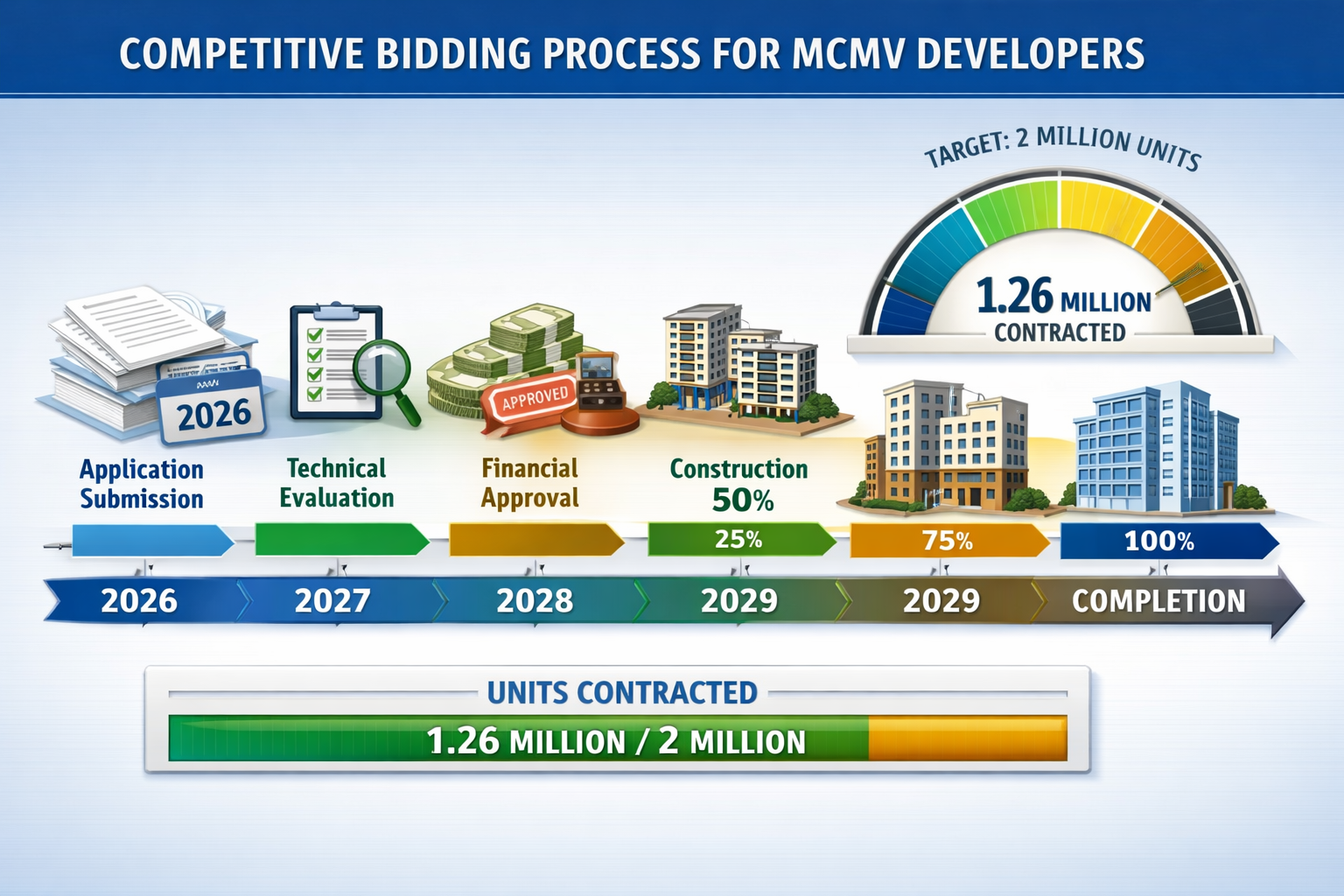

Brazil’s housing sector stands at a crossroads in 2026, with $39.8 billion in government-backed funding creating unprecedented opportunities for developers who understand how to navigate the complex FGTS financing system. As the Minha Casa Minha Vida (MCMV) program races toward its ambitious target of 2 million units, developers face both massive potential and significant challenges in capturing their share of this subsidized housing boom.

