ESG clauses are no longer a negotiating footnote in São Paulo’s premium office leases — they are the headline term. Green certifications have shifted from a developer marketing tool to a binding lease standard, and the financial evidence is unambiguous: certified Grade A towers in Faria Lima and Juscelino Kubitschek (JK) are commanding rental premiums of up to 15% over non-certified peers, while non-certified fringe CBD towers sit at vacancy rates above 15% [1][2]. Understanding ESG compliance as a rental premium driver — and how green certifications are commanding 15% price premiums in São Paulo’s Grade A office market in 2026 — is now essential intelligence for every developer, investor, and institutional tenant operating in Brazil’s commercial real estate sector.

Key Takeaways 📌

- 🟢 Green-certified Grade A offices in São Paulo are achieving 10–15% rental premiums over non-certified equivalents, backed by BloombergNEF data and Cushman & Wakefield market analysis.

- 🏢 Less than 30% of existing office stock meets current LEED or EDGE certification thresholds, creating a structural supply shortage that sustains premium pricing.

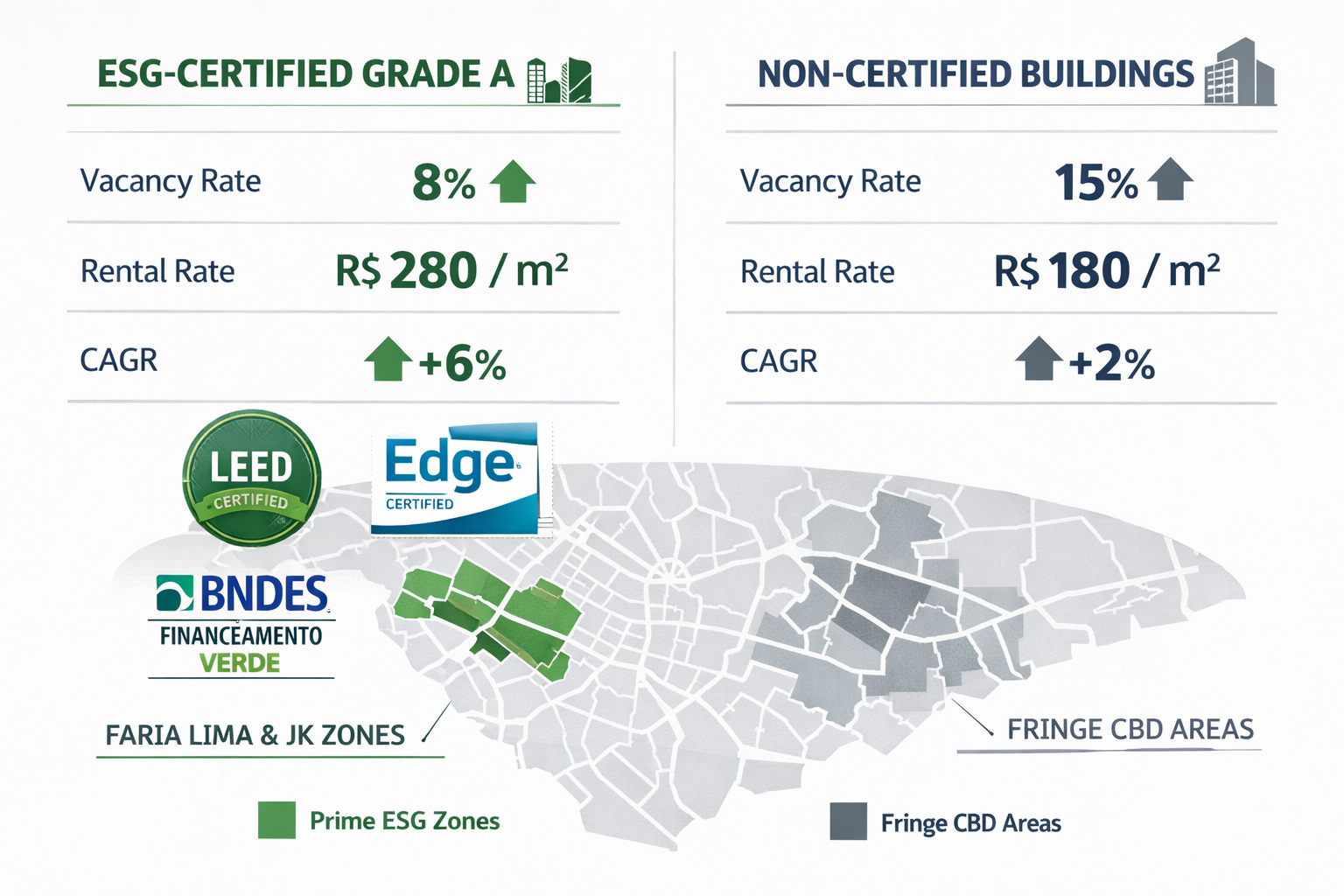

- 📉 Faria Lima vacancy sits below 8%, while non-certified fringe CBD towers exceed 15% vacancy — a stark performance gap driven by ESG demand.

