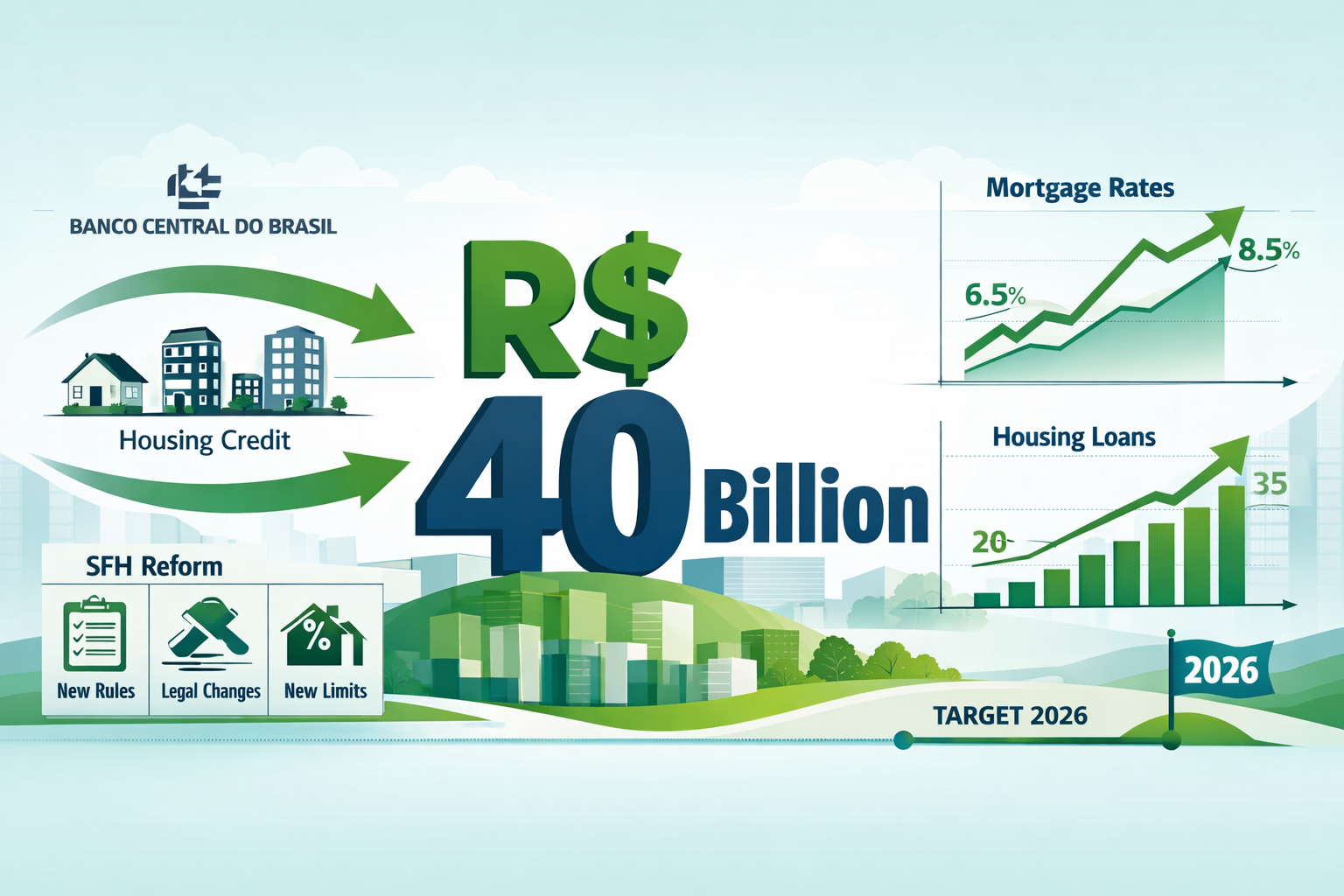

Brazil’s housing finance system just received its most significant structural upgrade in over a decade — and the numbers are staggering. The New SFH Credit Model 2026: R$40B Injection Tactics for Mid-Tier Launches Post-Cap Hike represents a deliberate policy pivot: raising the SFH (Sistema Financeiro de Habitação) financing ceiling to R$2.25 million, expanding loan-to-value (LTV) ratios to 80%, and channeling an estimated R$40 billion into a segment of the market that has long been underserved. With the Selic rate moderating from its 2023–2024 peaks and October 2025 regulatory reforms now fully in effect, developers and investors are racing to position themselves ahead of an estimated 80,000 additional housing units unlocked by the new rules.