The stakes couldn’t be higher. With 1.26 million units already contracted and political uncertainty looming ahead of the October 2026 presidential elections, developers must act strategically to secure funding, optimize project timelines, and position themselves competitively in this rapidly evolving market[5].

Key Takeaways

- $39.8 billion in housing investment is available through FGTS and supplementary funding channels in 2026, creating massive opportunities for developers who understand the application process

- Three distinct financing channels (FGTS, SBPE, SFI) serve different income brackets, with FGTS offering subsidized rates of 4-8% compared to 11-12% market rates

- Faixa 4 expansion now covers families earning up to R$12,000/month with property ceilings of R$275,000 in major metros, opening new market segments

- Political risk ahead of October 2026 elections requires developers to accelerate project timelines and secure funding commitments early

- Competitive bidding strategies and technical compliance are critical for winning MCMV contracts in an increasingly crowded marketplace

Understanding the FGTS Funding Mechanism Behind the 2026 MCMV Surge

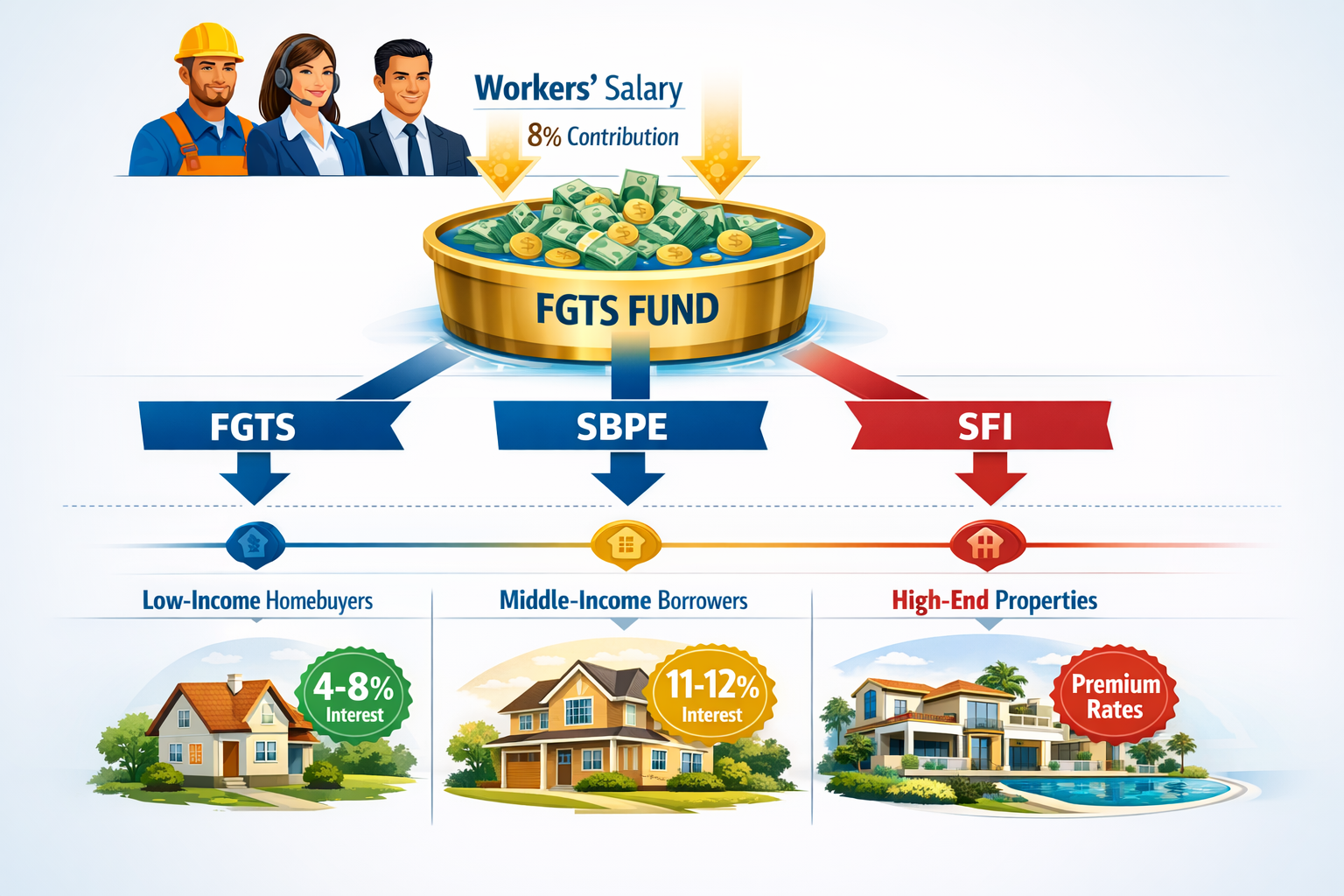

The Fundo de Garantia do Tempo de Serviço (FGTS) represents the financial backbone of Brazil’s affordable housing push. Every formal worker in Brazil has 8% of their salary automatically deposited into this workers’ fund by their employer. The government then channels these accumulated funds into low-income mortgages at significantly subsidized interest rates[5].

This mechanism creates a powerful financing engine that benefits all stakeholders:

How FGTS Creates Below-Market Financing

The FGTS system operates through three distinct channels, each targeting different income segments[5]:

🏠 FGTS Channel (Low-Income)

- Target: Families earning up to R$4,400/month

- Interest rates: 4-8% annually

- Maximum property value: Varies by region

- Primary subsidy source for MCMV units

🏘️ SBPE Channel (Middle-Income)

- Target: Families earning R$4,400-R$8,000/month

- Interest rates: 8-11% annually

- Backed by savings accounts (poupança)

- Moderate subsidies available

🏢 SFI Channel (Market-Rate)

- Target: Higher-income borrowers

- Interest rates: 11-12% or higher

- Market-based financing

- Minimal government subsidies

For developers, understanding which channel their projects qualify for is crucial. The FGTS channel offers the most attractive terms for buyers, which translates to faster sales velocity and reduced inventory risk for developers targeting low-income segments.

The 2026 Budget Expansion: What Developers Need to Know

