Brazil’s real estate development landscape is experiencing a dramatic transformation in 2026. Housing credit expansion policy changes implemented at the start of this year are unlocking opportunities in regional markets that developers previously considered financially impossible. With $39.8 billion in total investment flowing into housing programs and revolutionary new mortgage rules taking effect, previously unviable regional projects are suddenly becoming profitable ventures for savvy developers and investors[1].

The Brazilian government’s strategic expansion of housing credit access is creating unprecedented opportunities across secondary cities and emerging regions. Developers who understand these policy changes and act quickly stand to benefit from a market shift that’s making regional residential development financially viable for the first time in years.

Key Takeaways

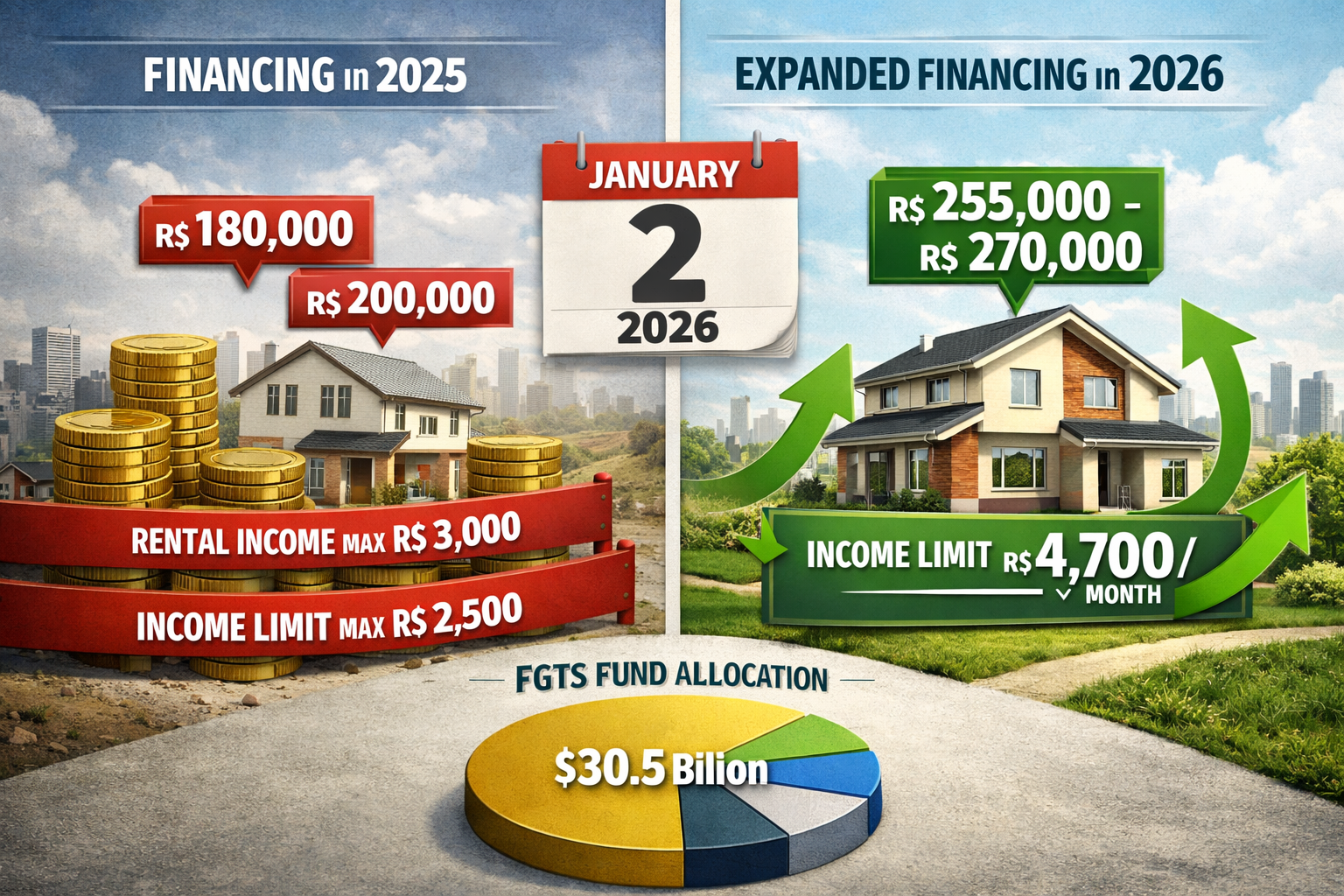

- 🏗️ New mortgage financing rules effective January 2, 2026, expand access for families earning up to 4,700 Reais monthly, with maximum property values reaching 255,000-270,000 Reais in larger urban centers[1]

- 💰 $39.8 billion total investment committed to housing programs in 2026, combining federal resources, FGTS funds, and specialized allocations[1]

