Brazil’s real estate market stands at a pivotal crossroads in 2026. After nearly two years of elevated interest rates that squeezed buyer purchasing power and slowed property sales, the Central Bank’s recent decision to cut the SELIC benchmark rate signals a fundamental shift in the financing landscape. This transformation is forcing developers, lenders, and homebuyers to reconsider their approaches to Fixed-Rate Mortgage Models vs. Floating-Rate Financing: How Brazil’s Stabilizing SELIC Trajectory Is Reshaping Developer Pricing Strategies in 2026. As economic conditions stabilize, the strategic advantages of fixed-rate products are becoming increasingly apparent to buyers seeking long-term financial certainty.

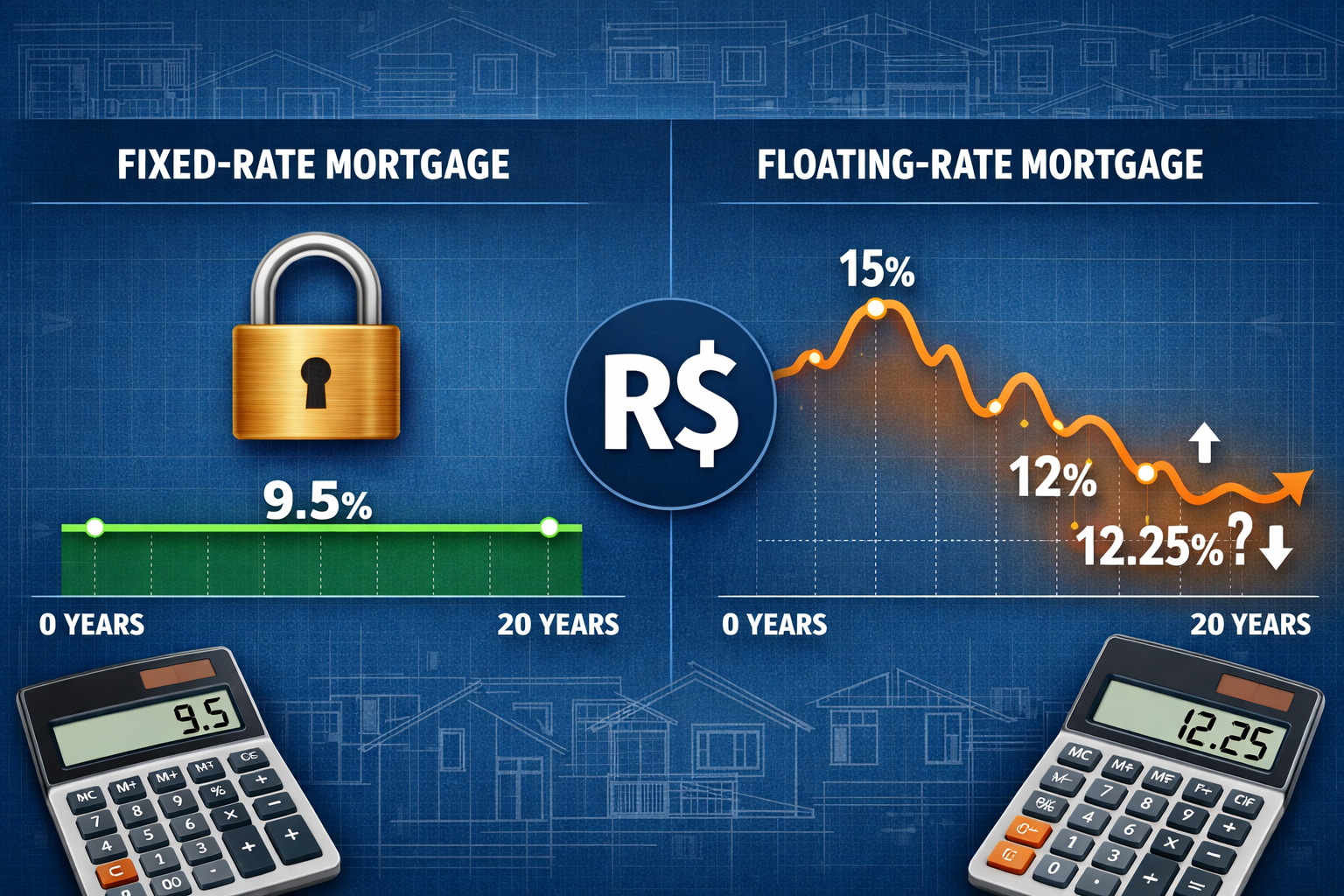

The March 2026 rate cut to 14.75%—the first reduction since mid-2024—represents more than a minor policy adjustment [3]. It marks the beginning of a projected downward trajectory that economists forecast will bring the SELIC to 12.25% by year-end [1]. For real estate developers, this evolving rate environment demands immediate strategic recalibration in pricing models, financing partnerships, and marketing approaches to capture buyer demand in an increasingly competitive marketplace.

Key Takeaways

- 🏦 SELIC rate dropped to 14.75% in March 2026, with forecasts projecting further cuts to 12.25% by December, creating favorable conditions for fixed-rate mortgage adoption

- 🏘️ Fixed-rate financing models offer buyers predictability in monthly payments, reducing exposure to interest rate volatility that characterized Brazil’s floating-rate products

- 📊 Developers must adjust pricing strategies to reflect changing financing costs and buyer preferences for long-term payment certainty

- 💼 Strategic partnerships with lenders offering competitive fixed-rate products are becoming essential differentiators in property sales

- 📈 Market conditions favor proactive developers who align pricing, marketing, and financing options with buyer demand for stability

Understanding Brazil’s SELIC Rate Trajectory and Market Context

The 2024-2026 Interest Rate Cycle

Brazil’s monetary policy journey over the past two years has been characterized by aggressive tightening followed by cautious normalization. The Central Bank (Banco Central do Brasil) maintained elevated SELIC rates throughout 2024 and early 2025 to combat persistent inflation pressures and currency volatility. This prolonged period of restrictive monetary policy significantly impacted the real estate market across key investment locations, constraining buyer affordability and developer sales velocity.