The MCMV program received a substantial boost in 2026 with a $2.0 billion expansion for direct subsidies plus a planned $3.3 billion injection from the Pre-Salt Social Fund[5]. This additional capital aims to accelerate the program toward its 2 million unit target.

For developers navigating financing the 2026 MCMV surge, this expansion means:

✅ Increased subsidy availability for qualifying projects

✅ Faster approval timelines as funding bottlenecks ease

✅ Greater flexibility in project specifications and locations

✅ Enhanced credit guarantees reducing developer risk exposure

However, this funding surge also intensifies competition. Developers must differentiate their proposals through superior technical compliance, strategic location selection, and demonstrated construction capacity.

Strategic Approaches for Financing the 2026 MCMV Surge Through Competitive Bidding

Securing FGTS funding requires developers to navigate a competitive bidding process that evaluates technical capability, financial stability, and project viability. Success demands a systematic approach that begins months before formal application submission.

Pre-Qualification Requirements and Documentation

Before entering the bidding process, developers must establish their credentials through comprehensive documentation:

Financial Requirements:

- Audited financial statements for the past 3 years

- Proof of minimum equity capital (typically 20-30% of project value)

- Credit history and banking relationships

- Tax compliance certificates (federal, state, municipal)

Technical Requirements:

- Professional registration (CREA, CAU)

- Portfolio of completed projects with similar scope

- Quality certifications (PBQP-H or equivalent)

- Environmental licenses and permits

Legal Requirements:

- Clean land title with no encumbrances

- Zoning compliance documentation

- Corporate registration and bylaws

- Construction insurance policies

Developers who invest in best practices for property investment position themselves more competitively in the MCMV bidding process.

Optimizing Your MCMV Application for Maximum Success

The application evaluation process weighs multiple factors. Developers can improve their competitive position by focusing on these high-impact areas:

| Evaluation Criteria | Weight | Optimization Strategy |

|---|---|---|

| Technical Capacity | 30% | Demonstrate successful track record with similar projects |

| Financial Strength | 25% | Maintain strong balance sheet, secure pre-approvals |

| Project Location | 20% | Target high-demand areas with infrastructure |

| Timeline Feasibility | 15% | Present realistic schedules with contingency buffers |

| Social Impact | 10% | Emphasize community benefits, job creation |

Pro Tip: Applications that demonstrate integration with existing infrastructure and proximity to employment centers score significantly higher in location evaluations.