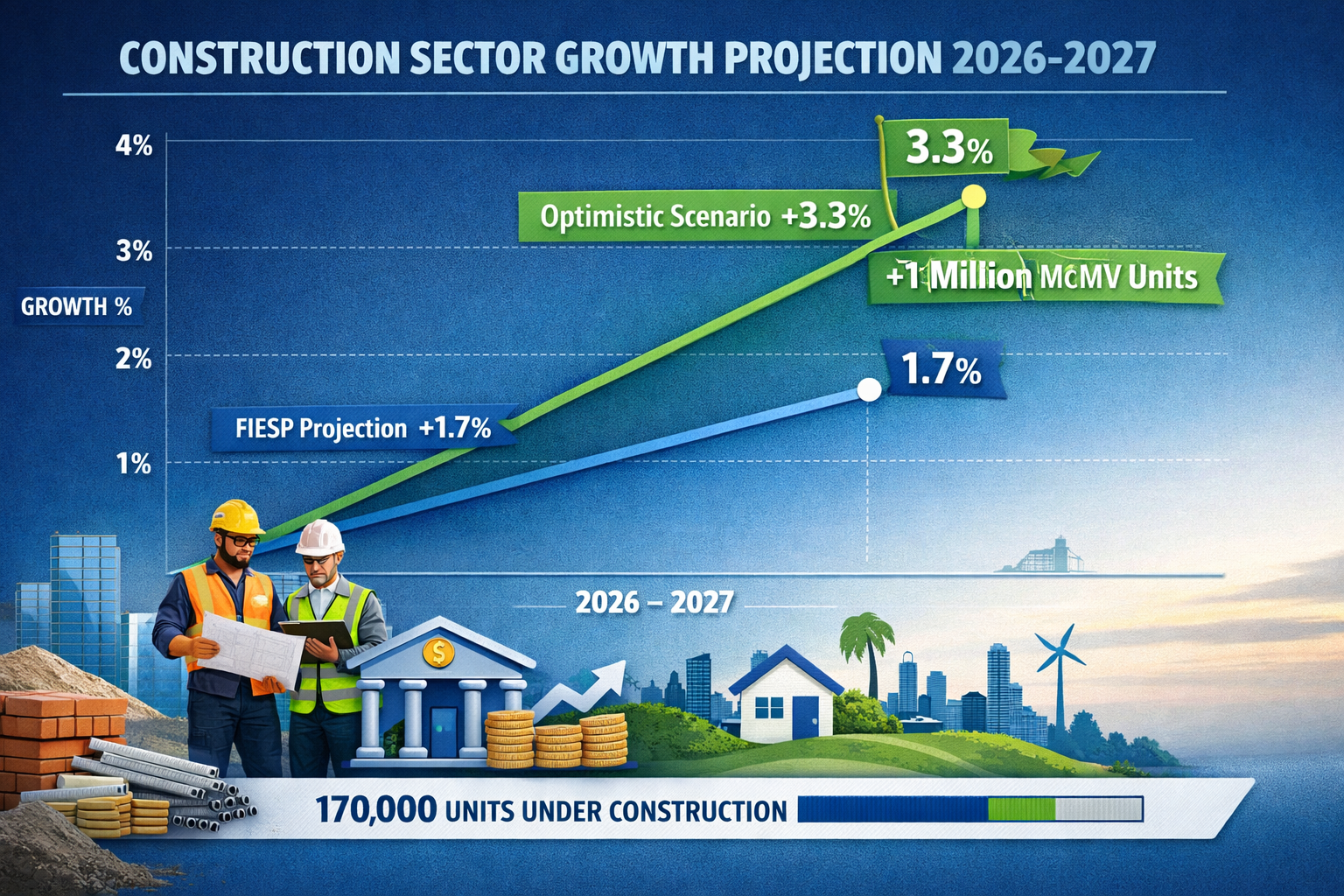

- 📈 Construction sector growth projected at 3.3% under optimistic scenarios, nearly double initial forecasts, driven by expanded housing credit availability[1]

- 🏘️ 2 million housing units already contracted under Minha Casa, Minha Vida (MCMV) program, with 1 million additional units planned for 2026[1]

- 🔄 Structural financing model transition beginning in 2026 will gradually increase savings fund allocation to real estate, creating more competitive lending environment through 2027[2]

Understanding Brazil’s Housing Credit Expansion Policy Changes

The landscape of Brazilian real estate financing underwent fundamental restructuring beginning January 2, 2026. These housing credit expansion policy changes represent the most significant shift in mortgage accessibility in over a decade, specifically designed to support residential development in regions where high construction costs previously blocked projects.

The New Mortgage Rules Framework

The updated mortgage financing rules introduced at the start of 2026 dramatically expand access for lower-income families. Households earning up to 4,700 Reais ($875) per month can now qualify for subsidized financing, a substantial increase from previous thresholds[1]. This expansion directly impacts regional markets where average incomes traditionally fell outside financing parameters.

Maximum property values have increased to 255,000-270,000 Reais in larger urban centers, enabling developers to build quality housing in secondary cities without pricing projects outside the financing envelope[1]. This adjustment accounts for regional construction cost variations that previously made many projects economically unfeasible.

The $39.8 Billion Investment Commitment

Brazil’s 2026 housing investment represents an unprecedented financial commitment structured across multiple funding sources:

| Funding Source | Amount | Purpose |

|---|---|---|

| Federal Budget Resources | $1.6 billion | Direct subsidies and program administration |

| FGTS Funds | $30.5 billion | Primary mortgage financing pool |

| Social Fund/Caixa Econômica | $7.4 billion | Reforma Casa Brasil program support |

