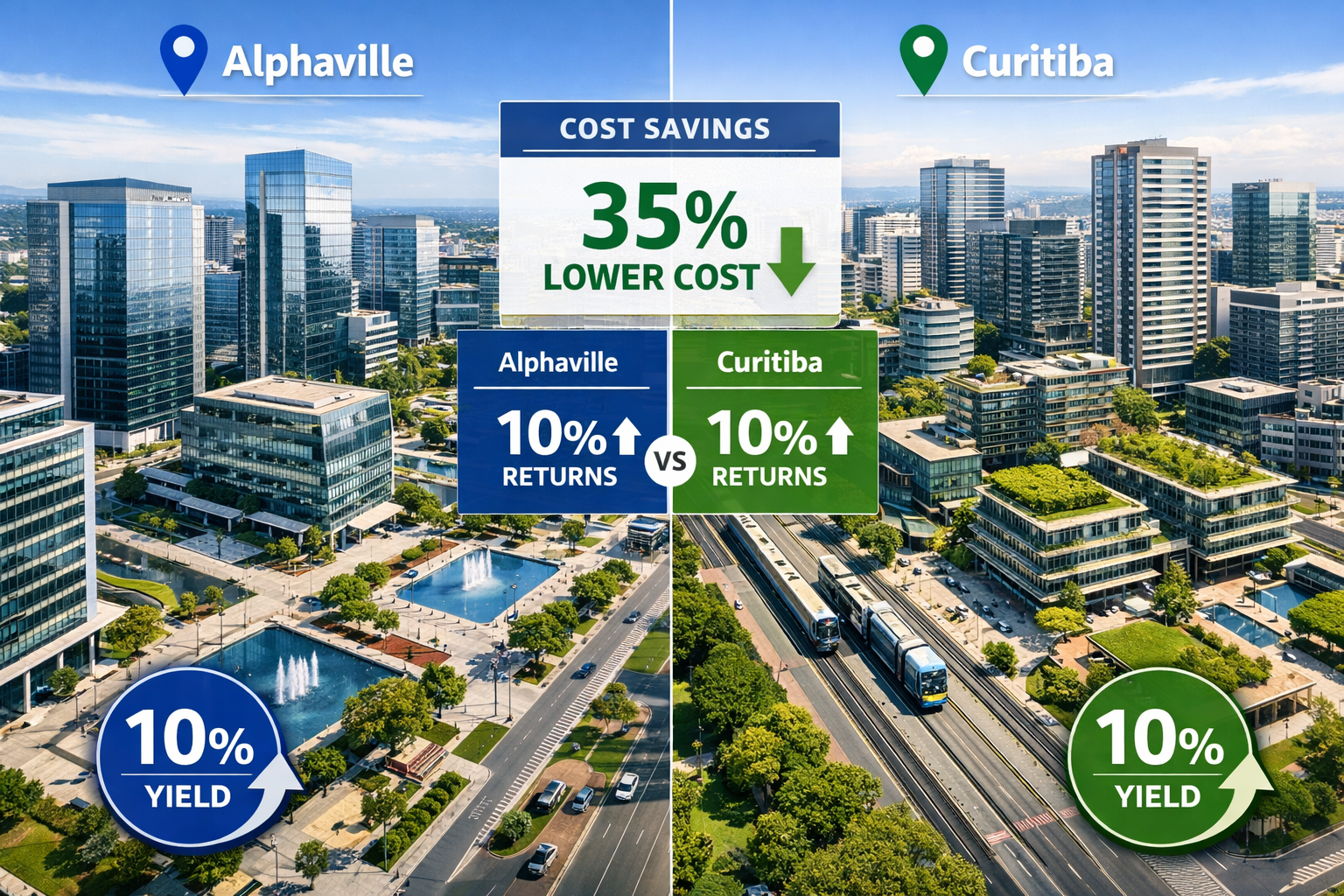

Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization represents more than just a real estate trend. It signals a fundamental rethinking of corporate geography, where support functions migrate from expensive primary markets to affordable, well-connected locations that deliver 10% investment yields while cutting operational costs by 30-40%.

