The Port of Santos is experiencing an unprecedented logistics transformation that’s capturing the attention of institutional investors worldwide. As Brazil’s largest port handles record cargo volumes and undergoes massive infrastructure expansion, the Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors represents one of the most compelling opportunities in Latin American commercial real estate. With e-commerce growth driving insatiable demand for modern warehouse space and supply chain re-shoring creating structural tailwinds, developers partnering with institutional capital are positioning themselves to capitalize on this multi-billion-dollar expansion.

The convergence of several powerful trends—record-low vacancy rates, government infrastructure investment through the Novo PAC program, and strategic capacity expansions by global operators—has created a perfect storm for logistics property development. The Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors isn’t just a headline; it’s a fundamental shift in how institutional capital views Brazilian industrial assets.

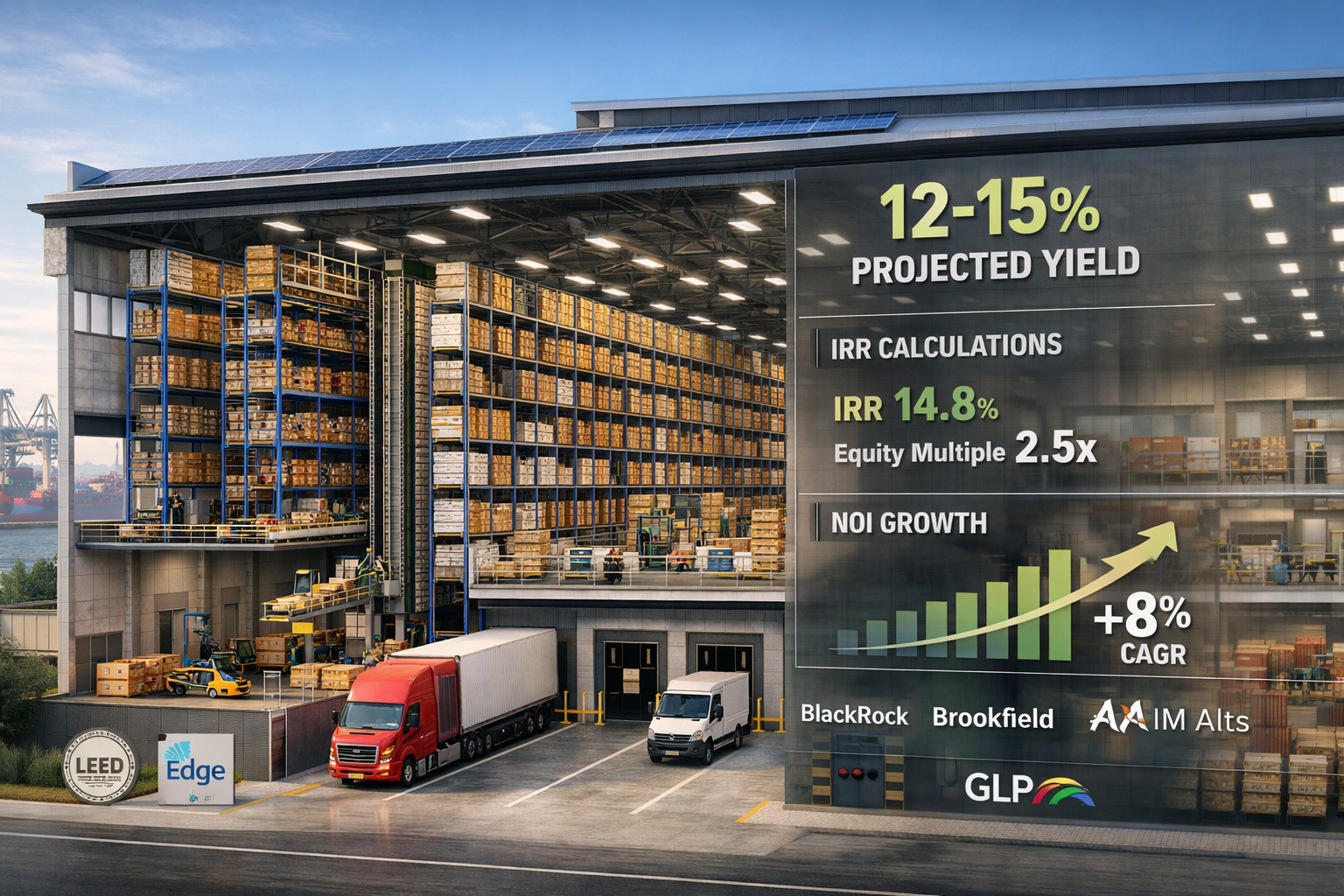

Key Takeaways

- 📊 Record Growth: Port of Santos handled 12.7 million tonnes in January 2026, representing 9.5% year-over-year growth, with container volumes reaching 1.3 million TEUs in 2025