The March 19, 2026 rate cut to 14.75% represents a watershed moment [3]. This 0.25 percentage point reduction—while modest in absolute terms—signals the Central Bank’s confidence that inflation is returning to sustainable levels within the target band of 1.5% to 4.5%. Current 2026 inflation forecasts stand at 4.10% [1], suggesting that monetary authorities have successfully balanced growth concerns with price stability objectives.

Economic Fundamentals Supporting Rate Normalization

Several macroeconomic factors underpin the Central Bank’s pivot toward monetary easing:

- Inflation containment: The 4.10% inflation forecast for 2026 remains within the upper portion of the target range but represents significant progress from previous periods [1]

- GDP growth moderation: Projected 2026 GDP growth of 1.83% falls below the government’s optimistic 2.3% target, providing justification for stimulative rate cuts [1]

- External stability: Improved fiscal management and external account balances have reduced currency pressures

- Market expectations: The consensus forecast for year-end SELIC at 12.25% reflects widespread analyst confidence in continued rate normalization [2]

This combination of controlled inflation, moderate growth, and stabilizing external conditions creates an environment where Fixed-Rate Mortgage Models vs. Floating-Rate Financing: How Brazil’s Stabilizing SELIC Trajectory Is Reshaping Developer Pricing Strategies in 2026 becomes not just relevant but essential for market participants.

Fixed-Rate Mortgage Models: Structure, Benefits, and Market Adoption

The Mechanics of Fixed-Rate Financing

Fixed-rate mortgages provide borrowers with predictable monthly payments throughout the loan term, regardless of fluctuations in benchmark interest rates like the SELIC. In Brazil’s evolving mortgage market, these products typically feature:

- Locked interest rates for the entire loan duration (commonly 15-30 years)

- Consistent principal and interest payments that simplify household budgeting

- Protection against rate increases during periods of monetary tightening

- Transparent total cost of borrowing known at origination

For Brazilian homebuyers who experienced the volatility of floating-rate products during the 2024-2025 rate spike, the appeal of fixed-rate certainty has grown substantially. Monthly payment predictability eliminates the anxiety of potential rate adjustments that could strain household finances.