The Faixa 4 Opportunity: Expanding Your Market Reach

One of the most significant developments in financing the 2026 MCMV surge is the Faixa 4 coverage extension, which now includes families earning up to R$12,000 per month[5]. This expansion opens substantial new market opportunities for developers.

Faixa 4 Key Parameters:

- Income range: R$8,000-R$12,000/month

- Property value ceiling: R$275,000 (major metropolitan areas)

- Interest rates: 9-10% (still below market)

- Subsidy level: Moderate government support

This tier represents a sweet spot for developers because:

🎯 Higher profit margins than lower Faixas

🎯 Faster buyer qualification due to higher incomes

🎯 Greater design flexibility with higher value ceilings

🎯 Reduced default risk from more financially stable buyers

Developers should consider positioning projects specifically for Faixa 4 buyers, particularly in high-growth regions where property values align with the R$275,000 ceiling.

Navigating Political Risk and Timeline Optimization in 2026

The elephant in the room for financing the 2026 MCMV surge is the October 2026 presidential election. Historical precedent shows that housing programs in Brazil face significant policy risk during political transitions[5].

Understanding the Political Timeline Impact

Developers must recognize that political uncertainty creates both risks and opportunities:

⚠️ Risk Factors:

- Potential program modifications or discontinuation post-election

- Funding delays during transition periods

- Policy reversals affecting subsidy structures

- Regulatory changes impacting project specifications

✅ Opportunity Factors:

- Current administration’s urgency to show results before elections

- Accelerated approvals to meet political targets

- Enhanced subsidies to demonstrate program success

- Flexibility in requirements to boost unit numbers

Smart developers are front-loading their applications and accelerating construction timelines to secure funding commitments and achieve substantial completion before potential policy shifts.

Accelerated Project Timeline Strategies

To mitigate political risk, developers should implement these timeline optimization strategies:

Phase 1: Pre-Application (Months 1-3)

- Secure land with clear title

- Complete environmental studies

- Obtain preliminary permits

- Assemble professional team

Phase 2: Application & Approval (Months 4-6)

- Submit comprehensive MCMV application

- Respond promptly to information requests

- Maintain regular communication with Caixa Econômica Federal

- Secure backup financing options

Phase 3: Construction Launch (Months 7-9)

- Begin foundation work immediately upon approval

- Implement prefabrication strategies to accelerate timeline

- Establish robust supply chain with multiple vendors

- Deploy project management technology for real-time tracking

Phase 4: Execution & Delivery (Months 10-24)

- Maintain aggressive construction schedule

- Implement quality controls to avoid rework delays

- Begin buyer marketing and qualification early

- Coordinate final inspections and certifications

Developers who have successfully navigated market performance challenges understand that timeline discipline directly impacts profitability in subsidized housing projects.

Diversification Strategies Beyond MCMV

While the $39.8 billion MCMV opportunity is substantial, prudent developers maintain portfolio diversification to hedge against political and market risks:

Alternative Revenue Streams:

- Mixed-Income Developments: Combine MCMV units with market-rate properties to balance risk and returns

- Commercial Integration: Add ground-floor retail or service spaces to enhance project economics

- Private Market Projects: Maintain non-subsidized developments for higher-income segments

- Build-to-Rent: Explore rental housing models less dependent on government subsidies

Developers should consider how cryptocurrency and real estate integration might provide additional financing flexibility beyond traditional FGTS channels.

Financial Structuring and Risk Management for MCMV Projects

Successfully financing the 2026 MCMV surge requires sophisticated financial structuring that balances leverage, liquidity, and risk exposure.

Capital Stack Optimization

A typical MCMV project capital stack includes:

Equity (20-30%)

- Developer contribution

- Strategic investor capital

- Family office investments

FGTS Financing (50-60%)

- Primary construction loan

- Subsidized buyer mortgages

- Government guarantees

Mezzanine Financing (10-20%)

- Private credit facilities

- Construction bonds

- Supplier financing arrangements

The key to successful structuring is matching financing terms to project cash flow cycles. MCMV projects typically generate negative cash flow during construction, followed by rapid positive cash flow as units sell and FGTS mortgages close.

