As 2026 unfolds, Latin America’s housing markets face an unprecedented convergence of opportunity and uncertainty. With Mexico’s presidential election cycle intersecting with $61.43 billion in housing investments and Brazil’s continued MCMV (Minha Casa Minha Vida) expansion, developers and investors must navigate a landscape where political transitions can reshape fiscal commitments overnight. Understanding Election Year Fiscal Risks 2026: Stress-Testing Housing Pipelines Amid MCMV and Reforma Investments has become essential for anyone with capital deployed in the region’s residential construction sector.

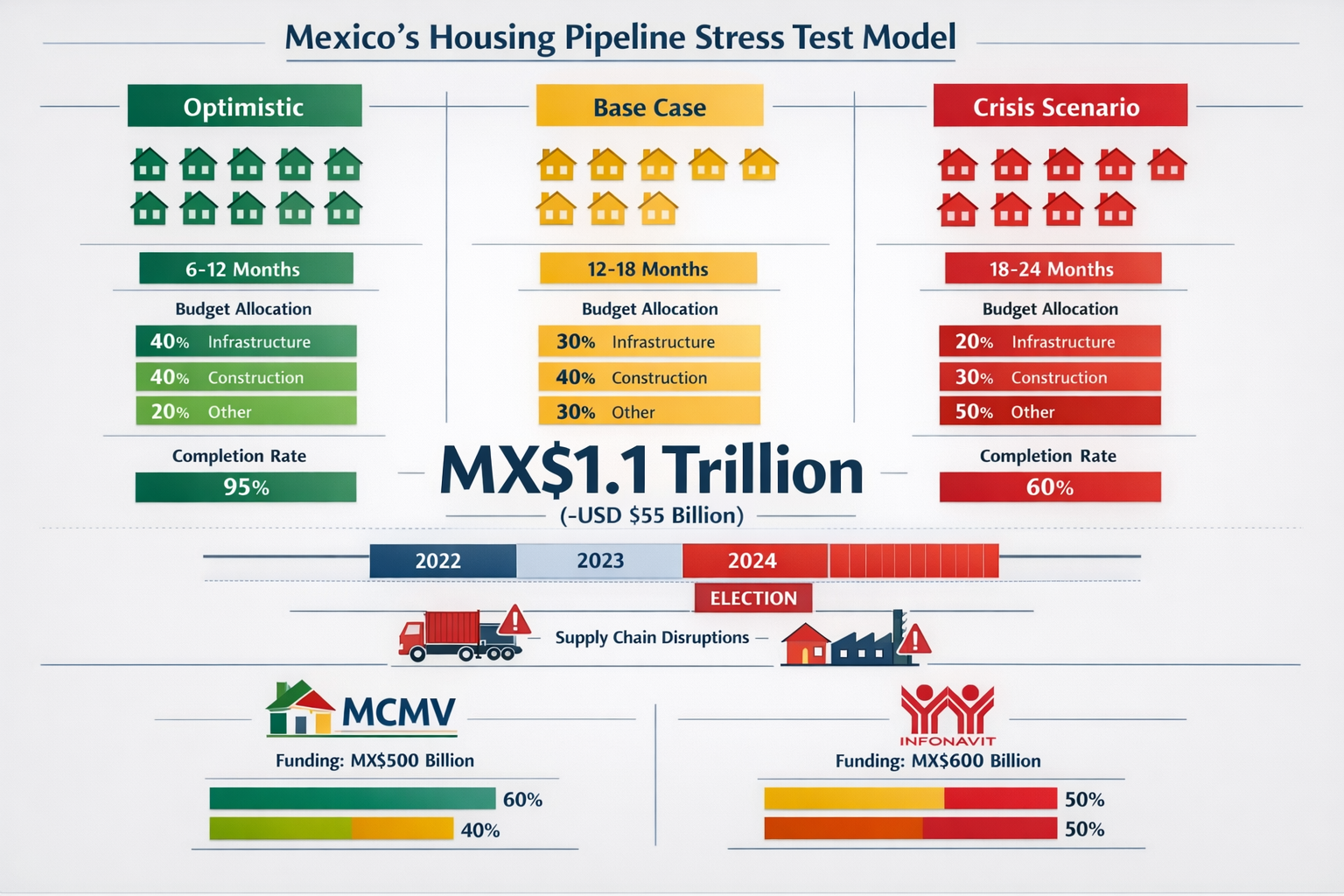

Mexico’s ambitious Housing for Well-being program targets over 400,000 homes in 2026, backed by MX$1.1 trillion in commitments[1]. Yet this massive pipeline launches against a backdrop of construction sector contraction, supply chain fragmentation, and the inherent volatility that election years bring to public spending priorities. Meanwhile, Brazil’s housing initiatives continue to evolve, creating parallel opportunities and risks across the continent’s two largest economies.

Key Takeaways

- 🏗️ Mexico’s housing pipeline faces election-year stress with MX$1.1 trillion ($61.43B) committed to 1.8 million homes amid a 3.6% construction sector contraction in 2025[1][2]

- 📊 Supply chain coordination gaps are creating 10-20% cost increases through payment delays and capital flow asymmetries, threatening project viability[2]

- 🗳️ Political transition risks require stress-testing housing investments across optimistic, base case, and crisis scenarios to protect portfolio returns

- 💡 Resilient investment strategies include geographic diversification, phased capital deployment, and focusing on best places to invest in Brazil property with stable fundamentals

- 🎯 Recovery projections suggest 2.6% average annual construction growth from 2026-2029, driven by nearshoring and industrial development[2]

Understanding the 2026 Housing Investment Landscape

The Scale of Current Commitments

The Sheinbaum administration has scaled Mexico’s housing ambitions to address a staggering 8.38 million-home expanded housing backlog as of 2024[1]. This deficit has grown even as annual construction remains far below 2015 levels, creating both urgent need and significant execution risk.

The numbers are substantial:

| Program Component | Target/Investment | Timeline |

|---|---|---|

| Total homes planned | 1.8 million units | Multi-year |

| 2026 construction target | 400,000+ homes | Current year |

| Total investment | MX$1.1 trillion ($61.43B) | Ongoing |

| Families to benefit | Nearly 8 million | Program duration |

| Current housing deficit | 8.38 million homes | As of 2024 |

These commitments involve major INFONAVIT contracting, delivery acceleration, and loan-restructuring initiatives designed to unlock both supply and demand simultaneously[1]. However, the execution of such ambitious targets during an election year introduces variables that prudent investors must model carefully.

Election Year Fiscal Dynamics

Election years historically create fiscal uncertainty in Latin American markets. Government priorities can shift rapidly, budget allocations face political pressures, and implementation timelines often extend as administrations transition. For housing investments specifically, this manifests in several ways:

Budget reallocation risks emerge as incoming administrations reassess predecessor commitments. While Mexico’s 2026 housing targets enjoy current political support, the post-election landscape could alter funding priorities, especially if economic conditions deteriorate or competing infrastructure needs arise.

Implementation velocity typically slows during transition periods. The construction activity data already shows this pattern—while building growth rose 1.6% month-over-month in November 2025, civil engineering experienced sharp slumps tied to weaker public investment[1]. This divergence illustrates how political cycles impact different construction segments unevenly.

Regulatory changes often accompany new administrations, potentially affecting permitting timelines, environmental requirements, or financing structures. Investors in real estate development projects must anticipate these shifts when projecting completion schedules and exit strategies.

Stress-Testing Housing Pipelines: Scenario Modeling for Election Year Fiscal Risks 2026

Sophisticated investors approach Election Year Fiscal Risks 2026: Stress-Testing Housing Pipelines Amid MCMV and Reforma Investments through rigorous scenario analysis. Rather than relying on single-point forecasts, resilient portfolios incorporate multiple outcome pathways.