| Total Investment | $39.8 billion | Comprehensive housing support |

This diversified funding structure ensures sustained capital availability throughout 2026 and beyond, providing developers with financing certainty essential for regional project planning[1].

Structural Financing Model Transition

Announced in October 2025, the structural financing model represents a long-term transformation of Brazil’s real estate financing architecture. The transition phase began in 2026, with full adoption scheduled for 2027[2].

Current regulations mandate that 65% of savings funds be allocated to housing financing. The new model will eventually reach 100% allocation, dramatically expanding available capital for mortgage lending[2]. This transition creates a more competitive lending environment as banks expand concession capacity and test internal systems during the implementation phase.

Additionally, the 20% compulsory savings requirement will be gradually eliminated over 10 years starting in 2027, replaced by a more flexible model that allows financial institutions greater discretion in real estate lending[4].

How Brazil’s New Mortgage Rules Are Making Previously Unviable Regional Projects Profitable

The practical impact of these policy changes extends far beyond theoretical improvements in credit access. Developers across Brazil’s regional markets are discovering that projects dismissed as financially impossible just months ago now present compelling investment opportunities.

Regional Market Transformation

Secondary cities and emerging regions face unique challenges that historically prevented residential development. High construction costs, limited local financing options, and income levels below traditional mortgage thresholds created a perfect storm of obstacles. The 2026 policy changes systematically address each barrier.

For developers exploring investment opportunities in Brazil’s property markets, the expanded income thresholds and increased property value limits unlock entirely new demographic segments. Families earning 3,500-4,700 Reais monthly—a substantial portion of regional populations—can now access financing that was previously unavailable.