Managing Buyer Default Risk

While FGTS financing includes government guarantees, developers still face risks from buyer defaults during the qualification and closing process:

Risk Mitigation Strategies:

🛡️ Pre-Qualification Screening: Implement rigorous buyer financial assessment before unit reservation

🛡️ Multiple Backup Buyers: Maintain waiting lists with qualified alternates for each unit type

🛡️ Flexible Payment Plans: Offer varied down payment structures within MCMV guidelines

🛡️ Credit Enhancement: Partner with financial institutions offering buyer credit improvement programs

Developers focusing on pre-construction sales strategies can reduce inventory risk and improve project cash flow.

Cost Control and Value Engineering

MCMV projects operate within strict price ceilings, making cost control essential for profitability:

High-Impact Cost Reduction Areas:

| Cost Category | Typical % of Budget | Optimization Approach |

|---|---|---|

| Land Acquisition | 15-20% | Target peripheral areas with infrastructure |

| Materials | 35-40% | Bulk purchasing, alternative materials |

| Labor | 25-30% | Prefabrication, productivity incentives |

| Financing | 8-12% | Optimize capital stack, minimize carry costs |

| Overhead | 5-8% | Shared services, technology automation |

Value Engineering Priorities:

- Standardized floor plans to reduce design costs

- Modular construction techniques to accelerate timelines

- Local material sourcing to minimize logistics expenses

- Energy-efficient systems to reduce operational costs for buyers

Location Strategy: Where to Deploy Your MCMV Projects in 2026

Geographic strategy significantly impacts both MCMV approval success and long-term project performance. The program prioritizes locations that maximize social impact while ensuring buyer access to employment and services.

High-Priority Metropolitan Areas

FGTS funding allocation favors major metropolitan regions with:

✅ Strong employment markets supporting buyer income stability

✅ Existing infrastructure (transportation, utilities, services)

✅ Housing deficits demonstrating clear demand

✅ Municipal cooperation with streamlined permitting

Top-Performing Markets for 2026:

- São Paulo Metropolitan Region: Largest housing deficit, highest FGTS allocation

- Rio de Janeiro: Significant demand, infrastructure investments

- Belo Horizonte: Strong economic growth, favorable cost structure

- Florianópolis: Emerging market with strong fundamentals

- Brasília: Government employment stability, consistent demand

Secondary Market Opportunities

While major metros receive the largest funding allocations, secondary markets often offer superior risk-adjusted returns:

Advantages of Secondary Markets:

- Lower land costs improving project economics

- Reduced competition for FGTS funding

- Faster permitting and approval processes

- Strong local demand with limited supply

- Lower construction costs

Developers should evaluate regional market dynamics when selecting project locations to balance funding availability against competitive intensity.

Site Selection Criteria for Maximum MCMV Scoring

Within target markets, specific site characteristics significantly impact MCMV application scoring:

High-Value Site Attributes:

🏆 Proximity to Employment Centers (within 30km)

🏆 Public Transportation Access (bus routes, future metro stations)

🏆 Educational Facilities (schools within 2km)

🏆 Healthcare Services (clinics, hospitals accessible)

🏆 Commercial Services (shopping, banking, services)

🏆 Infrastructure Readiness (water, sewer, electricity, paving)

Sites scoring high across these dimensions receive priority in FGTS funding allocation and achieve faster sales velocity post-construction.

Building Strategic Partnerships for MCMV Success

No developer succeeds in financing the 2026 MCMV surge alone. Strategic partnerships multiply capabilities and reduce risk exposure.

Key Partnership Categories

Financial Partners:

- Regional banks with FGTS lending expertise

- Private equity firms focused on affordable housing

- Construction finance specialists

- Credit enhancement providers

Technical Partners:

- Architectural firms with MCMV design experience

- Construction companies specializing in affordable housing

- Property management firms for post-delivery services

- Technology providers for project management systems

Government Relations:

- Municipal housing departments

- Caixa Econômica Federal relationship managers

- State housing agencies

- Federal program administrators

Community Partners:

- Local resident associations

- Social service organizations

- Employment training programs

- Community development corporations

Structuring Win-Win Partnership Agreements

Effective partnerships require clear agreements that align incentives:

Partnership Structure Options:

- Joint Venture: Shared equity and decision-making for major projects

- Fee-for-Service: Fixed fees for specific expertise or services

- Profit Sharing: Performance-based compensation tied to project success

- Strategic Alliance: Long-term collaboration across multiple projects

The most successful MCMV developers build recurring partnerships that create competitive advantages through accumulated expertise and streamlined processes.