- 💰 The São Paulo state government confirmed a USD 1.14 billion PPP in February 2026 to deliver 288,000 sq m of ESG-benchmarked Grade A offices, signaling institutional momentum.

- 📈 Grade A offices are forecast to grow at a 5.47% CAGR through 2031, outpacing the broader South American office market CAGR of 4.91%.

The Green Premium Is Now Structural, Not Cyclical

For years, sustainability features in commercial real estate were treated as optional upgrades — nice to have, rarely priced in. That era is over. ESG compliance as a rental premium driver has become a structural market force in São Paulo’s Grade A office segment, underpinned by corporate sustainability mandates, institutional investor criteria, and a genuine shortage of certified supply.

The Supply Gap Fueling Premium Pricing

The most powerful dynamic sustaining green rent premiums is simple: supply is scarce. Less than 30% of São Paulo’s existing office stock meets current green certification thresholds under LEED or EDGE standards [1]. With corporate occupiers increasingly embedding ESG compliance requirements directly into their real estate briefs, the pool of eligible buildings is dramatically smaller than total market supply.

This creates a seller’s market within a market — where certified landlords negotiate from a position of structural advantage. Tenants who need certified space to satisfy their own ESG reporting obligations, board mandates, or investor expectations have fewer alternatives, and that scarcity translates directly into pricing power.

💬 “The flight-to-quality trend is no longer about prestige — it’s about compliance. Tenants need certified buildings to meet their own ESG commitments.”

Faria Lima vs. The Fringe: A Tale of Two Markets

The vacancy data tells the clearest story. São Paulo’s premium ESG-certified submarkets — particularly Faria Lima and JK — maintained vacancy rates below 8% in 2025, while non-certified fringe CBD towers exceeded 15% vacancy during the same period [1]. This is not a marginal difference. It represents a fundamental bifurcation of the market along ESG lines.

Average asking prices in Faria Lima and JK more than doubled over the past six years, climbing from approximately R$ 130/m² to R$ 280/m², with peak prices reaching R$ 350/m² in the most sought-after stretches between Avenida Cidade Jardim and Faria Lima’s terminus [2]. Non-certified buildings in secondary locations have not participated in this appreciation cycle.

| Metric | ESG-Certified Grade A | Non-Certified Grade B/Fringe |

|---|---|---|

| Vacancy Rate (2025) | < 8% | > 15% |

| Avg. Asking Price | R$ 280–350/m² | R$ 130–180/m² |

| Rental Premium | +10–15% | Baseline |

| CAGR Forecast (to 2031) | 5.47% | 4.91% (market avg.) |

| Tenant Profile | MNCs, fintechs, institutional | SMEs, cost-sensitive occupiers |

Sources: [1][2][4]

How ESG Compliance Became a Standard Lease Clause in 2026

The transition from ESG as a marketing differentiator to ESG as a contractual lease requirement has accelerated sharply. Several converging forces drove this shift.

Corporate Sustainability Mandates Are Reshaping Tenant Demand

Large multinational corporations and Brazilian institutional tenants are now operating under formal ESG reporting frameworks — whether driven by EU taxonomy requirements for European-listed entities, B3’s ESG disclosure rules, or internal net-zero commitments. The building a company occupies is now a material ESG disclosure item.

This dynamic was illustrated vividly in January 2026 when fintech leader Nubank allocated USD 500 million over five years to expand corporate offices across São Paulo, Campinas, Rio de Janeiro, Belo Horizonte, and Bogotá — with ESG-compliant space cited as a core selection criterion [1]. When a company of Nubank’s scale and investor scrutiny makes that commitment, it signals to the entire market that certified space is a prerequisite, not a preference.

BNDES Green Finance and Municipal Tax Incentives

On the supply side, Brazil’s national development bank BNDES is increasingly channeling financing toward LEED-certified office developments, with cost-reduction incentives that improve developer economics for green projects [3]. Simultaneously, 55 municipalities across Brazil have introduced tax incentives to promote green construction as of early 2026 [3].