- 💰 Strong Returns: Modern logistics warehouses near Santos are delivering 12-15% annual returns for institutional investors, driven by record-low vacancy rates and e-commerce demand

- 🏗️ Massive Investment: Over R$1.6 billion in port expansion projects underway, with total Brazilian port sector investments projected at USD 7.2 billion by 2026

- 🚢 Capacity Expansion: Santos terminal capacity increasing from 1.3 million to 2.1 million TEUs by 2028, representing 25% growth and creating significant warehouse demand

- 🎯 Strategic Positioning: Novo PAC infrastructure improvements and supply chain re-shoring trends position Santos as Latin America’s premier logistics gateway

Understanding the Port of Santos Infrastructure Expansion

Record-Breaking Performance Drives Development Demand

The Port of Santos has shattered performance records throughout 2025 and into 2026, establishing itself as an undeniable powerhouse in global trade. In January 2026 alone, the port handled 12.7 million tonnes of cargo, marking a 9.5% increase compared to the 11.6 million tonnes processed in January 2025.[5] This remarkable throughput demonstrates the sustained momentum that’s fueling warehouse development opportunities across the Santos corridor.

DP World’s Santos terminal exemplifies this explosive growth trajectory. The facility handled a record 1.3 million TEUs (twenty-foot equivalent units) in 2025, surpassing the previous 2024 record of 1.25 million TEUs and representing 14% annual growth.[1] This isn’t incremental improvement—it’s transformational expansion that requires proportional growth in supporting logistics infrastructure.

Multi-Billion Dollar Capacity Investments

To accommodate this surging demand, major operators have committed unprecedented capital to expansion projects. DP World approved R$1.6 billion (US$306 million) in new investments designed to expand terminal capacity from 1.3 million TEUs to 1.7 million TEUs by the end of 2026, with subsequent phases increasing total capacity to 2.1 million TEUs by 2028—a cumulative 25% increase from 2025 levels.[1]

These investments include tangible infrastructure improvements that directly impact warehouse development viability:

- 190-meter quay extension currently under construction (40 meters dedicated to pulp exports, 150 meters to container operations)[2]

- Four new quay cranes to accelerate vessel turnaround times

- 15 rubber-tyred gantry (RTG) cranes for improved yard efficiency

- 40 internal transfer vehicles (ITVs) aligned with decarbonization strategies[3]

Since entering Brazil in 2013, DP World has invested over R$3 billion (US$574 million) in port infrastructure, logistics capacity, and multimodal connectivity at Santos.[1] This long-term commitment signals confidence in the region’s structural growth potential—confidence that institutional investors are increasingly sharing.

The STS-10 Mega-Terminal: Game-Changing Expansion

Perhaps the most significant catalyst for the Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors is the upcoming STS-10 mega-terminal auction scheduled for 2026. This project involves planned investments of BRL 6.4 billion (approximately USD 1.2 billion) to construct a 1.3-kilometer quay and modernize 622,000 square meters of port facilities.[4]

The STS-10 terminal alone will increase overall port container handling capacity by 50%, pushing annual throughput to approximately 10 million units per year.[4] This magnitude of expansion creates immediate demand for hundreds of thousands of square meters of Class A warehouse space to support import/export operations, cross-docking facilities, and value-added logistics services.

E-Commerce and Supply Chain Dynamics Driving Warehouse Demand

Brazil’s E-Commerce Explosion

The Brazilian e-commerce market has experienced explosive growth, fundamentally reshaping logistics real estate demand patterns. Online retail penetration accelerated dramatically during and after the pandemic, creating permanent structural changes in consumer behavior. This digital transformation requires sophisticated fulfillment infrastructure positioned near major ports like Santos to optimize last-mile delivery economics.