Key Takeaways 📌

- 🏗️ R$40 billion in new SFH credit is being directed toward mid-tier residential launches in 2026, following October 2025 ceiling reforms.

- 📈 The SFH financing cap rose to R$2.25 million, opening the mid-to-upper-mid market to regulated, subsidized lending for the first time.

- 🏠 LTV ratios expanded to 80%, reducing the equity barrier for buyers and accelerating sales velocity for developers.

- 🔑 An estimated 80,000 extra housing units are now viable under the new credit framework, reshaping launch pipelines nationwide.

- 📉 Moderating Selic rates amplify the effect of these reforms, compressing mortgage costs and boosting purchasing power across income bands.

Understanding the October 2025 SFH Reforms: What Actually Changed

Before diving into developer tactics, it is essential to understand the structural shift that created this opportunity. Brazil’s SFH has historically served lower-to-middle income buyers through regulated interest rates and mandatory FGTS (Fundo de Garantia do Tempo de Serviço) allocations. The October 2025 reforms, announced by the Conselho Monetário Nacional (CMN), made three decisive changes:

The New Ceiling: R$2.25 Million

Previously capped at R$1.5 million in most major markets, the new R$2.25 million ceiling fundamentally repositions which buyers and which projects qualify for SFH financing. This is not a marginal adjustment — it is a 50% increase in the maximum property value eligible for regulated credit.

“The ceiling hike effectively created a new addressable market: the mid-tier buyer who earns too much for Minha Casa Minha Vida but was previously priced out of SFH-eligible properties in high-demand urban markets.”

LTV Expansion to 80%

Raising the loan-to-value ratio from the previous 70–75% threshold to a uniform 80% has two powerful effects:

- Reduces the required down payment — a buyer purchasing a R$1.8M property now needs R$360,000 upfront instead of R$450,000+.

- Increases purchasing power — more buyers qualify at higher price points without additional income.

The R$40 Billion Credit Envelope

The CMN and Banco Central do Brasil coordinated a directed credit envelope of approximately R$40 billion specifically targeting SFH-eligible launches in 2026. This capital flows primarily through Caixa Econômica Federal and Banco do Brasil, with private banks incentivized through reserve requirement adjustments.

| Reform Element | Pre-October 2025 | Post-October 2025 |

|---|---|---|

| SFH Financing Ceiling | R$1.5 million | R$2.25 million |

| Maximum LTV | 70–75% | 80% |

| Directed Credit Volume | ~R$28B annually | ~R$40B (2026 target) |

| Estimated New Units Unlocked | — | ~80,000 |

| Eligible Market Segment | Low-to-mid | Mid-to-upper-mid |

New SFH Credit Model 2026: R$40B Injection Tactics for Mid-Tier Launches Post-Cap Hike — Developer Strategies

The reforms did not automatically translate into sales. Developers who are capturing disproportionate market share in 2026 are deploying specific tactics to leverage the new credit architecture. Here is what the most competitive operators are doing:

Tactic 1: Repricing Existing Pipelines Into the SFH Window 🏢

Many developers held land banks and approved projects originally conceived for the free-market (SFI) segment — properties priced between R$1.5M and R$2.5M that previously sat outside SFH eligibility. With the new R$2.25M ceiling, a significant portion of these projects can now be repositioned as SFH-eligible launches without redesigning the product.

The tactical move: adjust unit mix and finishing specifications to land the majority of units in the R$1.8M–R$2.2M band — squarely within SFH territory while maintaining margin.

Tactic 2: Structuring Launches Around 80% LTV Marketing

Developers are building entire sales campaigns around the 80% LTV message. The pitch to buyers is straightforward: “Finance R$1.8 million with only R$360,000 down.” For a mid-tier buyer in markets like Florianópolis, Campinas, or Curitiba, this is a transformational offer.

For those exploring real estate investment opportunities in Brazil’s high-growth markets, the LTV expansion is particularly relevant — it lowers the capital barrier for investors who previously needed to deploy more equity per unit.