The MCMV Program’s Regional Impact

The Minha Casa, Minha Vida (MCMV) program achieved remarkable results during its first three years under the current administration. 2 million units were already contracted through the end of 2025, reaching the original four-year target ahead of schedule[1]. An additional 1 million units are planned for contracting through the end of 2026[1].

These numbers translate to direct regional development opportunities. MCMV now accounts for roughly half of new housing launches in Brazil, creating material impact across the entire construction supply chain[1]. Regional developers can tap into this massive program to support projects that align with local housing needs.

“MCMV accounts for roughly half of new housing launches in Brazil, creating direct and material impact across the entire construction supply chain.” – Industry Analysis[1]

Construction Activity and Economic Multipliers

Currently, 170,000 units are under construction with expectations to deliver more than 100,000 housing units in 2026 under subsidized MCMV lines alone[1]. When including both subsidized and financed programs, over 1 million housing units are under construction nationwide[1].

This construction activity generates powerful economic multipliers in regional markets. Each housing unit creates demand for:

- 🔨 Local construction labor and skilled trades

- 🧱 Building materials and supply chain services

- 🚚 Transportation and logistics infrastructure

- 🏪 Retail and commercial services for new residents

- 🏫 Educational and healthcare facilities

For regions experiencing this development surge, the economic benefits extend well beyond the immediate construction phase, creating sustainable growth that further enhances property values and investment returns.

Revised Growth Projections

The construction sector’s growth outlook for 2026 has been substantially upgraded. Under optimistic scenarios supported by expanded housing credit availability, growth projections have been revised upward to 3.3%, compared to FIESP’s initial projection of just 1.7%[1].

This nearly doubled growth expectation reflects confidence in the policy changes’ ability to stimulate real activity. Infrastructure and social programs are identified as primary growth drivers, while MCMV sustains the popular and mid-range housing segments[1]. Developers focusing on emerging regions like Florianópolis can capitalize on this momentum.

Identifying Which Regions Benefit Most from Housing Credit Expansion

Not all regional markets benefit equally from Brazil’s housing credit expansion policy changes. Understanding which regions present the strongest opportunities requires analyzing multiple factors that determine project viability and profitability potential.

Key Regional Selection Criteria

Developers should evaluate regional opportunities based on these critical factors:

1. Income Distribution Alignment

Regions with substantial populations earning 3,000-4,700 Reais monthly present ideal targets. These households previously fell outside financing parameters but now qualify under expanded rules. Markets with concentrated populations in this income band offer the largest addressable customer base.

2. Construction Cost Dynamics

The increased maximum property values (255,000-270,000 Reais) make the most difference in regions where construction costs previously pushed projects above financing limits. Secondary cities with moderate construction costs relative to major metros benefit disproportionately.

3. Supply-Demand Imbalances

Regions experiencing population growth but limited recent residential development present compelling opportunities. Years of underbuilding due to financing constraints created pent-up demand that expanded credit access can now satisfy.

4. Infrastructure Development

Areas receiving state or federal infrastructure investment multiply the benefits of housing credit expansion. New transportation links, utilities, and public services enhance property values and accelerate regional development cycles.

Emerging Opportunity Zones

Several regional categories present particularly strong opportunities under the new financing framework:

Secondary Urban Centers

Cities with populations of 200,000-500,000 often possess economic diversity and employment bases sufficient to support housing demand, but lacked financing infrastructure. The FGTS fund expansion and MCMV program presence now make these markets accessible to developers.

Tourism-Adjacent Markets

Regions near established tourism destinations benefit from economic spillover while maintaining lower land and construction costs. The growth of regions like Florianópolis demonstrates how proximity to tourism centers creates sustainable residential demand.

Industrial Corridor Communities

Towns and cities along major industrial corridors experience steady employment growth but often lack adequate housing supply. Manufacturing and logistics employment creates stable income populations ideal for MCMV program targeting.

Agricultural Hub Peripheries

Communities surrounding major agricultural centers benefit from agribusiness prosperity while maintaining moderate cost structures. These markets often feature underserved populations with newly qualifying income levels.