Scenario 1: Optimistic Continuation

In this best-case scenario, political transitions occur smoothly, fiscal commitments remain intact, and the projected 2.6% average annual construction growth from 2026-2029 materializes as forecast[2]. Key assumptions include:

- Full funding delivery for the 400,000-home 2026 target

- Successful coordination improvements reducing the current 10-20% cost overruns[2]

- Nearshoring momentum continuing to drive complementary infrastructure investment

- Credit relief programs expanding as planned to unlock demand

Under this scenario, early-stage investments in housing pipelines deliver strong returns as supply meets pent-up demand. Projects positioned in high-growth regions benefit from both program support and organic market appreciation.

Scenario 2: Base Case with Delays

A more conservative base case incorporates moderate political friction and implementation delays. This scenario assumes:

- 60-75% delivery of stated 2026 housing targets

- Continued supply chain coordination challenges maintaining 10-15% cost premiums

- Selective program continuation with some budget reallocation

- Regional variation in execution, with some markets outperforming others

This scenario requires investors to build timing buffers into their underwriting models. Projects with longer development horizons face greater exposure to shifting priorities, while those nearing completion benefit from momentum and sunk-cost dynamics that discourage abandonment.

The construction sector’s recent performance supports this middle-ground view—the 3.6% contraction in 2025 followed by projected recovery suggests neither catastrophic failure nor seamless execution[2].

Scenario 3: Crisis Disruption

The pessimistic scenario models significant fiscal retrenchment driven by economic stress, political upheaval, or external shocks. Assumptions include:

- Major budget cuts reducing housing program funding by 40%+

- Widespread project delays or cancellations

- Supply chain disruptions intensifying cost pressures beyond 20%

- Credit market tightening limiting buyer financing options

While this scenario represents tail risk rather than base probability, its impact would be severe. Investors with concentrated exposure to government-dependent housing programs would face substantial losses. This underscores the importance of diversification strategies that balance program-dependent projects with market-rate developments in stable locations.

Interestingly, cryptocurrency adoption in real estate offers one potential hedge against traditional fiscal disruption, though with its own volatility considerations.