Modern e-commerce operations demand Class A warehouse facilities with specific characteristics:

- High ceiling clearances (12+ meters) for automated storage systems

- Heavy floor loading capacity (6+ tonnes per square meter)

- Cross-docking capabilities with multiple loading docks

- Advanced fire suppression and security systems

- Energy-efficient design with LEED or equivalent certifications

- Strategic proximity to port terminals and highway networks

The scarcity of existing facilities meeting these specifications has created record-low vacancy rates in the Santos logistics corridor, with prime assets commanding premium rents and delivering exceptional returns to developers and investors.

Supply Chain Re-Shoring and Nearshoring Trends

Global supply chain disruptions over the past several years have accelerated a fundamental reassessment of manufacturing and distribution strategies. Companies are increasingly prioritizing supply chain resilience over pure cost optimization, leading to significant re-shoring and nearshoring initiatives that benefit Latin American logistics hubs.

Brazil’s position as South America’s largest economy and manufacturing base makes Santos the natural gateway for these reconfigured supply chains. Multinational corporations establishing or expanding Brazilian operations require modern warehouse facilities to support:

- Regional distribution centers serving the São Paulo metropolitan area (22+ million people)

- Manufacturing support facilities for automotive, electronics, and consumer goods sectors

- Agricultural export consolidation for Brazil’s massive agribusiness industry

- Pharmaceutical and healthcare logistics requiring temperature-controlled environments

The Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors directly reflects these structural shifts in global trade patterns.

Contract Logistics Expansion

The sophistication of modern supply chains has driven rapid growth in contract logistics—third-party providers offering comprehensive warehousing, distribution, and value-added services. DP World’s recent expansion exemplifies this trend: the company now operates nearly 100,000 square meters (1.1 million square feet) of contract logistics capacity across Brazil.[1]

In February 2026, DP World signed a new contract logistics agreement with Suzano, establishing a dedicated warehouse facility with inbound handling capacity of 152 tons per day and outbound distribution capacity of 128 tons per day to support approximately 19,000 bales of daily production across Rio de Janeiro, São Paulo, Minas Gerais, and Brazil’s Central-West region.[1]

This single contract demonstrates the scale of warehouse demand being generated by Brazil’s export-oriented industries. Pulp, agricultural products, and manufactured goods all require specialized logistics infrastructure that institutional investors can develop and lease to creditworthy tenants on long-term contracts.

Yield Analysis: Why 12-15% Returns Are Achievable for Institutional Investors

Return Components and Market Fundamentals

The 12-15% annual returns being achieved by institutional investors in Santos logistics developments stem from multiple complementary factors that create a compelling risk-adjusted return profile:

Income Yield (7-9%)

- Prime logistics assets command USD 6.50-8.50 per square meter monthly in triple-net lease rates

- Long-term leases (7-15 years) with creditworthy tenants provide stable cash flows

- Annual rent escalations tied to inflation (IPCA) or USD protect against currency depreciation

- Low operating expenses in triple-net structures maximize net operating income (NOI)

Capital Appreciation (5-6%)

- Supply-demand imbalances driving rental rate growth of 4-6% annually

- Cap rate compression as institutional capital discovers the asset class

- Infrastructure improvements enhancing location premium

- Currency appreciation potential as Brazilian economy stabilizes

Development Profit (Build-to-Core Strategy)

- Development margins of 15-20% on successful projects

- Pre-leasing to anchor tenants before construction completion

- Institutional buyers acquiring stabilized assets at premium valuations

- Recycling capital into new development projects

Comparative Analysis: Santos vs. Other Brazilian Markets

| Market | Prime Rent (USD/sqm/month) | Vacancy Rate | Cap Rate | Infrastructure Quality |

|---|---|---|---|---|

| Santos Corridor | $7.50-8.50 | 2-4% | 8.5-9.5% | Excellent |

| São Paulo (Interior) | $6.00-7.00 | 5-7% | 9.0-10.0% | Very Good |

| Rio de Janeiro | $5.50-6.50 | 8-12% | 9.5-10.5% | Good |

| Campinas | $6.50-7.50 | 4-6% | 8.5-9.5% | Very Good |

| Curitiba | $5.00-6.00 | 6-9% | 9.5-10.5% | Good |

The Santos corridor offers the optimal combination of high rents, low vacancy, and superior infrastructure connectivity—factors that justify premium valuations while still delivering double-digit returns.