Regional Risk Factors to Consider

While opportunities abound, developers must also evaluate regional risks:

- ⚠️ Political stability and local government support for development

- ⚠️ Environmental regulations that may complicate permitting

- ⚠️ Labor availability for construction workforce needs

- ⚠️ Market absorption rates to ensure demand matches supply

- ⚠️ Competition intensity from other developers entering newly viable markets

Developer Strategies to Capitalize on Policy Changes

Understanding the policy changes represents only the first step. Successful developers must implement strategic approaches that maximize the opportunities created by Brazil’s housing credit expansion.

Project Design Optimization

Align project specifications with the new financing parameters to maximize market accessibility:

Target the Sweet Spot

Design units priced at 220,000-255,000 Reais to capture the expanded financing envelope while maintaining healthy profit margins. This range accommodates regional construction costs while staying within maximum property value limits[1].

Unit Mix Strategy

Focus on 2-3 bedroom configurations that appeal to families in the 3,000-4,700 Reais monthly income range. These households typically include young families and dual-income couples seeking their first property purchase.

Amenity Selection

Include amenities that enhance value without pushing prices beyond financing limits. Community spaces, basic fitness facilities, and secure parking provide differentiation without excessive cost escalation.

Financing Partnership Development

Establish relationships with financial institutions actively expanding their mortgage portfolios under the new structural financing model:

The more competitive lending environment expected in 2026-2027 creates opportunities for developers to negotiate favorable terms as banks expand concession capacity[2]. Developers who establish early partnerships position themselves advantageously as institutions test internal systems during the transition phase.

Caixa Econômica Federal, as the primary MCMV program administrator, represents a critical partnership for regional developers. Understanding their approval processes and documentation requirements accelerates project timelines.

Phased Development Approach

Regional markets may lack the absorption capacity of major metros. Implement phased development strategies that:

- 📊 Test market demand with initial phases before committing full capital

- 💵 Generate cash flow from early sales to fund subsequent phases

- 🔄 Adjust offerings based on market feedback and sales velocity

- ⚡ Maintain flexibility to respond to changing market conditions

This approach mirrors successful strategies employed in emerging Florianópolis developments, where phased construction manages risk while capitalizing on market momentum.

Pre-Launch Marketing Investment

Regional markets often require more extensive buyer education than established metros. Families accessing mortgage financing for the first time need guidance through the process.

Invest in:

- 🎯 Educational seminars explaining financing options and qualification requirements

- 📱 Digital marketing campaigns targeting income-qualified demographics

- 🤝 Partnership programs with local employers and community organizations

- 📋 Simplified application processes that reduce friction for first-time buyers

Value Engineering for Regional Costs

Regional construction costs vary significantly from major metros. Implement value engineering strategies that optimize costs without compromising quality:

- 🏗️ Standardized designs that reduce architectural complexity

- 📦 Bulk material procurement leveraging multiple regional projects

- 👷 Local labor development programs to ensure skilled workforce availability

- 🔧 Construction methodology selection appropriate to regional capabilities

Developers who master regional cost optimization while maintaining quality standards achieve the strongest margins in newly viable markets.

Monitoring Policy Evolution

The structural financing model transition continues through 2027, with the 20% compulsory savings requirement gradually eliminated over 10 years starting 2027[4]. Developers must monitor ongoing policy evolution to anticipate future opportunities and adjust strategies accordingly.

Subscribe to industry publications, maintain relationships with banking partners, and participate in developer associations to stay informed about regulatory changes that may create additional advantages.

Long-Term Implications for Regional Development

Brazil’s housing credit expansion policy changes represent more than temporary stimulus—they signal a fundamental shift in how regional development will unfold over the coming decade.

Sustainable Regional Growth Patterns

The combination of expanded financing access and substantial capital allocation creates conditions for sustainable regional development rather than boom-bust cycles. The $30.5 billion in FGTS funds allocated to housing financing in 2026 alone provides a stable capital base that supports multi-year development pipelines[1].

This stability allows developers to plan long-term regional strategies rather than opportunistic single projects. Communities benefit from planned development that integrates with local infrastructure and economic development initiatives.