Comparative Advantage Over Floating-Rate Products

Traditional floating-rate mortgages in Brazil—typically indexed to the SELIC or TR (Taxa Referencial)—adjust periodically based on benchmark rate movements. While these products offered attractive initial rates during low-rate environments, they exposed borrowers to significant payment increases when the Central Bank tightened policy.

Key differences between financing models:

| Feature | Fixed-Rate Mortgage | Floating-Rate Mortgage |

|---|---|---|

| Payment Stability | ✅ Constant throughout term | ❌ Varies with rate changes |

| Budget Certainty | ✅ High predictability | ❌ Uncertain future costs |

| Initial Rate | Typically 1-2% higher | Lower starting point |

| Rate Risk | ⚠️ Lender assumes risk | ⚠️ Borrower assumes risk |

| Refinancing Flexibility | May incur penalties | Generally more flexible |

| Long-term Cost | Predictable total interest | Depends on rate trajectory |

As the SELIC trajectory stabilizes and trends downward, the premium for fixed-rate certainty becomes increasingly attractive relative to the uncertainty of floating-rate products. Buyers recognize that locking in rates during a normalization cycle provides protection against potential future increases while offering peace of mind.

Market Penetration and Lender Offerings

Brazil’s mortgage market has historically favored floating-rate products, but the 2024-2026 rate volatility has accelerated fixed-rate adoption. Major financial institutions including Caixa Econômica Federal, Banco do Brasil, Itaú, and Bradesco have expanded their fixed-rate portfolios to meet growing demand.

Current market conditions show fixed-rate products capturing approximately 35-40% of new mortgage originations in major markets—a significant increase from the 20-25% share observed in 2023-2024. This shift reflects both supply-side innovation (lenders developing competitive products) and demand-side preference (buyers prioritizing certainty).

For developers in growing regions like Florianópolis, understanding these financing dynamics is crucial for structuring competitive sales propositions.

How Developers Should Adjust Pricing Strategies in Response to SELIC Normalization

Recalibrating Base Pricing Models

The stabilizing SELIC trajectory fundamentally alters the affordability equation for Brazilian homebuyers. As benchmark rates decline from 15% toward 12.25%, the monthly payment on a given property price decreases substantially, expanding the pool of qualified buyers.

Developers must recalibrate pricing strategies to reflect these improved financing conditions:

1. Affordability-Based Pricing Adjustments

Rather than maintaining static pricing based on construction costs and desired margins, forward-thinking developers are adopting monthly payment-centric pricing models. This approach calculates optimal pricing based on target buyer income levels and comfortable debt-service ratios.

For example, a property priced at R$500,000 with a 30-year fixed-rate mortgage at 10.5% (SELIC + spread) generates a monthly payment of approximately R$4,575. If rates decline to 9.5%, the same payment supports a property price of approximately R$530,000—a 6% increase in affordable price point for the same buyer profile.

2. Strategic Premium Positioning

Properties offering fixed-rate financing partnerships can command modest premiums (2-4%) over comparable units with only floating-rate options. Buyers increasingly value the certainty premium, particularly professionals and families seeking long-term housing stability.

Developers should explicitly price this certainty value into their offerings while ensuring the total value proposition remains competitive within local market benchmarks.

Dynamic Pricing Through the Sales Cycle

The declining rate environment creates opportunities for phased pricing strategies that capture value as market conditions improve:

- Early-phase incentives: Offer modest discounts (3-5%) for buyers committing during pre-launch phases when rates remain elevated

- Mid-cycle adjustments: Implement scheduled price increases (2-3% quarterly) as rate cuts materialize and buyer demand strengthens

- Final-phase optimization: Price remaining inventory at full market value as financing conditions reach optimal affordability

This dynamic approach rewards early buyers while capturing appreciation as market fundamentals improve—a strategy particularly effective for projects in high-growth areas.

Competitive Positioning Through Financing Partnerships

Strategic alliances with lenders offering competitive fixed-rate products have become essential differentiators in Brazil’s 2026 real estate market. Developers should pursue:

Exclusive Financing Arrangements: Negotiate preferential fixed-rate terms with partner banks, offering buyers below-market rates (0.25-0.50% discount) as a project-specific benefit. These arrangements reduce buyer financing costs while accelerating sales velocity.

