Brazil’s benchmark interest rate hit 14.75% in March 2026 before a modest 25-basis-point cut brought it to 14.50% in April — still among the highest real policy rates of any major economy on the planet [7]. For developers working outside the protective umbrella of subsidized housing programs, that number is not just a macroeconomic headline. It is the single most powerful force determining whether a mid-market project gets launched, delayed, or quietly shelved.

How Brazil’s High Selic Rate Is Reshaping Development Feasibility for Mid-Market Projects is a question every developer, investor, and capital allocator in the country must answer with precision right now. With IPCA inflation running near 3.8–4.0% year-on-year as of early 2026 and market expectations still above the Central Bank’s 3.0% target, real interest rates remain punishingly high [1]. That gap between nominal rates and inflation keeps hurdle rates elevated, squeezes equity returns, and forces a fundamental rethink of how mid-market projects are structured, priced, and sold.

Key Takeaways

- 🏗️ The Selic at 14.50% keeps real borrowing costs near double digits, making marginal mid-market projects extremely difficult to justify on standard IRR models.

- 📉 Pre-sales thresholds are rising — developers must now secure a larger percentage of units before banks release construction credit, tightening launch windows.

- 💼 Capital stack design is being restructured — equity contributions are increasing, mezzanine debt is more expensive, and phased releases are replacing full-tower launches.

- 🏘️ Product positioning is shifting — smaller units, flexible payment plans, and amenity-rich designs are being used to defend absorption rates in a price-sensitive market.

- 📅 BBVA Research projects Selic averaging 11.75% in 2026 and 10.00% in 2027 [4] — meaning developers must plan for a prolonged high-rate environment, not a quick pivot.

The Mechanics: Why the Selic Hits Mid-Market Developers Hardest

Subsidized vs. Non-Subsidized: A Tale of Two Markets

Brazil’s housing market is structurally divided. Programs like Minha Casa Minha Vida insulate lower-income segments from Selic movements through fixed subsidized rates. The mid-market segment — broadly defined as units priced between R$500,000 and R$1.5 million — receives no such buffer. Every basis point the Copom moves translates directly into higher construction financing costs, higher opportunity costs for equity, and higher mortgage rates for end buyers.

This asymmetry is critical. When the Selic rises, subsidized housing demand can remain stable or even increase as buyers shift down-market. Mid-market demand, however, compresses from both sides: buyers face more expensive mortgages, and developers face higher carrying costs on land banks and construction loans.

How the Rate Transmits Into Project Economics

The transmission mechanism works through several channels simultaneously:

| Channel | Impact at 14.50% Selic |

|---|---|

| Construction financing (CDI-linked) | Effective rate 16–18% p.a. |

| Equity hurdle rate (opportunity cost) | 17–20% p.a. minimum |

| End-buyer mortgage rate (SBPE) | 12–14% p.a. effective |

| Land bank carrying cost | Compounding monthly |

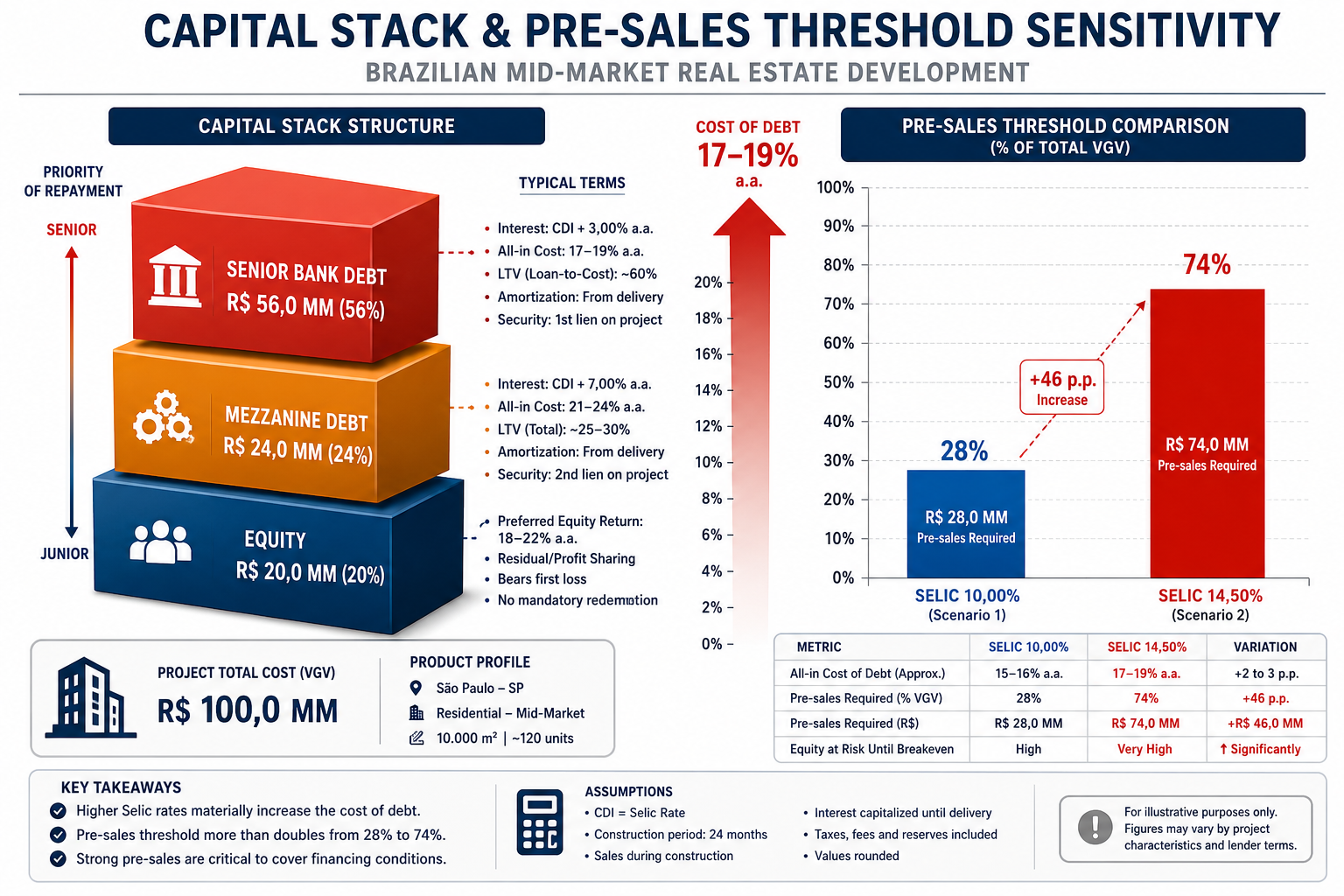

| Pre-sales requirement (bank threshold) | Typically 30–40% of units |

“When the risk-free rate sits above 14%, every project is competing against Tesouro Direto. Developers must offer a substantial premium to attract equity — and that premium comes directly out of feasibility.”

Fitch Ratings flagged in February 2026 that high interest rates are eroding Brazilian corporates’ financial cushions after a prior credit boom, increasing interest burdens and reducing headroom under leverage covenants [8]. For mid-market developers — who typically carry thinner margins and have less access to capital markets than large publicly listed incorporadoras — this dynamic is acute.

How Brazil’s High Selic Rate Is Reshaping Development Feasibility: Launch Timing and Pre-Sales Strategy

The Pre-Sales Trap

Under normal market conditions, a developer might launch a tower, achieve 20–25% pre-sales, and trigger construction financing from a bank. In the current environment, that threshold has quietly risen. Banks — facing their own cost-of-capital pressures and tightening credit standards — are demanding 30–40% pre-sales before releasing credit lines. Some institutions are requiring even higher levels for projects in secondary markets or from developers without established track records.

This creates a structural problem: the cost of the pre-sales period itself has increased. Every month a developer holds a land parcel while running a sales campaign, the carrying cost compounds at CDI-linked rates. A six-month pre-sales campaign that once cost R$800,000 in financing charges might now cost R$1.2 million or more. That delta has to be absorbed somewhere — either in reduced land acquisition prices, compressed developer margins, or higher unit prices passed to buyers.

The IMF noted in its October 2025 analysis that new loan volumes in Brazil had been falling since April 2025, confirming that monetary tightening is now fully biting — and that banks are first tightening standards and pricing risk more aggressively for smaller, mid-market borrowers [3]. This is not a theoretical risk. It is already reshaping which projects get financed.

Timing the Launch Window

Smart developers are now treating launch timing as a strategic variable, not just a marketing decision. Key considerations include:

- 📅 Avoid launching during Copom meeting cycles when rate uncertainty peaks and buyer sentiment softens.

- 📊 Monitor the yield curve — long-term interest rates were under pressure as recently as February 2026 [10], signaling that even if the Selic cuts continue, mortgage rates may not fall proportionally in the near term.

- 🏦 Secure bank pre-approvals before public launch to reduce the gap between sales campaign start and credit release.

- 📋 Build longer pre-sales periods into feasibility models — assume 8–12 months rather than 4–6 months for mid-market projects in 2026.