Key Takeaways

- 💼 Cost Reduction: Companies relocating back-office operations to Alphaville and Curitiba achieve 30-40% savings on real estate and labor costs compared to São Paulo and Rio de Janeiro central districts

- 🏗️ Development Boom: Alphaville saw dozens of new towers and logistics centers in 2024-2025, with Barueri ranking among the top construction markets in São Paulo state [1]

- 📊 Investment Yields: Mixed-use office-residential projects in these markets deliver 10% annual yields, significantly outperforming traditional primary market returns

- 🌐 Infrastructure Advantage: Both cities offer superior zoning flexibility, municipal support, and connectivity that make them ideal for corporate expansion

- 🎯 Market Opportunity: Alphaville’s R$17 billion land bank sales potential across 120+ projects demonstrates massive developer opportunities [2]

Understanding the Decentralized Office Hub Movement

Why Corporations Are Shifting Support Functions

The economics of corporate real estate have fundamentally changed. Traditional headquarters in São Paulo’s Avenida Paulista or Rio’s Centro districts command premium rents—often exceeding R$150 per square meter monthly—while offering limited expansion flexibility. Meanwhile, back-office functions such as customer service, data processing, accounting, and human resources don’t require prestigious addresses to deliver value.

This realization has sparked a corporate exodus toward decentralized office hubs where companies can secure:

- Lower occupancy costs (40-60% reduction)

- Abundant talent pools with competitive salary expectations

- Modern facilities built specifically for operational efficiency

- Scalability without the constraints of aging urban infrastructure

The shift mirrors global trends seen in markets like the United States, where companies have moved support operations from Manhattan to Charlotte or from San Francisco to Austin. Brazil’s version centers on Alphaville and Curitiba as the primary beneficiaries.

The Alphaville Advantage: Scale Meets Infrastructure

Alphaville has evolved from a residential community concept into Brazil’s largest community development company, with over 120 projects in development across 23 Brazilian states and a land bank representing approximately R$17 billion in sales potential [2]. This scale creates unique advantages for corporate tenants and developers alike.

The Alphaville area, particularly in Barueri, experienced remarkable construction activity in 2024, with dozens of new towers and logistic centers emerging alongside strong municipal infrastructure investment [1]. Barueri consistently ranks as one of the top construction markets in São Paulo state on a per-resident basis, demonstrating sustained demand and development momentum.

Key infrastructure elements include:

- Direct highway access to São Paulo’s ring roads

- Proximity to major airports (Congonhas and Guarulhos)

- Established telecommunications infrastructure

- Mixed-use zoning that accommodates office-residential integration

- Private security and community management systems

For developers, this represents a mature market with proven demand, established governance, and clear regulatory frameworks—reducing development risk while maintaining attractive returns.

Curitiba’s Strategic Position in Corporate Decentralization

Curitiba brings a different value proposition to the Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization equation. As a state capital with a reputation for urban planning excellence, Curitiba offers:

- Lower labor costs compared to São Paulo (15-25% reduction)

- Quality of life that aids talent retention

- Sustainable urban design that appeals to ESG-conscious corporations

- Business-friendly municipal government with streamlined permitting

Recent developments signal growing corporate interest. The opening of Qoya Hotel Curitiba, Curio Collection by Hilton, with 168 rooms and 690 square meters of flexible meeting space [3], demonstrates the city’s capacity to support business travel and corporate events—essential infrastructure for companies establishing regional operations centers.

The city’s integrated transit system, pedestrian-friendly design, and established technology sector create an ecosystem where back-office operations can thrive without the congestion and costs associated with larger metropolitan areas.