Wealth Building for Regional Populations

Expanded mortgage access enables wealth building for families previously excluded from homeownership. As regional populations build equity through homeownership, local economies strengthen through:

- 💰 Increased consumer spending power

- 🏘️ Community investment and maintenance

- 📈 Property value appreciation benefiting all owners

- 🎓 Educational and economic opportunities for children

These wealth-building effects create virtuous cycles that further enhance regional development prospects and property investment returns.

Infrastructure Investment Acceleration

Housing development drives infrastructure investment as municipalities respond to growing populations. Transportation improvements, utility expansion, and public service development follow residential growth, creating additional value for early-stage developers and investors.

Regions experiencing housing credit-driven development today will likely see significant infrastructure investment over the next 5-10 years, multiplying property value appreciation potential.

Competitive Dynamics Evolution

As more developers recognize opportunities in newly viable regional markets, competitive dynamics will evolve. First movers who establish market presence, develop local relationships, and build brand recognition before competition intensifies will maintain sustainable advantages.

The current window—with policy changes fresh and many developers still focused on traditional metros—presents optimal timing for regional market entry. Those exploring property investment opportunities should act decisively while competitive intensity remains moderate.

Banking Sector Transformation

The structural financing model’s transition creates lasting changes in how banks approach real estate lending. The eventual 100% allocation of savings funds to housing financing fundamentally expands available capital[2], while the gradual elimination of compulsory savings requirements increases institutional flexibility[4].

These banking sector changes will support sustained regional development well beyond 2026-2027, creating a more robust and accessible financing environment for decades to come.

Conclusion

Housing credit expansion policy changes implemented in 2026 are fundamentally transforming Brazil’s regional real estate development landscape. The combination of new mortgage rules effective January 2, 2026, $39.8 billion in total housing investment, and the structural financing model transition creates unprecedented opportunities for developers willing to look beyond traditional metro markets[1][2].

Previously unviable regional projects are now financially attractive due to expanded income thresholds reaching 4,700 Reais monthly, increased maximum property values of 255,000-270,000 Reais, and substantially enhanced capital availability through FGTS fund allocations[1]. The MCMV program’s achievement of contracting 2 million units ahead of schedule, with 1 million additional units planned for 2026, demonstrates the scale of opportunity[1].

Developers who successfully capitalize on these changes will:

✅ Identify regional markets with income distributions, construction costs, and supply-demand dynamics aligned with new financing parameters

✅ Design projects optimized for the 220,000-255,000 Reais price range that maximizes financing accessibility

✅ Establish banking partnerships early in the structural financing model transition to secure favorable lending terms

✅ Implement phased development strategies appropriate to regional absorption capacity

✅ Invest in buyer education and marketing to reach newly qualified demographics

The construction sector’s revised growth projection of 3.3%—nearly double initial forecasts—reflects confidence in these policy changes’ ability to drive real economic activity[1]. For developers and investors exploring opportunities in Brazil’s evolving real estate landscape, the time to act is now.

Regional markets that seemed financially impossible just months ago are opening to development. Those who move decisively while competitive intensity remains moderate will establish market positions that generate returns for years to come. The policy framework is in place, the capital is allocated, and the opportunity is clear—Brazil’s regional housing development transformation has begun.

For more information about emerging investment opportunities and regional development projects, explore Quadragon’s current developments and stay informed through our latest news and market insights.

References

[1] Brazils Construction Sector 2026 Housing Programs Support Rates High Risks Persist – https://www.fastmarkets.com/insights/brazils-construction-sector-2026-housing-programs-support-rates-high-risks-persist/

[2] New Real Estate Financing Model What Changes In 2026 And How It Affects Those Who Invest In Bombinhas – https://roccoimob.com/en/new-real-estate-financing-model-what-changes-in-2026-and-how-it-affects-those-who-invest-in-bombinhas/

[4] Brazil Mortgage Finance Changes Benefit Large Banks Test Smaller 05 11 2025 – https://www.fitchratings.com/research/banks/brazil-mortgage-finance-changes-benefit-large-banks-test-smaller-05-11-2025