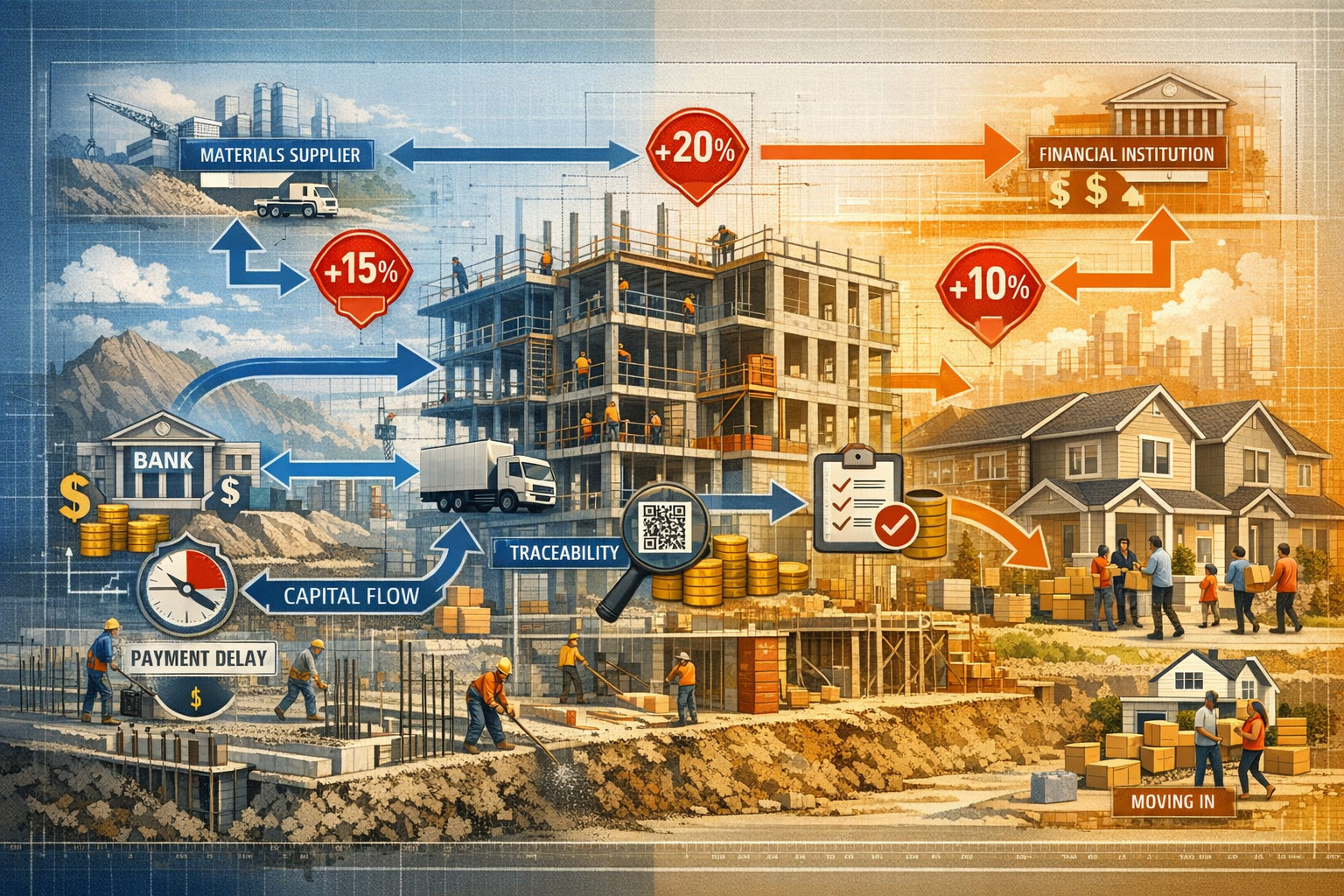

Supply Chain Fragmentation and Cost Management Challenges

Beyond political risks, Election Year Fiscal Risks 2026: Stress-Testing Housing Pipelines Amid MCMV and Reforma Investments must account for operational realities that threaten project economics regardless of government stability.

The Coordination Crisis

Mexico’s construction sector faces what industry analysts describe as a coordination crisis—where financial and commercial systems lag behind technological capabilities[2]. This manifests in several problematic ways:

Deferred payment structures create cash flow mismatches that ripple through supply chains. When developers delay payments to suppliers awaiting government disbursements, material providers must either absorb carrying costs or pass them forward as price increases. These delays can increase project costs by 10% to 20%[2], eroding margins that underwriting models assumed.

Lack of traceability prevents efficient capital allocation. Without standardized data systems tracking materials, labor, and progress, institutional investors struggle to assess true project status. This information asymmetry increases risk premiums and can trigger funding holdbacks that further delay completion.

Asymmetric capital flows disadvantage smaller participants. Large developers with strong balance sheets can weather payment delays and negotiate favorable terms, while smaller contractors face liquidity crunches that force project abandonment or distressed asset sales.

Cost Mitigation Strategies

Forward-thinking developers are implementing several tactics to manage these supply chain risks:

- Pre-purchasing critical materials to lock in pricing and ensure availability

- Establishing direct supplier relationships that bypass fragmented intermediaries

- Implementing digital tracking systems to improve traceability and milestone verification

- Structuring milestone-based financing that aligns capital releases with verified progress

- Building contingency buffers of 15-25% into project budgets to absorb coordination costs

These strategies require upfront capital and operational sophistication, creating competitive advantages for well-capitalized developers while pressuring marginal participants. For investors, this suggests focusing on experienced development teams with proven execution capabilities rather than chasing the highest projected returns from unproven operators.