Decentralized Office Hubs 2026: Market Analysis for Alphaville and Curitiba

Cost Optimization Breakdown

Understanding the financial advantages requires examining specific cost categories:

| Cost Category | São Paulo CBD | Alphaville | Curitiba | Savings (Alphaville) | Savings (Curitiba) |

|---|---|---|---|---|---|

| Office Rent (R$/m²/month) | R$150-180 | R$65-85 | R$55-75 | 47-57% | 54-63% |

| Average Salary (Mid-level) | R$8,500 | R$6,800 | R$6,200 | 20% | 27% |

| Parking (per space/month) | R$800 | R$300 | R$250 | 62% | 69% |

| Utilities (per m²/month) | R$18 | R$12 | R$11 | 33% | 39% |

These savings compound significantly for operations requiring 2,000-5,000 square meters—typical for back-office functions supporting 150-400 employees. A company relocating 300 employees to Alphaville can save R$4-6 million annually on real estate and direct labor costs alone.

Investment Yield Analysis for Developers

The 10% yield figure attracting developers to these markets stems from several factors:

Revenue drivers:

- Higher occupancy rates (92-96% vs. 85-88% in primary markets)

- Longer lease terms (5-7 years vs. 3-5 years)

- Triple-net lease structures shifting operating costs to tenants

- Mixed-use premiums from residential components

Cost advantages:

- Land acquisition costs 60-70% lower than prime São Paulo locations

- Construction costs benefiting from competitive local markets

- Faster permitting in business-friendly municipalities

- Lower property taxes in suburban jurisdictions

For developers focused on real estate investment opportunities, these fundamentals create compelling risk-adjusted returns that outperform traditional office developments in saturated primary markets.

Tenant Demand Drivers

Corporate tenants evaluating Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization typically prioritize:

- Operational efficiency: Modern facilities designed for specific functions

- Talent accessibility: Locations where employees can commute without São Paulo’s traffic challenges

- Scalability: Ability to expand operations without relocating

- Technology infrastructure: Fiber connectivity, redundant power, cloud access

- Amenities: On-site services that reduce employee turnover

The most successful developments integrate these elements into mixed-use projects that combine office space with residential units, retail services, and recreational facilities—creating self-contained ecosystems that enhance employee satisfaction while maximizing land value.

Zoning and Infrastructure Analysis for Secondary Market Entry

Navigating Alphaville’s Regulatory Environment

Developers entering the Alphaville market must understand its unique governance structure. Unlike traditional municipalities, Alphaville operates through master-planned communities with private governance overlaying municipal regulations from Barueri and surrounding cities.

Key zoning considerations:

- Mixed-use designations: Most Alphaville zones permit combined office-residential development, enabling higher land utilization

- FAR (Floor Area Ratio) allowances: Typically 2.5-4.0 in commercial zones, supporting mid-rise development

- Parking requirements: Generally 1 space per 35m² of office space, plus residential requirements

- Setback regulations: Vary by zone but typically require 5-10m from property lines

- Height restrictions: Usually 15-25 stories depending on proximity to residential areas

The private governance layer adds requirements around architectural standards, landscaping, and community integration that can increase development costs by 8-12% but also protect property values and ensure consistent quality—ultimately benefiting long-term yields.

Municipal infrastructure investment in Barueri has accelerated, with improvements to major arterials, expansion of water and sewage capacity, and enhanced public transit connections. These investments reduce infrastructure burden on developers while improving asset accessibility—critical factors for corporate tenants evaluating locations.

Curitiba’s Planning Framework

Curitiba’s reputation for urban planning excellence translates into a more structured but predictable development environment. The city’s Master Plan designates specific corridors for high-density mixed-use development, particularly along the Bus Rapid Transit (BRT) lines.

Development advantages in Curitiba:

- Transit-oriented development incentives: FAR bonuses (up to 6.0) for projects near BRT stations

- Streamlined environmental review: Established processes for developments meeting sustainability criteria

- Infrastructure readiness: Existing capacity in target development zones

- Clear timeline expectations: Permitting typically completed in 6-9 months for compliant projects

The city actively courts corporate development through its economic development office, which provides site selection assistance, regulatory guidance, and sometimes tax incentives for projects creating significant employment.

For developers, this means lower regulatory risk and more predictable project timelines compared to São Paulo’s complex, often unpredictable approval processes. Projects that align with the city’s sustainability goals—incorporating green building standards, transit connectivity, and mixed-use design—receive preferential treatment.