Risk Mitigation Through Institutional Partnerships

Institutional investors accessing the Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors typically employ sophisticated risk mitigation strategies:

✅ Pre-leasing requirements: Securing anchor tenants for 60-80% of space before construction ✅ Credit enhancement: Targeting multinational corporations and investment-grade Brazilian companies ✅ Currency hedging: Structuring USD-denominated leases or implementing FX hedges ✅ Development partnerships: Collaborating with experienced local developers who understand regulatory environments ✅ Diversification: Building portfolios across multiple assets and sub-markets ✅ Exit optionality: Maintaining relationships with institutional buyers for eventual disposition

These institutional-grade practices transform what might appear as emerging market risk into a professionally managed investment with appropriate risk-adjusted returns. For investors exploring broader opportunities, understanding best places to invest in Brazil property provides valuable context for portfolio diversification strategies.

Strategic Site Selection and Development Considerations

Proximity Analysis: The Golden Radius

Successful logistics development near Santos requires sophisticated understanding of proximity economics. The optimal development zone typically falls within a 30-50 kilometer radius of the port terminals, balancing land costs against transportation efficiency:

Inner Ring (0-15 km)

- ⚡ Advantages: Immediate port access, premium tenant demand, highest rental rates

- ⚠️ Challenges: Land scarcity, higher acquisition costs, environmental restrictions, urban congestion

Middle Ring (15-30 km)

- ⚡ Advantages: Optimal cost-benefit ratio, good highway access, available land parcels, lower congestion

- ⚠️ Challenges: Moderate competition, infrastructure dependencies

Outer Ring (30-50 km)

- ⚡ Advantages: Lower land costs, larger parcel availability, expansion potential

- ⚠️ Challenges: Transportation time penalties, tenant resistance, infrastructure gaps

The middle ring typically offers the most attractive risk-return profile for institutional development, particularly in municipalities like Cubatão, Guarujá, and portions of the Santos metropolitan region with direct highway connectivity.

Novo PAC Infrastructure Integration

Brazil’s Novo PAC (Programa de Aceleração do Crescimento) infrastructure program represents a critical catalyst for logistics development viability. The program includes substantial investments in:

- Highway improvements: Expansion and modernization of BR-116, BR-101, and Anchieta-Imigrantes corridor

- Rail connectivity: Enhancement of Santos-São Paulo rail freight capacity

- Port access roads: Dedicated truck routes reducing urban congestion

- Energy infrastructure: Reliable power supply for modern logistics facilities

- Digital connectivity: Fiber optic networks supporting warehouse automation

Developers who strategically position projects to benefit from Novo PAC improvements can achieve superior risk-adjusted returns by capitalizing on infrastructure-driven appreciation. The program’s multi-year timeline creates a predictable enhancement curve that sophisticated investors can model into their underwriting.

Environmental and Regulatory Considerations

Logistics development in the Santos region requires navigation of complex environmental and regulatory frameworks:

Environmental Licensing

- Atlantic Forest preservation requirements

- Wetland and mangrove protection zones

- Environmental impact assessments (EIA/RIMA)

- Compensation and mitigation measures

Zoning and Land Use

- Industrial zoning classifications

- Building height and coverage restrictions

- Setback requirements

- Traffic impact studies

Construction and Operations

- Fire safety and suppression systems

- Hazardous materials handling permits

- Labor and employment regulations

- Tax incentive programs (ISS, IPTU reductions)

Experienced institutional developers maintain specialized teams or partnerships to efficiently navigate these requirements, avoiding costly delays that can erode project returns. This expertise represents a significant competitive advantage in capturing the Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors.