These policy levers are reducing the incremental cost of certification — historically cited as a barrier — while increasing the financial return on green investment. For developers, the calculus is shifting: the premium rental income from a certified building now more than offsets the additional upfront certification cost across a standard investment horizon.

For those exploring real estate investment opportunities in Brazil’s growing markets, understanding how ESG compliance drives asset value is increasingly central to underwriting decisions.

The February 2026 PPP: Government as ESG Anchor Tenant

Perhaps the most significant institutional signal of 2026 came from the São Paulo state government itself. In February 2026, the state confirmed a 30-year Public-Private Partnership auction to consolidate 22,700 civil servants into 288,000 sq m of Grade A offices built to explicit ESG benchmarks — a USD 1.14 billion commitment [1].

This is transformative for two reasons:

- It validates ESG standards as a government procurement requirement, normalizing certification expectations across the broader market.

- It injects a massive long-term anchor tenant into the Grade A ESG segment, reducing risk for developers and investors building or repositioning certified stock.

Monetizing Sustainability: The Developer and Investor Playbook

Understanding ESG compliance as a rental premium driver — and specifically how green certifications are commanding 15% price premiums in São Paulo’s Grade A office market in 2026 — requires translating the market data into actionable development and investment strategy.

Certification as a Revenue Strategy, Not a Cost Center

The most important mindset shift for developers is reframing certification from a cost line to a revenue strategy. A 15% rental premium on a 10,000 sq m Grade A tower in Faria Lima — where base rents approach R$ 280/m² — translates to approximately R$ 420,000 per month in additional gross rental income compared to a non-certified equivalent. Over a 10-year lease, that premium represents over R$ 50 million in incremental revenue before accounting for capital value appreciation.

💡 Key Insight: At current Faria Lima pricing, a 15% ESG rental premium on a mid-size Grade A tower can recover LEED certification costs within 18–24 months of occupancy.

The Flight-to-Quality Consolidation Wave

A medium-term trend with significant demand implications is corporate consolidation into fewer, higher-quality locations. Companies are trading multiple non-certified offices for single ESG-certified flagship headquarters — reducing their real estate footprint while upgrading quality. This trend is contributing an estimated +1.2% incremental demand across Brazil, Chile, Colombia, and Argentina [1].

For developers, this creates an opportunity to target consolidation-driven demand — positioning certified buildings as the destination for companies rationalizing their portfolios. New office deliveries are increasingly incorporating LEED or EDGE certifications alongside touchless entry systems, advanced HVAC, and wellness amenities as standard features, not optional upgrades [1].

Investors evaluating real estate development projects with strong value appreciation potential should weigh ESG certification as a primary value driver alongside location and specification.

Grade A Market Share and Growth Trajectory

Grade A towers captured 55.2% of the South American office real estate market share in 2025, with sub-8% vacancy rates and 12% rental premiums over Grade B peers driven largely by ESG and amenity advantages [1]. The growth trajectory reinforces the investment case: Grade A offices are forecast to expand at a 5.47% CAGR through 2031, outrunning the broader South American office market CAGR of 4.91% [1].

São Paulo’s overall high-grade corporate office market achieved a 15.9% vacancy rate by Q4 2025 — the lowest recorded since 2012 — reflecting the demand pressure that supports ESG premium rental rates across the city [4]. Within that overall market, certified Grade A submarkets are performing significantly better than the aggregate figure suggests.

Repositioning Legacy Stock: The Retrofit Opportunity

Not every ESG premium play requires ground-up development. Repositioning existing Grade B assets to meet LEED or EDGE certification standards represents a significant opportunity in São Paulo’s market, where the supply gap in certified stock is most acute.

Successful repositioning typically involves:

- ✅ Upgrading HVAC systems to meet energy efficiency benchmarks

- ✅ Installing water recycling and rainwater harvesting systems

- ✅ Achieving LEED Building Operations & Maintenance (O+M) certification

- ✅ Adding wellness amenities (air quality monitoring, biophilic design elements)

- ✅ Implementing smart building management systems for real-time ESG reporting

The Brazilian real estate sector is also seeing innovation in financing structures, with alternative capital sources increasingly supporting sustainable development and repositioning projects.

What Institutional Tenants Are Actually Paying For

The 15% premium is not simply for a certificate on a wall. Institutional tenants are paying for a bundle of quantifiable operational and reputational benefits that certified buildings deliver.

Operational Cost Savings

LEED-certified buildings typically consume 25–30% less energy and 30–50% less water than conventional equivalents. For large corporate occupiers with significant utility footprints, these savings are material — and increasingly relevant as Brazilian energy prices remain volatile. The operational savings partially offset the rental premium, making the all-in occupancy cost difference smaller than the headline rent gap suggests.