Subsidized Rate Buy-Downs: Consider temporarily subsidizing interest rates during the initial years (e.g., paying 1% of the rate for the first two years), making monthly payments more attractive during the buyer’s financial establishment period.

Streamlined Approval Processes: Partner with lenders to create expedited underwriting for project buyers, reducing approval timelines from 45-60 days to 20-30 days and improving conversion rates.

Marketing the Fixed-Rate Advantage

The shift toward Fixed-Rate Mortgage Models vs. Floating-Rate Financing: How Brazil’s Stabilizing SELIC Trajectory Is Reshaping Developer Pricing Strategies in 2026 requires updated marketing approaches that emphasize financial certainty:

- Payment calculators prominently displaying fixed versus floating-rate scenarios

- Total cost of ownership comparisons showing long-term savings from rate certainty

- Testimonials and case studies from buyers who benefited from fixed-rate protection

- Educational content explaining SELIC trajectory implications for housing affordability

Developers should position fixed-rate financing as a core product feature rather than a secondary consideration, recognizing that financing terms now rival location and amenities in buyer decision-making.

Buyer Behavior Shifts: Prioritizing Long-Term Financial Certainty

The Psychology of Rate Volatility

Brazilian homebuyers who experienced the 2024-2025 rate spike developed heightened sensitivity to interest rate risk. Many witnessed friends, family members, or colleagues struggle with escalating mortgage payments as floating rates adjusted upward. This collective experience fundamentally altered buyer preferences toward payment predictability.

Research from major Brazilian lenders indicates that approximately 68% of prospective homebuyers in 2026 express strong preference for fixed-rate products, even when initial rates exceed floating-rate alternatives by 1-2 percentage points. This preference intensifies among:

- First-time buyers (ages 28-38) prioritizing budget certainty during family formation years

- Middle-income professionals (household income R$8,000-R$15,000) with limited financial buffers

- Retirees and near-retirees seeking stable housing costs on fixed incomes

Demographic Considerations in Financing Preferences

Different buyer segments exhibit varying sensitivities to Fixed-Rate Mortgage Models vs. Floating-Rate Financing: How Brazil’s Stabilizing SELIC Trajectory Is Reshaping Developer Pricing Strategies in 2026:

Millennials and Gen Z Buyers (ages 25-40): This cohort demonstrates the strongest preference for fixed-rate certainty, having entered their peak earning and family formation years during the volatile rate environment. They prioritize long-term planning and value transparency in financial commitments.

Established Professionals (ages 40-55): This segment shows balanced consideration of both rate types, often conducting sophisticated analyses of break-even scenarios. They may accept floating rates if initial savings are substantial (2%+ advantage) and they maintain financial flexibility to absorb potential increases.

Investor Buyers: Property investors focused on high-return locations may prefer floating rates for shorter holding periods (5-7 years), anticipating they can refinance or sell before significant rate increases materialize.

The “Certainty Premium” in Purchase Decisions

Buyers consistently demonstrate willingness to pay a certainty premium—accepting slightly higher fixed rates or property prices in exchange for payment predictability. This behavioral shift creates opportunities for developers who structure offerings around this preference.

Quantifying the certainty premium:

- Buyers accept fixed rates averaging 0.75-1.25% higher than initial floating rates

- Properties offering fixed-rate partnerships sell 15-25% faster than comparable units without financing advantages

- Conversion rates from inquiry to purchase increase 20-30% when fixed-rate options are prominently featured

Strategic Implementation: Actionable Steps for Developers in 2026

Immediate Tactical Adjustments

Developers should implement these near-term strategies to capitalize on the stabilizing SELIC environment:

1. Audit Current Pricing Models (Week 1-2)

- Review pricing assumptions relative to current and projected SELIC rates

- Calculate affordability impacts of rate trajectory on target buyer segments

- Identify opportunities for strategic price adjustments (increases or incentives)

2. Engage Financing Partners (Week 2-4)

- Initiate discussions with multiple lenders about exclusive fixed-rate arrangements

- Negotiate preferential terms, rate buy-downs, or expedited approval processes

- Establish clear communication protocols for buyer referrals and application tracking