Geographic Diversification: Brazil’s Parallel Opportunities

While Mexican housing programs dominate current headlines, prudent portfolio construction requires geographic diversification to mitigate country-specific political risks. Brazil’s MCMV program and broader real estate market offer complementary exposure with different risk profiles.

Brazil’s Housing Market Fundamentals

Brazil’s residential market benefits from several structural advantages:

- Demographic demand from urbanization and household formation

- Regional variation allowing selective market entry based on local fundamentals

- Less concentrated political risk with housing policy distributed across federal, state, and municipal levels

- Established legal frameworks for property rights and foreclosure procedures

Markets like Florianópolis demonstrate how local infrastructure development and quality of life factors can drive sustained appreciation independent of national housing programs. This organic demand provides downside protection that purely program-dependent projects lack.

MCMV Program Dynamics

Brazil’s Minha Casa Minha Vida program operates differently from Mexico’s centralized approach, creating distinct risk-return characteristics:

- Subsidy structures target specific income bands with varying government support levels

- Private sector participation is more established, with mature financing and construction ecosystems

- Regional implementation varies by state capacity and local market conditions

Investors can access MCMV-adjacent opportunities through partnerships with established developers or by focusing on market-rate projects in MCMV-supported locations where infrastructure improvements create spillover benefits.

Portfolio Allocation Considerations

A resilient Latin American housing portfolio might allocate:

- 40-50% to Brazilian market-rate developments in high-growth secondary cities

- 25-35% to Mexican program-supported projects with strong completion momentum

- 15-25% to diversified real estate funds providing broader sector exposure

- 5-10% to opportunistic distressed asset acquisitions during market dislocations

This allocation balances growth potential from Mexico’s massive housing push against the stability of Brazil’s more mature market dynamics. The specific weighting should reflect individual risk tolerance, liquidity needs, and market access capabilities.

Building Resilient Investment Portfolios Amid Political Uncertainty

Translating scenario analysis into actionable investment strategy requires systematic approaches to Election Year Fiscal Risks 2026: Stress-Testing Housing Pipelines Amid MCMV and Reforma Investments.

Tactical Portfolio Adjustments for 2026

Timing optimization becomes critical in election years. Investors should consider:

- Accelerating exits on projects nearing completion before potential policy shifts

- Delaying new commitments until post-election policy clarity emerges

- Staging capital deployment with milestone-based releases rather than upfront funding

- Negotiating flexible terms that allow repositioning if scenarios deteriorate

These tactics preserve optionality—the ability to adapt as political and economic conditions evolve. While they may sacrifice some upside in optimistic scenarios, they provide crucial downside protection in crisis cases.

Due Diligence Intensification

Standard due diligence processes must expand to address election-year specific risks:

Political risk assessment should evaluate:

- Developer relationships with current and potential future administrations

- Project dependency on specific government programs versus market demand

- Regulatory approval status and vulnerability to policy reversal

- Geographic exposure to politically contested regions

Financial stress testing must model:

- Impact of 20-40% budget cuts on project completion timelines

- Developer liquidity to weather 6-12 month payment delays

- Buyer financing availability under tightened credit conditions

- Exit market liquidity during potential distressed selling periods

Operational contingency planning requires:

- Alternative supplier identification for critical materials

- Workforce scalability to adjust to changing timelines

- Permit and approval redundancy to avoid single-point regulatory failures

- Currency hedging strategies for cross-border investments

Monitoring and Adaptation Frameworks

Static investment strategies fail in volatile environments. Successful investors implement dynamic monitoring frameworks that trigger predetermined responses as conditions change:

Early warning indicators might include:

- Government budget announcements showing housing allocation changes

- Construction permit issuance velocity in target markets

- Credit availability metrics from major housing lenders

- Political polling data suggesting administration changes

Response protocols should specify:

- Thresholds triggering portfolio rebalancing

- Pre-negotiated exit options with co-investors or developers

- Hedging instruments to deploy if specific risks materialize

- Communication cadences with portfolio managers and advisors

This systematic approach transforms scenario analysis from theoretical exercise into operational reality, ensuring that stress-testing actually improves portfolio resilience rather than merely documenting potential problems.