Infrastructure Requirements for Back-Office Developments

Successful back-office facilities in decentralized hubs require specific infrastructure elements:

Technology infrastructure:

- Redundant fiber connectivity (minimum 10Gbps capacity)

- On-site data center space or cloud connectivity

- Backup power systems (N+1 redundancy minimum)

- Advanced HVAC for equipment rooms

Physical infrastructure:

- Open floor plates (minimum 800m² contiguous space)

- Column spacing supporting flexible layouts (8-10m typical)

- Floor loading capacity for dense equipment areas (600-800 kg/m²)

- Adequate elevator capacity (1 elevator per 4,000m² occupied space)

Amenity infrastructure:

- On-site or nearby food service

- Fitness facilities (increasingly expected)

- Secure parking with EV charging capacity

- Outdoor spaces for breaks and informal meetings

Both Alphaville and Curitiba offer locations where these requirements can be met cost-effectively. The construction boom in Alphaville [1] has created competitive contractor markets and established supply chains for specialized building systems. Curitiba’s planning framework ensures that infrastructure capacity exists in designated development zones.

Development Strategies for Mixed-Use Office-Residential Projects

Optimizing the Office-Residential Mix

The most successful projects in the Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization trend carefully balance office and residential components to maximize both financial returns and tenant satisfaction.

Typical successful ratios:

- 60% office / 40% residential: Maximizes office revenue while providing housing for key employees

- 50% office / 50% residential: Balanced approach creating true live-work communities

- 70% office / 30% residential: Office-focused with residential as amenity/retention tool

The residential component serves multiple strategic purposes:

- Employee housing: Reduces commute burden, particularly for shift workers in 24/7 operations

- Yield enhancement: Residential units often achieve higher per-square-meter returns

- Activity diversification: Creates evening/weekend activity supporting retail tenants

- Risk mitigation: Diversifies tenant base across corporate and individual lessees

Projects incorporating residential elements typically command 5-8% rent premiums on office space due to enhanced amenities and live-work convenience. This premium, combined with residential rental income, drives the 10% overall yield that makes these developments attractive.

Phasing Strategies for Large-Scale Developments

Given the scale of opportunity—Alphaville alone represents R$17 billion in land bank potential [2]—successful developers employ phased development strategies that manage risk while capturing market growth.

Recommended phasing approach:

Phase 1 (Years 1-2):

- Develop initial office component (15,000-25,000m²)

- Establish anchor tenant relationship (pre-lease 60-70%)

- Build core infrastructure serving future phases

- Create initial amenity package

Phase 2 (Years 2-4):

- Add residential component (100-150 units)

- Expand office space based on Phase 1 absorption

- Enhance amenities (fitness center, food service)

- Develop retail/service component

Phase 3 (Years 4-6):

- Complete build-out to master plan capacity

- Add premium office space commanding higher rents

- Integrate additional residential towers

- Establish full mixed-use ecosystem

This approach allows developers to validate market assumptions with Phase 1 before committing full capital, while creating momentum that supports premium pricing in later phases. It also aligns with corporate tenant needs—many companies prefer to start smaller and expand as they validate the decentralized location strategy.

Sustainability and ESG Considerations

Corporate tenants increasingly evaluate locations through Environmental, Social, and Governance (ESG) criteria. Developments incorporating sustainability features command premium rents and achieve higher occupancy rates.

High-value sustainability features:

- LEED or AQUA certification (10-15% rent premium)

- Solar power generation (reduces operating costs, appeals to ESG mandates)

- Rainwater harvesting and greywater systems

- Native landscaping reducing water and maintenance requirements

- Bicycle infrastructure and EV charging

Curitiba’s planning framework particularly rewards sustainable design, with FAR bonuses and expedited permitting for certified green buildings. The city’s existing reputation for environmental leadership makes it attractive to companies with strong ESG commitments.

Alphaville’s private governance structure increasingly incorporates sustainability standards, with newer developments required to meet energy efficiency benchmarks and incorporate green space ratios that exceed municipal minimums.