Tactic 3: Speed-to-Launch Acceleration

The R$40 billion credit envelope is not unlimited in time. Developers who understand the policy cycle know that directed credit programs have windows. The tactical imperative is launching in H1 2026 before potential credit tightening in late 2026 or 2027 if inflation pressures resurface.

This has created a notable acceleration in construction timelines and regulatory approvals. Projects that might have launched in 2027 are being fast-tracked. For an example of what accelerated construction execution looks like in practice, see the progress updates on Tramonto foundations and construction pace.

Tactic 4: Geographic Targeting — Secondary Cities With Primary Demand

The R$2.25M ceiling is most impactful in markets where property values have been rising rapidly but were previously straddling the old SFH limit. Secondary cities with strong internal migration and economic growth — particularly coastal and tech-hub markets — are seeing the most aggressive developer activity.

Florianópolis is a prime example. The Grande Florianópolis real estate market has seen sustained price appreciation driven by lifestyle migration, remote work trends, and infrastructure investment. Under the new SFH model, mid-tier launches in neighborhoods like Ingleses and Canasvieiras now qualify for regulated financing that simply did not exist under the old ceiling.

Tactic 5: Pre-Sale Financing Partnerships With Caixa and Bradesco

Savvy developers are not waiting for buyers to arrange their own credit. They are pre-negotiating credit lines with Caixa Econômica Federal and major private banks, arriving at launch events with pre-approved financing packages tailored to their specific project’s price range and LTV structure.

This “turnkey financing” approach reduces buyer friction dramatically — a buyer at a launch event can receive a conditional pre-approval within 48 hours rather than navigating the bank relationship independently.

The Selic Rate Context: Why Timing Matters in 2026

The New SFH Credit Model 2026: R$40B Injection Tactics for Mid-Tier Launches Post-Cap Hike does not operate in isolation from Brazil’s broader monetary environment. The interaction between the SFH reforms and the Selic trajectory is critical to understanding why 2026 is a uniquely favorable window.

Selic Moderation and Mortgage Cost Compression

After peaking above 13% in 2023–2024, the Selic rate has been on a moderated path. SFH-regulated mortgages are capped at TR + 12% per annum (or equivalent), which means they are already below market rates. As the Selic moderates, the spread between SFH rates and free-market rates widens, making SFH-eligible properties significantly more attractive to buyers.

The math for a buyer in 2026:

- Property value: R$2.0M

- SFH loan (80% LTV): R$1.6M

- SFH rate: ~10.5% p.a. (TR + regulated margin)

- Free-market equivalent rate: ~14–15% p.a.

- Monthly payment difference: approximately R$4,000–R$6,000

That difference is not marginal — it is the difference between a purchase being financially viable or not for the mid-tier buyer.

Sales Performance Trends Reinforce the Opportunity

The sales performance transformation in Florianópolis’s real estate market shows how credit availability directly correlates with velocity. Markets with strong SFH penetration consistently outperform in units sold per launch event and in time-to-sellout metrics.

Mid-Tier Buyer Profile: Who Benefits Most From the New Model?

Understanding the target buyer unlocks better product design and marketing. The mid-tier SFH buyer in 2026 has a specific profile:

- 👤 Household income: R$15,000–R$35,000/month

- 🏙️ Location preference: Urban or peri-urban, proximity to services

- 📱 Digital-first: Research conducted online, expects digital pre-approval tools

- 🏘️ Unit preference: 2–3 bedroom apartments, 65–110m², with amenity packages

- 💰 Investment horizon: Mix of primary residence and investment buyers

This buyer was previously caught in a gap: too affluent for Minha Casa Minha Vida, but facing free-market mortgage rates that made mid-tier purchases painful. The new SFH ceiling closes that gap decisively.

For developers considering studio or compact unit formats within this segment, the investment case for studios in Florianópolis provides relevant demand analysis.