Talent Attraction and Retention

In São Paulo’s competitive talent market — particularly in finance, technology, and professional services — workplace quality is a recruitment tool. Certified buildings with wellness amenities, superior air quality, natural light optimization, and biophilic design elements contribute measurably to employee satisfaction and retention metrics. Companies that can point to a LEED Platinum headquarters are making a statement to prospective employees that resonates beyond compensation packages.

ESG Reporting and Investor Relations

For publicly listed companies or those with institutional investors applying ESG screens, the building address is now an ESG data point. Occupying a certified building provides verifiable, auditable evidence of environmental commitment that feeds directly into sustainability reports, investor presentations, and regulatory disclosures. The reputational and compliance value of this evidence is increasingly being priced into tenant willingness to pay.

Exploring current real estate market trends and investment insights can help investors and developers stay ahead of evolving ESG demand signals across Brazil’s dynamic property landscape.

Risks and Considerations

No market premium is without risk. Several factors merit careful consideration:

- ⚠️ Greenwashing scrutiny is intensifying. Tenants and investors are applying greater due diligence to certification claims. Buildings with outdated LEED versions or certifications that don’t reflect actual operational performance face reputational and legal exposure.

- ⚠️ Certification maintenance requires ongoing investment. LEED O+M recertification cycles demand sustained operational discipline and capital allocation — costs that must be factored into long-term asset management budgets.

- ⚠️ New supply could compress premiums. As more developers pursue certification to capture the green premium, supply of certified stock will grow. The current 15% premium reflects scarcity; as the certified supply share rises above 30%, some compression is likely over a 5–7 year horizon.

- ⚠️ Macroeconomic sensitivity. Brazil’s interest rate environment and currency volatility can affect tenant expansion decisions regardless of ESG preferences, particularly for smaller occupiers with tighter cost constraints.

For investors comparing different real estate market opportunities across Brazil, understanding the risk-adjusted return profile of ESG-certified assets relative to conventional stock is an essential part of portfolio construction.

Conclusion: Actionable Next Steps for Developers and Investors

The evidence assembled across 2025 and into 2026 is conclusive: ESG compliance is a rental premium driver, and green certifications are commanding 15% price premiums in São Paulo’s Grade A office market with structural, not cyclical, foundations. The supply gap is real, the institutional demand is accelerating, and government policy is reinforcing the trend through both financing incentives and anchor procurement commitments.

For developers, the priority actions are clear:

- Pursue LEED or EDGE certification on all new ground-up developments — the premium recovery timeline has shortened to under two years at current Faria Lima pricing.

- Evaluate retrofit certification pathways for existing Grade B assets in prime locations — the repositioning premium can be significant.

- Engage BNDES green finance programs and municipal tax incentive schemes to optimize project economics.

For investors, the strategic imperatives are:

- Overweight ESG-certified Grade A assets in São Paulo’s Faria Lima and JK submarkets, where the vacancy and pricing data most strongly support premium valuations.

- Apply certification status as a primary underwriting filter — non-certified assets in the same locations carry structurally higher vacancy risk.

- Monitor the PPP pipeline — the February 2026 USD 1.14 billion government commitment signals further Grade A ESG supply absorption over the next decade.

For tenants, the message is equally direct: locking in long-term leases in certified buildings now — before the supply gap narrows further — provides both cost predictability and ESG compliance certainty that will become increasingly valuable as reporting requirements tighten.

The green premium is no longer a bonus. In São Paulo’s Grade A office market in 2026, it is the baseline expectation. Developers and investors who treat sustainability as a core financial strategy — rather than a reputational add-on — are positioned to capture the most durable returns in Brazil’s commercial real estate cycle.

To explore premium real estate developments built with quality and value at their core, or to learn more about how leading developers are approaching the next generation of high-performance assets, the market intelligence available in 2026 has never been clearer.

References

[1] South America Office Real Estate Market – https://www.mordorintelligence.com/industry-reports/south-america-office-real-estate-market

[2] Premium Offices SP – https://www.cushmanwakefield.com/en/brazil/insights/premium-offices-sp

[3] Brazil Commercial Real Estate Share 43836054 – https://www.marketresearch.com/Mordor-Intelligence-LLP-v4018/Brazil-Commercial-Real-Estate-Share-43836054/

[4] São Paulo Market Reports – https://www.nmrk.com/insights/market-report/saopaulo-market-reports