For developers, the incremental cost of sustainability features (typically 5-8% of construction budget) is more than offset by higher rents, faster lease-up, and longer tenant retention—ultimately improving overall project returns while future-proofing assets against evolving corporate requirements.

Financial Modeling and Risk Assessment

Pro Forma Analysis for Typical Projects

Understanding the financial mechanics of Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization requires examining realistic project economics.

Sample project (Alphaville, 30,000m² mixed-use):

Development Costs:

- Land acquisition: R$12 million

- Hard costs (construction): R$85 million

- Soft costs (design, permits, financing): R$18 million

- Total Development Cost: R$115 million

Revenue (Stabilized Year 3):

- Office space (18,000m² @ R$75/m²/month): R$16.2 million/year

- Residential (120 units @ R$3,500/month average): R$5.04 million/year

- Retail/parking: R$1.8 million/year

- Total Annual Revenue: R$23.04 million

Operating Expenses:

- Property management, maintenance, utilities: R$6.9 million/year

- Net Operating Income: R$16.14 million

Yield Calculation:

- NOI / Total Development Cost = 16.14 / 115 = 14.0% yield

This example demonstrates how well-executed projects can exceed the 10% yield benchmark, particularly when achieving strong occupancy and efficient operations. The mixed-use component is critical—a pure office project would generate approximately 11-12% yield under similar assumptions.

Risk Factors and Mitigation Strategies

Developers must address several risk categories when entering these secondary markets:

Market Risk:

- Concern: Corporate demand may not materialize at projected levels

- Mitigation: Pre-lease minimum 40-50% before construction start; focus on multi-tenant rather than single-tenant developments

Construction Risk:

- Concern: Cost overruns or delays affecting returns

- Mitigation: Fixed-price contracts with experienced local contractors; adequate contingency (12-15% in current market)

Regulatory Risk:

- Concern: Zoning changes or permit delays

- Mitigation: Engage with municipalities early; structure projects within existing approved frameworks; consider working with experienced local developers

Economic Risk:

- Concern: Macroeconomic downturn reducing corporate expansion

- Mitigation: Conservative leverage (60% LTV maximum); diversified tenant base; flexible space design allowing alternative uses

Competition Risk:

- Concern: Oversupply from multiple developers pursuing same opportunity

- Mitigation: Differentiation through amenities, sustainability, or specialized design; relationships with corporate real estate decision-makers

The most successful developers in these markets combine conservative financial assumptions with operational excellence in property management—recognizing that achieving projected yields requires not just successful development but also effective long-term asset management.

Corporate Tenant Perspectives and Requirements

What Companies Look for in Decentralized Hubs

Understanding tenant requirements is essential for developers designing projects in the Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization market. Corporate real estate decisions involve multiple stakeholders with different priorities:

CFO/Finance priorities:

- Total occupancy cost reduction (30-40% target)

- Lease flexibility for business volatility

- Predictable operating expenses

- Favorable lease terms (rent escalation, renewal options)

Operations priorities:

- Space efficiency and layout flexibility

- Technology infrastructure reliability

- Expansion capacity within same location

- 24/7 access and security

HR priorities:

- Employee commute accessibility

- Amenities supporting retention

- Quality work environment

- Nearby housing options for key staff

Facilities priorities:

- Modern building systems

- Energy efficiency

- Adequate parking

- Reliable HVAC and power

Projects that address all stakeholder priorities achieve faster lease-up and longer tenant retention—critical factors for achieving projected yields. The most successful developments involve early engagement with potential anchor tenants, allowing design customization that secures long-term commitments.

Emerging Trends in Back-Office Space Design

The nature of back-office work continues evolving, influencing space requirements:

Activity-based working: Rather than assigned desks, spaces designed for specific activities (focused work, collaboration, video conferencing) with flexible allocation

Hybrid work accommodation: Reduced density (150-180 square feet per employee vs. traditional 100-120) to accommodate rotating schedules

Wellness integration: Natural light, air quality systems, biophilic design elements that reduce stress and improve productivity

Technology integration: Seamless video conferencing, hot-desking management systems, occupancy sensors optimizing space utilization

These trends favor newer developments in Alphaville and Curitiba over retrofitted older buildings in primary markets—creating competitive advantages for purpose-built facilities in decentralized hubs.