Phased Releases as a Risk Management Tool

One of the most significant tactical shifts in 2026 is the move from full-tower launches to phased releases. Rather than offering all units simultaneously, developers are releasing 30–40% of inventory in an initial phase, using those sales to validate pricing, trigger financing, and reduce exposure before committing to the full project.

This approach has real advantages in a high-rate environment:

✅ Reduces pre-sales period carrying costs by shortening the time to first credit release ✅ Allows pricing adjustments between phases based on market absorption data ✅ Limits downside if demand proves weaker than projected ✅ Gives buyers in later phases confidence from a partially sold project

The Tramonto development by Quadragon is an example of how disciplined project execution — including foundation completion milestones — signals credibility to buyers and financiers alike, a critical trust signal when market conditions are tight. For more on how sales performance is evolving in this environment, the analysis of how sales performance is transforming Florianópolis’s real estate market offers useful context.

Capital Stack Design and Product Positioning in a High-Rate World

Redesigning the Capital Stack

How Brazil’s High Selic Rate Is Reshaping Development Feasibility for Mid-Market Projects is perhaps most visible in how developers are restructuring their capital stacks. The classic Brazilian development model — thin equity, heavy reliance on construction credit, and buyer installments funding construction — is under stress.

The new capital stack reality for mid-market projects in 2026:

- Equity contribution: Rising from 20–25% to 30–40% of total project cost

- Construction credit (bank): More expensive, more covenant-heavy, released later

- Mezzanine/bridge debt: Available but priced at CDI + 8–12%, making it viable only for short-duration needs

- Buyer installments (permuta financeira): Still the most cost-effective funding source — maximizing installment collection during construction is now a priority

BBVA Research’s March 2026 outlook projects the Selic averaging 11.75% in 2026 and 10.00% in 2027, with explicit warnings that global factors and fiscal risks represent upside risks to those forecasts [4]. The Central Bank itself has emphasized caution, citing upside inflation risks and fiscal uncertainty [9]. This means developers cannot count on a rapid rate normalization to rescue marginal projects. Feasibility models must work at current rates, not hoped-for future rates.

Product Positioning: Smaller, Smarter, More Flexible

When borrowing costs are high, affordability becomes the dominant buyer concern. Mid-market developers are responding with product adjustments that protect absorption rates without necessarily cutting headline prices:

Unit Size Optimization Reducing average unit size from 90–110m² to 70–85m² lowers the absolute ticket price while maintaining per-square-meter pricing. This keeps monthly mortgage installments within buyer qualification thresholds.

Flexible Payment Structures Offering larger down payments in exchange for discounts, or structuring installments to align with buyer income cycles, can meaningfully improve qualification rates. When mortgage rates are running at 12–14% effective, every R$10,000 reduction in financed amount saves a buyer approximately R$120–150/month — which can be the difference between qualifying and not.

Amenity Differentiation In a high-rate environment, buyers who do commit are making a long-term decision. They demand value beyond square footage: coworking spaces, pet areas, rooftop gardens, and smart-home technology justify price premiums and reduce price sensitivity.

For investors evaluating where mid-market fundamentals remain strongest despite rate pressure, understanding the best places to invest in Brazilian property is essential context. Markets like Florianópolis — where the Ingleses region continues to show strong infrastructure growth and appreciation — demonstrate that location quality can partially offset rate headwinds by sustaining demand from high-income buyers less sensitive to financing costs.

Buyer Qualification: The Hidden Bottleneck

Rising rates do not just affect developers — they directly shrink the pool of qualified buyers. A household earning R$15,000/month could qualify for a R$600,000 mortgage at 10% effective rates. At 13% effective, that same household qualifies for roughly R$480,000 — a 20% reduction in purchasing power.

Practical implications for sales teams:

- 🎯 Pre-qualify buyers earlier in the funnel, before marketing spend is committed

- 📑 Partner with multiple mortgage brokers to access the widest range of bank products

- 💡 Educate buyers on FGTS utilization strategies to reduce financed amounts

- 📉 Build buyer qualification rate assumptions into absorption models (assume 15–20% fall-through on signed contracts)

The investment case for studio and compact units — which carry lower absolute prices and therefore lower financing requirements — has strengthened considerably. The analysis of the advantages of investing in studios in Florianópolis illustrates how this product category is increasingly attractive both to end-buyers and investors in a high-rate context.

Navigating the Medium Term: What Developers Must Plan For

The Rate Path Ahead

The Central Bank’s April 2026 cut to 14.50% was accompanied by clear signals of a slower easing cycle than markets had priced in late 2025 [7]. BBVA Research’s forecast of 11.75% average Selic for 2026 implies rates will remain in double digits through year-end [4]. Even the more optimistic scenario of 10.00% in 2027 still represents a real rate environment that is historically tight by Brazilian standards.