Tenant Profile and Lease Structuring Strategies

Target Tenant Categories

Successful logistics developments in the Santos corridor typically target a diversified tenant mix across several categories:

🚢 Import/Export Consolidators

- Freight forwarders and customs brokers

- Container freight stations (CFS)

- Bonded warehouse operators

- Typical lease: 5-10 years, USD-denominated

📦 E-Commerce and Retail

- Regional distribution centers for major retailers

- Third-party logistics (3PL) providers

- Last-mile delivery hubs

- Typical lease: 7-15 years, inflation-indexed

🏭 Manufacturing Support

- Automotive parts distribution

- Electronics and consumer goods

- Industrial supplies

- Typical lease: 10-15 years, long-term commitments

🌾 Agricultural Export

- Pulp and paper consolidation (as demonstrated by the Suzano-DP World agreement)

- Grain and soybean export facilities

- Coffee and sugar warehousing

- Typical lease: 5-10 years, commodity-linked escalations

💊 Specialized Logistics

- Pharmaceutical cold chain

- Hazardous materials storage

- High-value goods security facilities

- Typical lease: 7-12 years, premium rates

Lease Structure Optimization

Institutional investors maximize returns through sophisticated lease structuring:

Triple-Net (NNN) Structures

- Tenants responsible for property taxes, insurance, and maintenance

- Landlord receives pure net income stream

- Simplified property management

- Enhanced asset liquidity for eventual sale

Currency Considerations

- USD-denominated leases for import/export tenants

- BRL leases with IPCA escalators for domestic operators

- Hybrid structures with currency adjustment mechanisms

- Natural hedging through diversified tenant base

Rent Escalations

- Annual adjustments tied to inflation indices

- Periodic market resets (every 3-5 years)

- Revenue-sharing arrangements for high-growth tenants

- Step-up provisions for phased occupancy

Tenant Improvement Allowances

- Build-to-suit specifications for anchor tenants

- Standardized shell-and-core for multi-tenant facilities

- Amortization of improvements over lease term

- Recapture provisions for early termination

These sophisticated structures protect investor returns while providing tenants with the flexibility they require in dynamic logistics markets.

Financing Structures and Capital Stack Optimization

Institutional Capital Sources

The Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors attracts diverse capital sources, each with distinct requirements and return expectations:

Pension Funds and Insurance Companies

- Seeking: 9-12% levered returns, long-term income stability

- Typical allocation: Core-plus and value-add strategies

- Investment size: USD 50-200 million per commitment

- Hold period: 7-15 years

Private Equity Real Estate Funds

- Seeking: 15-20% IRR through development and value creation

- Typical allocation: Opportunistic and value-add

- Investment size: USD 25-100 million per project

- Hold period: 3-7 years with defined exit strategies

Sovereign Wealth Funds

- Seeking: 8-11% returns with inflation protection

- Typical allocation: Core and core-plus

- Investment size: USD 100-500 million portfolio commitments

- Hold period: 10+ years, patient capital

Family Offices and High-Net-Worth

- Seeking: 12-18% returns with capital preservation

- Typical allocation: Direct investments and co-investments

- Investment size: USD 10-50 million

- Hold period: 5-10 years with flexibility

Optimal Capital Stack Construction

Successful logistics developments typically employ 60-70% leverage with the following capital stack structure:

Senior Debt (50-60% LTV)

- Brazilian development banks (BNDES) offering favorable terms

- International commercial banks for USD-denominated financing

- Interest rates: 8-12% depending on currency and tenor

- Loan term: 3-5 years construction + mini-perm

Mezzanine/Preferred Equity (10-15%)

- Subordinated debt or preferred equity structures

- Return expectations: 12-16%

- Provides additional leverage while maintaining senior debt covenants

- Often provided by specialized real estate credit funds

Common Equity (30-40%)

- Developer/sponsor equity: 10-15%

- Institutional co-investment: 20-30%

- Target equity returns: 18-25% IRR

- Waterfall structures with preferred returns and profit participation

This capital stack optimization allows developers to maximize returns while providing institutional investors with appropriate risk-adjusted profiles across the capital structure.

Market Outlook and Growth Projections Through 2028

Capacity Expansion Timeline

The phased expansion of Santos port capacity creates a predictable pipeline of warehouse demand:

2026 Milestones

- DP World capacity increase to 1.7 million TEUs

- Completion of 190-meter quay extension

- STS-10 mega-terminal auction and initial development

- Estimated new warehouse demand: 250,000-300,000 sqm

2027 Projections

- Continued infrastructure improvements under Novo PAC

- Additional freight forwarding offices opening across Brazil

- Estimated new warehouse demand: 300,000-350,000 sqm

2028 Targets

- DP World capacity reaching 2.1 million TEUs (25% increase from 2025)

- STS-10 terminal operational, adding 50% port capacity

- Estimated new warehouse demand: 400,000-500,000 sqm

This cumulative demand of 950,000-1,150,000 square meters over three years represents approximately USD 950 million-1.15 billion in development opportunity at current construction costs of USD 800-1,000 per square meter.