Similar to trends observed in other growing Brazilian markets, the shift toward quality over location prestige is reshaping corporate real estate strategies nationwide.

Implementation Roadmap for Developers

Market Entry Strategy

Developers considering entry into the Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization market should follow a structured approach:

Step 1: Market Validation (3-6 months)

- Conduct tenant demand research with corporate real estate brokers

- Analyze competitive supply and absorption rates

- Identify specific submarkets with infrastructure advantages

- Assess regulatory environment and approval timelines

Step 2: Site Selection (2-4 months)

- Evaluate sites based on transit connectivity, zoning, and infrastructure

- Conduct preliminary feasibility analysis

- Engage with municipalities on development framework

- Secure site control (option or acquisition)

Step 3: Project Design (4-6 months)

- Develop conceptual design addressing tenant requirements

- Engage anchor tenant prospects for input and pre-leasing

- Finalize mixed-use ratio and phasing strategy

- Complete detailed financial modeling

Step 4: Entitlements (6-12 months)

- Submit permit applications

- Navigate environmental and zoning approvals

- Secure necessary infrastructure commitments

- Finalize anchor tenant lease agreements

Step 5: Financing and Construction (18-24 months)

- Secure construction and permanent financing

- Execute construction contracts

- Implement project management and quality control

- Begin marketing to additional tenants

Step 6: Lease-up and Stabilization (12-18 months)

- Complete building and obtain occupancy permits

- Tenant improvement construction

- Tenant move-ins and building commissioning

- Achieve stabilized occupancy (90%+)

This timeline totals approximately 4-5 years from initial market entry to stabilized operations—consistent with large-scale mixed-use development in secondary markets. Developers with existing market presence or partnerships can compress timelines by 6-12 months.

Partnership Opportunities

Given the complexity of mixed-use development in secondary markets, strategic partnerships often accelerate success:

Local development partners: Provide market knowledge, municipal relationships, and regulatory navigation expertise

Corporate real estate advisors: Connect developers with tenant demand and provide market intelligence

Institutional capital partners: Provide scale capital for larger projects while sharing risk

Property management firms: Ensure operational excellence critical to achieving projected yields

Developers should evaluate partnership structures that align incentives while preserving control over critical decisions affecting project quality and financial performance. The most successful partnerships clearly define roles, decision rights, and economic participation from project inception.

For those interested in exploring development opportunities in emerging Brazilian markets, understanding local partnership dynamics is essential to successful execution.

Future Outlook: Beyond 2026

Market Evolution Scenarios

The Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization trend will likely evolve through several potential scenarios:

Scenario 1: Accelerated Adoption (60% probability)

- Corporate cost pressures intensify decentralization

- Additional secondary markets emerge (Campinas, Joinville, Ribeirão Preto)

- Primary market office values decline 15-25%

- Decentralized hub yields compress to 8-9% as competition increases

Scenario 2: Steady Growth (30% probability)

- Moderate pace of corporate relocation continues

- Alphaville and Curitiba maintain market leadership

- Yields stabilize around 9-10%

- Hybrid work models reduce overall office demand but favor quality space

Scenario 3: Reversal (10% probability)

- Economic recovery and corporate culture shifts favor headquarters concentration

- Remote work reduces need for satellite offices

- Development slows in secondary markets

- Yields rise as occupancy softens

Most market participants anticipate Scenario 1, with corporate cost optimization remaining a priority regardless of economic conditions. The infrastructure investments already underway in Alphaville [1] and Curitiba’s continued urban development suggest sustained momentum.