Learning from Market Leaders

Examining how successful developers navigate market volatility provides practical insights for investment strategy. Key patterns include:

- Diversified project pipelines spanning multiple price points and geographies

- Strong pre-sales requirements before construction commencement

- Conservative leverage ratios maintaining financial flexibility

- Proven execution track records demonstrating ability to complete projects on time and budget

Investors should seek exposure to these characteristics rather than chasing maximum leverage or aggressive timelines that amplify election-year risks.

Conclusion: Navigating 2026’s Housing Investment Landscape

Election Year Fiscal Risks 2026: Stress-Testing Housing Pipelines Amid MCMV and Reforma Investments represents more than an academic exercise—it’s an essential framework for protecting capital and identifying opportunities in one of Latin America’s most dynamic sectors. With $61.43 billion committed to Mexican housing programs and parallel investments across Brazil, the stakes for getting this analysis right have never been higher.

The convergence of massive housing deficits, ambitious government programs, and political transition creates a complex risk-return environment. While Mexico’s 8.38 million-home backlog represents genuine need and substantial opportunity, the path from commitment to completion winds through supply chain challenges, fiscal uncertainties, and coordination gaps that can inflate costs by 10-20% or more[1][2].

Actionable Next Steps

For active investors:

- Conduct scenario analysis on existing housing pipeline exposure using the three-scenario framework outlined above

- Assess geographic concentration and consider rebalancing toward diversified Brazilian markets if over-weighted to Mexican program-dependent projects

- Review developer partnerships to ensure operational capabilities match execution requirements

- Establish monitoring systems with clear triggers for portfolio adjustments

- Build liquidity reserves to weather potential payment delays or take advantage of distressed opportunities

For prospective investors:

- Wait for post-election clarity before committing to long-duration projects heavily dependent on government programs

- Focus on near-completion projects with established momentum and reduced execution risk

- Prioritize market-rate developments in locations with organic demand drivers independent of subsidies

- Partner with experienced local operators who have navigated previous political cycles successfully

- Start with smaller allocations that allow learning before scaling exposure

For all market participants:

- Stay informed on policy developments through reliable sources and local market intelligence

- Network with other investors to share insights and identify emerging risks or opportunities

- Consider professional advice from advisors with specific Latin American housing market expertise

- Maintain flexibility in capital deployment and exit strategies

- Focus on fundamentals rather than chasing headline returns that may not materialize

The Latin American housing sector’s long-term fundamentals remain compelling—demographic growth, urbanization, and massive supply deficits ensure sustained demand for decades. However, the path forward in 2026 requires navigating near-term political and operational challenges with clear-eyed realism and systematic risk management.

By stress-testing portfolios across multiple scenarios, diversifying geographic exposure, and maintaining operational flexibility, investors can position themselves to weather election-year volatility while capturing the substantial opportunities that Mexico’s housing push and Brazil’s continued development represent. The question isn’t whether to participate in this growth story, but how to do so with resilience and discipline that protects capital while pursuing attractive returns.

For those seeking stable, professionally managed real estate opportunities in Brazil’s growing markets, exploring established development projects with proven track records offers a balanced approach to Latin American housing exposure without excessive concentration in election-year fiscal risks.

References

[1] Mexico Launches Attrapi Housing Scales Weekly Roundup – https://mexicobusiness.news/infrastructure/news/mexico-launches-attrapi-housing-scales-weekly-roundup

[2] Mexican Construction In 2026 The Challenge Is Not Growth Its Coordination 302694286 – https://www.prweb.com/releases/mexican-construction-in-2026-the-challenge-is-not-growth-its-coordination-302694286.html