Competitive Landscape Evolution

The Santos logistics market is evolving from a fragmented, locally-dominated landscape toward institutional-grade, professionally-managed assets:

Traditional Players

- Local developers with land banks and political relationships

- Family-owned logistics companies expanding into real estate

- Typically smaller-scale projects (10,000-30,000 sqm)

Institutional Entrants

- Global logistics REITs (Prologis, GLP, Blackstone)

- Brazilian pension funds and insurance companies

- International private equity real estate funds

- Typically larger-scale projects (50,000-150,000 sqm)

The professionalization of the market benefits sophisticated investors who can deliver institutional-quality product with superior specifications, tenant services, and property management. This quality differentiation commands premium rents and attracts creditworthy tenants seeking long-term facilities.

Broader Brazilian Real Estate Context

While the Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors represents exceptional opportunity, investors should consider portfolio diversification across Brazilian real estate sectors. The broader real estate market transformation occurring throughout Brazil creates complementary investment opportunities.

Brazil’s port sector overall is projected to attract nearly USD 7.2 billion in investments by 2026, including multiple port concessions and infrastructure upgrades beyond Santos alone.[6] This national commitment to logistics infrastructure enhancement creates a rising tide that benefits well-positioned institutional investors across multiple markets.

Risk Factors and Mitigation Strategies

Macroeconomic Considerations

Currency Volatility

- 🎯 Mitigation: USD-denominated leases, currency hedging, natural hedges through export-oriented tenants

- 📊 Impact: Can affect returns by ±3-5% annually

Interest Rate Fluctuations

- 🎯 Mitigation: Fixed-rate financing, interest rate swaps, conservative underwriting assumptions

- 📊 Impact: Can affect development feasibility and exit cap rates

Political and Regulatory Changes

- 🎯 Mitigation: Diversification across administrations, engagement with industry associations, flexible project timelines

- 📊 Impact: Can delay projects or alter tax treatment

Operational and Market Risks

Construction Cost Escalation

- 🎯 Mitigation: Fixed-price contracts with reputable contractors, contingency reserves (10-15%), phased development approach

- 📊 Impact: Can compress development margins by 2-5%

Lease-Up Risk

- 🎯 Mitigation: Pre-leasing requirements (60-80%), relationships with tenant brokers, flexible space configurations

- 📊 Impact: Can delay stabilization by 6-18 months

Competition from New Supply

- 🎯 Mitigation: Superior locations, institutional-quality specifications, long-term tenant relationships

- 📊 Impact: Can pressure rental rates by 5-10% in oversupplied sub-markets

Tenant Credit Risk

- 🎯 Mitigation: Credit analysis, security deposits, diversified tenant base, parent company guarantees

- 📊 Impact: Can affect NOI by 2-4% through defaults or concessions

Environmental and Climate Considerations

The Santos region’s coastal location requires consideration of long-term climate risks:

- Sea level rise: Site selection above projected flood zones

- Extreme weather: Enhanced building standards for wind and precipitation

- Sustainability requirements: LEED or equivalent certifications increasingly demanded by tenants

- Carbon footprint: Energy-efficient design, renewable energy integration, EV charging infrastructure

Forward-thinking developers who proactively address these considerations position their assets for long-term value retention and tenant demand.

Actionable Implementation Roadmap for Institutional Investors

Phase 1: Market Entry and Due Diligence (Months 1-3)

Strategic Planning

- Engage local advisory teams with Santos market expertise

- Conduct comprehensive market study and demand analysis

- Identify target sub-markets and site selection criteria

- Establish legal entities and tax structures

Partnership Development

- Evaluate potential local development partners

- Assess track records and project execution capabilities

- Structure joint venture or co-investment agreements

- Define governance and decision-making processes

Initial Site Identification

- Review available land parcels meeting location criteria

- Conduct preliminary environmental assessments

- Evaluate infrastructure connectivity and Novo PAC alignment

- Analyze zoning and entitlement feasibility

Phase 2: Site Acquisition and Entitlements (Months 4-9)