Emerging Secondary Markets

While Alphaville and Curitiba lead the current trend, several additional markets show potential for back-office development:

Campinas: Strong university talent pipeline, proximity to São Paulo, established technology sector

Joinville: Manufacturing base creating demand for corporate support functions, lower costs than Curitiba

Ribeirão Preto: Agribusiness hub with growing service sector, excellent quality of life

Florianópolis: Technology sector growth, quality of life advantages, though higher costs than other secondary markets

Developers establishing successful models in Alphaville and Curitiba can potentially replicate these approaches in emerging markets, capturing first-mover advantages before competition intensifies. Understanding regional market dynamics becomes increasingly important as the decentralization trend expands geographically.

Technology’s Impact on Back-Office Location Decisions

Advancing technology will continue reshaping corporate location strategies:

Artificial Intelligence: Automation of routine back-office tasks may reduce overall space requirements while increasing demand for specialized technical facilities

5G and connectivity: Enables more geographic flexibility, potentially benefiting secondary markets with strong infrastructure

Virtual collaboration tools: Reduces need for proximity to headquarters, supporting further decentralization

Data sovereignty regulations: May require in-country data processing facilities, creating demand for secure back-office locations

These technological trends generally favor the decentralization thesis, as they reduce the importance of physical proximity while increasing the value of cost optimization and quality infrastructure—exactly what Alphaville and Curitiba offer.

Conclusion

The emergence of Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization represents a fundamental shift in Brazilian corporate real estate strategy. Companies facing persistent cost pressures are discovering that back-office functions can operate effectively—and more economically—outside expensive primary markets.

For corporations, the value proposition is compelling: 30-40% cost reductions while maintaining or improving operational effectiveness. The infrastructure investments in Alphaville [1], with its R$17 billion development pipeline [2], and Curitiba’s business-friendly environment, including recent hospitality expansions [3], provide the foundation for successful decentralization strategies.

For developers and investors, these markets offer 10% yields through well-executed mixed-use projects that combine office and residential components. The key success factors include:

✅ Strategic site selection prioritizing infrastructure and connectivity

✅ Mixed-use design maximizing land value and creating live-work ecosystems

✅ Sustainability integration meeting corporate ESG requirements

✅ Anchor tenant pre-leasing validating demand before construction

✅ Operational excellence in property management delivering projected returns

The trend extends beyond simple cost arbitrage. It reflects evolving work patterns, technology enablement, and corporate recognition that location prestige matters less for support functions than operational efficiency and employee quality of life.

Actionable Next Steps

For Corporate Real Estate Decision-Makers:

- Conduct detailed cost-benefit analysis comparing current locations with Alphaville/Curitiba alternatives

- Visit existing back-office facilities in these markets to assess employee experience

- Engage commercial real estate brokers specializing in these markets

- Pilot smaller operations (50-100 employees) before full-scale relocation

- Contact local development experts to explore available options

For Developers and Investors:

- Commission market feasibility studies for specific submarkets within Alphaville and Curitiba

- Establish relationships with corporate real estate advisors to understand tenant demand

- Evaluate partnership opportunities with local developers and operators

- Analyze zoning and infrastructure in target development areas

- Develop preliminary financial models testing sensitivity to key assumptions

- Consider broader Brazilian real estate investment strategies to diversify portfolio risk

The Decentralized Office Hubs 2026: Alphaville and Curitiba Back-Office Developments for Cost Optimization opportunity is substantial, but success requires careful planning, market understanding, and execution excellence. Those who move decisively while maintaining disciplined underwriting will capture the most attractive opportunities in this transformative market trend.

The future of Brazilian corporate real estate is increasingly decentralized—and the time to participate is now. 🚀

References

[1] Top 30 Brazilian Cities Leading The Construction Boom 2024 2025 – https://www.scribd.com/document/963975851/Top-30-Brazilian-Cities-Leading-the-Construction-Boom-2024-2025

[2] Alphaville – https://matrixbcg.com/blogs/owners/alphaville

[3] Hilton Expansion Brazil Debut Of Curio Collection By Hilton Brand – https://stories.hilton.com/releases/hilton-expansion-brazil-debut-of-curio-collection-by-hilton-brand