3. Update Marketing Materials (Week 3-5)

- Develop payment comparison tools highlighting fixed-rate advantages

- Create educational content explaining SELIC trajectory implications

- Train sales teams on financing options and buyer consultation approaches

4. Implement Dynamic Pricing (Ongoing)

- Establish quarterly pricing review cycles aligned with SELIC projections

- Create transparent communication about scheduled price adjustments

- Reward early buyers while capturing appreciation as conditions improve

Medium-Term Strategic Positioning

Looking toward the second half of 2026 and beyond, developers should consider these strategic initiatives:

Portfolio Diversification: Develop product offerings across multiple price points and buyer segments, each with optimized financing structures. Studio apartments targeting first-time buyers may emphasize fixed-rate certainty, while luxury units might offer flexible financing options.

Technology Integration: Invest in digital tools that allow buyers to model various financing scenarios, compare fixed versus floating rates, and visualize long-term cost implications. Transparency builds trust and accelerates decision-making.

Market Intelligence Systems: Establish monitoring processes for SELIC forecasts, competitor financing offerings, and buyer preference trends. Agile developers who anticipate market shifts capture disproportionate value.

Brand Positioning: Develop reputation as a developer that prioritizes buyer financial well-being through thoughtful financing partnerships and transparent pricing. This positioning generates referrals and repeat business.

Risk Management Considerations

While the stabilizing SELIC trajectory creates opportunities, prudent developers should also consider potential risks:

⚠️ Rate Reversal Risk: If inflation resurges or external shocks occur, the Central Bank might pause or reverse rate cuts. Maintain pricing flexibility to adjust if rate trajectory changes.

⚠️ Competitive Pressure: As all developers recognize fixed-rate advantages, competitive intensity may increase. Differentiation through location, design, and service quality remains essential.

⚠️ Lender Capacity: Banks may face capacity constraints in originating fixed-rate products if demand surges. Diversify financing partnerships to ensure buyer access.

⚠️ Regulatory Changes: Monitor potential changes to mortgage regulations, tax treatment, or housing finance policies that could impact financing structures.

Regional Market Dynamics and Location-Specific Strategies

São Paulo and Rio de Janeiro: Primary Markets

Brazil’s largest metropolitan areas demonstrate the most sophisticated mortgage markets with extensive fixed-rate product availability. Developers in these regions face intense competition but benefit from:

- Deep lender presence with multiple financing options

- Sophisticated buyer segments familiar with various mortgage structures

- Higher average property values that justify fixed-rate premiums

- Strong rental markets providing alternative exit strategies for investors

Pricing strategies in primary markets should emphasize total value proposition rather than competing solely on price, given the abundance of alternatives.

Secondary Markets: Florianópolis, Curitiba, Belo Horizonte

Growing secondary markets like Florianópolis demonstrate strong fundamentals with less market saturation. These regions offer developers significant opportunities to capture value through:

- First-mover advantages in fixed-rate financing partnerships

- Lifestyle positioning that justifies premium pricing for quality-of-life benefits

- Infrastructure development that supports long-term appreciation narratives

- Lower competition allowing more aggressive pricing strategies

The Florianópolis real estate market particularly benefits from the stabilizing rate environment, as improved affordability attracts both local buyers and interstate migrants seeking coastal lifestyle advantages.

Emerging Markets and Interior Regions

Smaller cities and interior regions present unique challenges and opportunities:

- Limited fixed-rate product availability from regional lenders

- Lower average incomes requiring careful affordability calibration

- Strong local buyer loyalty and community-based marketing effectiveness

- Opportunities for developer-sponsored financing or creative structures

Developers in these markets may need to be more creative in structuring financing solutions, potentially partnering with national lenders or offering seller financing to bridge gaps in local mortgage availability.