Technology and Innovation in MCMV Project Delivery

Forward-thinking developers leverage technology to improve efficiency, reduce costs, and accelerate timelines when financing the 2026 MCMV surge.

Construction Technology Solutions

Prefabrication and Modular Construction:

- 30-40% reduction in construction timeline

- Improved quality control through factory production

- Reduced weather-related delays

- Lower labor costs per unit

Building Information Modeling (BIM):

- Enhanced design coordination reducing rework

- Accurate quantity takeoffs improving cost estimation

- Clash detection preventing construction conflicts

- Facility management data for post-delivery operations

Project Management Platforms:

- Real-time progress tracking against milestones

- Automated reporting to FGTS administrators

- Supply chain coordination and logistics optimization

- Quality control documentation and verification

Digital Marketing and Sales Technology

MCMV projects require efficient buyer acquisition and qualification systems:

Digital Sales Tools:

- Virtual reality unit tours for remote buyers

- Online application and pre-qualification systems

- Automated FGTS eligibility verification

- Digital document management for faster closings

Developers can learn from successful sales performance strategies to optimize their MCMV marketing approaches.

Sustainability and Green Building Integration

While MCMV projects operate under tight budget constraints, strategic sustainability investments create long-term value:

Cost-Effective Green Features:

- Solar water heating (minimal upfront cost, significant buyer savings)

- Natural ventilation design (reduces cooling costs)

- Rainwater collection systems (lowers utility expenses)

- LED lighting (immediate energy savings)

- Low-flow plumbing fixtures (water conservation)

These features improve buyer satisfaction, reduce default risk through lower operating costs, and can provide additional points in MCMV application scoring.

Conclusion: Seizing the $39.8 Billion MCMV Opportunity in 2026

Financing the 2026 MCMV surge represents a generational opportunity for Brazilian developers who approach it strategically. With $39.8 billion in government-backed funding flowing into affordable housing, the potential for profitable growth is substantial—but only for developers who understand the complexities of FGTS financing, competitive positioning, and risk management.

Your Action Plan for MCMV Success

Immediate Actions (Next 30 Days):

- Assess your current portfolio and capacity for MCMV projects

- Establish relationships with Caixa Econômica Federal representatives

- Identify target markets and potential sites meeting MCMV criteria

- Assemble your professional team (architects, engineers, legal counsel)

- Review financial capacity and identify potential funding partners

Short-Term Priorities (Next 90 Days):

- Complete site due diligence and secure land options

- Develop preliminary project designs meeting MCMV specifications

- Prepare comprehensive MCMV application documentation

- Submit applications for priority projects before political timeline pressure

- Build strategic partnerships to strengthen competitive position

Long-Term Strategy (Next 12-24 Months):

- Maintain diversified portfolio balancing MCMV and market-rate projects

- Invest in construction technology and process optimization

- Build recurring buyer pipeline through digital marketing

- Expand into multiple markets to reduce concentration risk

- Develop expertise in Faixa 4 segment for higher-margin opportunities

The window for maximizing returns from the 2026 MCMV surge is limited. Political uncertainty surrounding the October elections creates urgency for developers to secure funding commitments and achieve construction milestones before potential policy shifts.

Developers who act decisively, maintain financial discipline, and execute efficiently will capture disproportionate value from this historic housing investment. The question isn’t whether the opportunity exists—it’s whether you’re positioned to seize it.

For developers ready to expand their capabilities in Brazil’s dynamic real estate market, exploring strategic development opportunities and understanding regional market trends provides essential context for success.

The $39.8 billion question is simple: Will you be among the developers who transform this government investment into sustainable business growth?

References

[5] Brazil Housing Boom Flash In The Pan Or Lula S Masterstroke – https://www.zonebourse.com/actualite-bourse/brazil-housing-boom-flash-in-the-pan-or-lula-s-masterstroke-ce7d50d8db88f620