For developers with projects in the pipeline, this creates a planning imperative:

“A project that only works at 9% Selic is not a 2026 project. Feasibility must be stress-tested at current rates and remain viable even if easing is slower than consensus.”

Credit Availability: Strong but Narrowing

An important nuance: despite the high Selic, Brazil’s credit market has not frozen. The IMF highlighted in October 2025 that strong income growth, fintech-driven financial inclusion, and capital market expansion have kept aggregate credit growth surprisingly robust [3]. However, the same analysis confirmed that new loan volumes have been falling since April 2025 — and that tightening hits marginal borrowers first [3].

For mid-market developers, this means credit is available — but at a price and with conditions that require careful management. The developers who will succeed in 2026 are those who:

- Maintain strong balance sheets with low leverage ratios

- Diversify funding sources beyond a single bank relationship

- Build equity reserves sufficient to bridge the pre-sales period without distress

- Choose projects with genuine demand drivers — not just favorable land prices

Those interested in understanding the broader market trajectory can explore the latest market news and analysis from Quadragon for ongoing updates on how these dynamics are playing out in key Brazilian markets.

Conclusion: Actionable Steps for Mid-Market Developers in 2026

How Brazil’s High Selic Rate Is Reshaping Development Feasibility for Mid-Market Projects is not a temporary disruption — it is a structural recalibration that demands a permanent upgrade in how projects are conceived, financed, and sold. The developers who treat this as a short-term inconvenience to wait out will find themselves holding depreciating land banks and unviable feasibility models. Those who adapt will find opportunity in a market where weaker competitors are stepping back.

Actionable next steps for developers and investors:

✅ Rebuild feasibility models at 14.50% Selic — stress-test at 15.00% and only proceed if the project works ✅ Increase equity contribution targets to 35–40% of total project cost to reduce bank dependency ✅ Adopt phased release strategies — launch 35–40% of units in Phase 1 before committing to full construction ✅ Optimize unit mix toward smaller, lower-ticket products that keep buyers within qualification thresholds ✅ Extend pre-sales period assumptions to 10–12 months in feasibility models ✅ Pre-qualify buyers aggressively and build 15–20% contract fall-through into absorption projections ✅ Focus on high-demand locations where organic demand can sustain absorption independent of rate cycles ✅ Monitor the Copom calendar and align launch campaigns to periods of rate stability, not uncertainty

For those evaluating specific opportunities, reviewing current Quadragon developments provides a concrete view of how disciplined developers are structuring projects to remain viable in this environment. And for investors weighing the off-plan purchase decision, understanding why buying off-plan can amplify returns remains relevant — particularly when projects are structured with the rate environment in mind from the outset.

The Selic will eventually normalize. The developers who build the discipline, capital efficiency, and product intelligence required to operate at 14.50% will be extraordinarily well-positioned when it does.

References

[1] Brazil Inflation 2026 Guide – https://www.riotimesonline.com/brazil-inflation-2026-guide/

[2] Spizot Inflation Selic Activity 7401349446917308416 Pyr – https://www.linkedin.com/posts/spizot_inflation-selic-activity-7401349446917308416-PYR_

[3] Explaining Strong Credit Growth In Brazil Despite High Policy Rates – https://www.imf.org/en/news/articles/2025/10/09/explaining-strong-credit-growth-in-brazil-despite-high-policy-rates

[4] Brazil Economic Outlook March 2026 – https://www.bbvaresearch.com/en/publicaciones/brazil-economic-outlook-march-2026/

[5] Interest Rate – https://tradingeconomics.com/brazil/interest-rate

[6] Policy Rate – https://www.ceicdata.com/en/indicator/brazil/policy-rate

[7] Brazil Central Bank Cuts Interest Rates By 25 Bp Expected 2026 04 29 – https://www.reuters.com/world/americas/brazil-central-bank-cuts-interest-rates-by-25-bp-expected-2026-04-29/

[8] High Rates Cut Brazil Corporates Financial Cushions After Credit Boom 26 02 2026 – https://www.fitchratings.com/research/corporate-finance/high-rates-cut-brazil-corporates-financial-cushions-after-credit-boom-26-02-2026

[9] Selicrate – https://www.bcb.gov.br/en/monetarypolicy/selicrate

[10] Long Term Interest Rates Remain Under Pressure Ahead Of Selic Cut – https://valorinternacional.globo.com/markets/news/2026/02/09/long-term-interest-rates-remain-under-pressure-ahead-of-selic-cut.ghtml