What Buyers Are Looking For in SFH-Eligible Launches

| Feature | Priority Level |

|---|---|

| SFH financing eligibility (confirmed) | 🔴 Critical |

| Pre-approved bank partnerships | 🔴 Critical |

| Location in high-appreciation corridor | 🟠 High |

| Amenity package (gym, pool, coworking) | 🟠 High |

| Delivery timeline under 36 months | 🟡 Medium |

| Sustainable building certifications | 🟡 Medium |

Risk Factors and Considerations for Developers and Investors

No credit expansion is without risk. The New SFH Credit Model 2026: R$40B Injection Tactics for Mid-Tier Launches Post-Cap Hike creates opportunity, but also introduces specific risks that must be managed:

⚠️ Risk 1: Inflation Resurgence and Selic Reversal

If Brazilian inflation accelerates in late 2026 or 2027, the Banco Central do Brasil may be forced to raise the Selic again. This would compress the SFH rate advantage and potentially reduce buyer qualification rates. Developers launching in H2 2026 should stress-test their sales projections against a +200bps Selic scenario.

⚠️ Risk 2: Credit Concentration in Caixa

With Caixa Econômica Federal handling the majority of SFH disbursements, any operational bottleneck or policy shift at Caixa directly affects developer cash flow. Diversifying financing partnerships — including private bank credit lines — is a prudent hedge.

⚠️ Risk 3: Construction Cost Inflation

The acceleration of mid-tier launches creates demand pressure on construction inputs — steel, cement, skilled labor. Developers who lock in supply contracts early and maintain contingency buffers of 12–15% in project budgets will be better positioned to protect margins.

⚠️ Risk 4: Regulatory Rollback

Credit policy in Brazil has historically been subject to political cycles. The current framework is favorable, but developers should structure projects to remain viable even if LTV ratios are reduced back to 75% or the ceiling is adjusted downward.

For investors considering alternative or complementary asset structures alongside real estate, the intersection of cryptocurrency and real estate development is an emerging area worth monitoring.

Actionable Framework: Evaluating a Mid-Tier SFH Launch in 2026

For developers and investors evaluating specific projects, the following framework helps assess SFH credit model alignment:

Step 1 — Price Band Validation Confirm that the majority of units (>60%) price between R$900K and R$2.25M. Units above the ceiling require free-market financing and will face higher buyer resistance.

Step 2 — LTV Stress Test Model buyer qualification at 80% LTV with SFH rates. If fewer than 70% of target buyers qualify at current income levels, reconsider unit sizing or pricing.

Step 3 — Bank Partnership Confirmation Secure a letter of intent from at least one SFH-accredited lender (Caixa, Bradesco, Itaú) before launch. This is now a marketing asset, not just a back-office requirement.

Step 4 — Geographic Demand Validation Confirm the target market has demonstrated absorption velocity. High-growth corridors like the Ingleses region in Florianópolis show strong fundamentals for mid-tier SFH products.

Step 5 — Launch Timing Target H1 2026 for maximum credit availability. Build in 90-day buffer for regulatory approvals.

For those looking to explore specific projects already aligned with this framework, the current development portfolio offers examples of launches structured for the post-reform environment.

Conclusion: Positioning for the SFH Credit Window in 2026

The New SFH Credit Model 2026: R$40B Injection Tactics for Mid-Tier Launches Post-Cap Hike is not a theoretical policy discussion — it is an active, time-sensitive market opportunity. The October 2025 reforms have fundamentally restructured who can buy, how much they can borrow, and at what cost. The R$40 billion credit envelope, combined with an 80% LTV ceiling and a R$2.25M property cap, has unlocked approximately 80,000 additional units of viable mid-tier demand.

Actionable next steps for developers and investors:

- ✅ Audit your pipeline — identify projects that can be repositioned into the R$1.5M–R$2.25M SFH band without compromising margins.

- ✅ Secure bank partnerships now — pre-approved credit packages are a competitive differentiator at launch events.

- ✅ Target high-absorption secondary markets — coastal cities and tech hubs with migration inflows offer the strongest demand fundamentals.

- ✅ Launch in H1 2026 — credit windows have cycles; early movers capture the deepest liquidity.

- ✅ Build risk buffers — 12–15% construction cost contingency and Selic stress-testing are non-negotiable in the current environment.

The developers who treat the new SFH model as a strategic architecture — not just a financing backdrop — will define the mid-tier residential market for the next three to five years. The window is open. The capital is allocated. The question is who moves first and with the most precision.

To explore developments already aligned with this new credit framework, contact the Quadragon team for a detailed project and financing consultation.

References

[1] 1977 12 18 Djvu – https://archive.org/stream/dailycolonist19771218/1977_12_18_djvu.txt