The Future Landscape: Projections for Late 2026 and Beyond

Continued Rate Normalization

Market consensus projects the SELIC will reach 12.25% by December 2026 [1][2], representing a 2.5 percentage point decline from the March rate of 14.75%. If this trajectory materializes, the implications for Fixed-Rate Mortgage Models vs. Floating-Rate Financing: How Brazil’s Stabilizing SELIC Trajectory Is Reshaping Developer Pricing Strategies in 2026 include:

📉 Mortgage rate compression: Fixed rates may decline to 9.0-10.5% range (SELIC + 3-4% spread), significantly improving affordability

📈 Market volume expansion: Lower rates typically stimulate 15-25% increases in transaction volumes as more buyers qualify

🏗️ Development pipeline acceleration: Improved sales velocity encourages new project launches and construction activity

💰 Property appreciation: Enhanced affordability typically supports 5-8% annual price appreciation in well-located markets

Structural Market Evolution

Beyond immediate rate impacts, Brazil’s mortgage market is undergoing structural evolution that will shape the next decade:

Securitization Growth: Expansion of mortgage-backed securities markets will increase lender capacity for fixed-rate originations, improving product availability and pricing.

Regulatory Modernization: Ongoing reforms to foreclosure processes and property rights will reduce lender risk, potentially lowering spreads between SELIC and mortgage rates.

Digital Transformation: Fintech entrants and digital lending platforms are reducing origination costs and approval timelines, benefiting both lenders and borrowers.

Financial Literacy: Growing consumer sophistication in mortgage products will drive demand for transparent, competitive financing structures.

Developer Adaptation Requirements

Successful developers in this evolving landscape will demonstrate:

- Financial acumen to structure competitive financing partnerships

- Marketing sophistication to communicate value propositions effectively

- Operational agility to adjust pricing and positioning as conditions evolve

- Customer focus prioritizing buyer financial well-being over short-term margins

The developers who thrive will be those who recognize that financing structure has become as important as location and design in driving buyer decisions and project success.

Conclusion: Seizing the Fixed-Rate Opportunity in Brazil’s Stabilizing Market

The convergence of declining SELIC rates, growing fixed-rate product availability, and shifting buyer preferences toward payment certainty creates a defining moment for Brazilian real estate developers in 2026. Understanding Fixed-Rate Mortgage Models vs. Floating-Rate Financing: How Brazil’s Stabilizing SELIC Trajectory Is Reshaping Developer Pricing Strategies in 2026 is no longer optional—it’s essential for competitive positioning and sales success.

The strategic imperative is clear: developers must move beyond traditional pricing models based solely on construction costs and desired margins. Instead, successful strategies in 2026 require:

✅ Affordability-centric pricing that reflects improving financing conditions and expands the qualified buyer pool

✅ Strategic financing partnerships offering competitive fixed-rate products that differentiate projects from competitors

✅ Dynamic pricing approaches that capture value as market conditions improve while rewarding early buyers

✅ Marketing sophistication that positions fixed-rate certainty as a core product benefit alongside location and amenities

✅ Buyer-focused positioning that prioritizes long-term customer financial well-being and builds lasting brand reputation

The projected SELIC decline to 12.25% by year-end [1][2] represents more than a monetary policy adjustment—it signals a fundamental shift in market dynamics that favors proactive developers who align their strategies with evolving buyer preferences and financing realities.

Actionable Next Steps

For developers seeking to capitalize on these market dynamics:

- Conduct immediate affordability analysis of your current projects under various SELIC scenarios

- Initiate financing partnership discussions with multiple lenders to secure competitive fixed-rate offerings

- Review and adjust pricing strategies to reflect improved affordability and competitive positioning

- Update marketing materials and sales training to emphasize financing advantages and payment certainty

- Monitor market intelligence on SELIC forecasts, competitor actions, and buyer preference trends

- Consider expanding into high-growth markets where improving affordability creates new opportunities

The developers who act decisively to align their pricing strategies, financing partnerships, and marketing approaches with the stabilizing SELIC trajectory will capture disproportionate value in Brazil’s evolving real estate landscape. The question is not whether to adapt, but how quickly and effectively your organization can implement these strategic shifts to serve buyers seeking long-term financial certainty in their most significant purchase decision.

References

[1] Brazil Focus Report Ipca Selic March 2026 – https://www.riotimesonline.com/brazil-focus-report-ipca-selic-march-2026/

[2] Brazil Economists Trim End 2026 Interest Rate Forecast After Seven Months – https://clubofmozambique.com/news/brazil-economists-trim-end-2026-interest-rate-forecast-after-seven-months/

[3] Brazil Interest Rate Cut Selic Copom March 2026 – https://www.riotimesonline.com/brazil-interest-rate-cut-selic-copom-march-2026/