Land Acquisition

- Negotiate purchase agreements with contingencies

- Conduct comprehensive due diligence (title, environmental, physical)

- Secure financing commitments for land acquisition

- Close on priority sites meeting investment criteria

Entitlement Process

- Initiate environmental licensing procedures

- Obtain zoning approvals and building permits

- Conduct traffic and infrastructure studies

- Engage with local authorities and community stakeholders

Tenant Pre-Leasing

- Launch marketing campaign to target tenants

- Negotiate letters of intent with anchor tenants

- Finalize lease terms and tenant improvement specifications

- Achieve 60-80% pre-leasing threshold for construction commencement

Phase 3: Development and Construction (Months 10-24)

Construction Financing

- Close on senior debt and mezzanine financing

- Draw equity capital according to development pro forma

- Establish project management and reporting systems

- Implement risk management and insurance programs

Project Execution

- Select general contractor through competitive bidding

- Monitor construction progress and quality control

- Manage tenant improvement build-outs

- Coordinate infrastructure connections and utilities

Ongoing Leasing

- Continue marketing to achieve 100% occupancy

- Negotiate additional leases for remaining space

- Finalize tenant move-in schedules

- Establish property management infrastructure

Phase 4: Stabilization and Asset Management (Months 25-36+)

Operational Excellence

- Implement institutional-grade property management

- Optimize operating expenses and service contracts

- Maintain high tenant satisfaction and retention

- Execute lease renewals and expansions

Value Enhancement

- Monitor market conditions for rental rate growth

- Implement sustainability improvements and certifications

- Expand or redevelop sites with additional phases

- Maintain relationships with potential acquirers

Exit Strategy Execution

- Engage investment sales advisors at optimal timing

- Market stabilized asset to institutional buyers

- Negotiate sale at attractive cap rate (typically 8.0-9.0%)

- Recycle capital into new development opportunities

This systematic approach allows institutional investors to successfully capture the Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors while managing risks through professional execution.

Conclusion

The Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors represents a compelling convergence of structural growth drivers, infrastructure investment, and supply-demand fundamentals that create exceptional opportunities for sophisticated capital. With the port handling record cargo volumes, undergoing multi-billion-dollar capacity expansions, and benefiting from e-commerce growth and supply chain re-shoring trends, the demand for modern Class A warehouse facilities has never been stronger.

The 12-15% annual returns being achieved by institutional investors reflect not speculative exuberance but rather fundamental economics: record-low vacancy rates, strong rental growth, creditworthy tenants on long-term leases, and infrastructure improvements that enhance location premiums. The phased expansion timeline—from 1.3 million TEUs in 2025 to 2.1 million TEUs by 2028, with the transformational STS-10 mega-terminal adding 50% additional capacity—creates a predictable pipeline of warehouse demand totaling nearly 1 million square meters over the next three years.

Success in this market requires more than capital—it demands sophisticated site selection aligned with Novo PAC infrastructure improvements, institutional-quality development execution, strategic tenant relationships, and professional asset management. Investors who partner with experienced local developers, implement rigorous risk mitigation strategies, and maintain patient capital with 5-10 year hold periods are positioned to achieve superior risk-adjusted returns.

Next Steps for Institutional Investors

✅ Conduct comprehensive market research on Santos logistics fundamentals and competitive landscape

✅ Engage specialized advisors with deep local market knowledge and development track records

✅ Identify strategic partners for joint venture or co-investment structures

✅ Establish legal and tax structures optimized for Brazilian real estate investment

✅ Begin site identification in the optimal 15-30 kilometer radius from port terminals

✅ Develop relationships with target tenants and leasing brokers

✅ Structure financing with appropriate leverage and currency considerations

The window of opportunity to capitalize on the Port of Santos Logistics Boom: Warehousing Developments Yielding 12-15% Returns for 2026 Institutional Investors is open now, but competition is intensifying as global institutional capital discovers this compelling market. Investors who move decisively with professional execution will secure the best sites, attract the strongest tenants, and achieve the exceptional returns that this transformational logistics expansion enables.

For investors seeking to diversify across Brazilian real estate opportunities, exploring comprehensive investment strategies and understanding market dynamics in emerging regions provides valuable context for building resilient portfolios positioned for long-term growth.

References

[1] Dp World Grows Brazil Contract Logistics Footprint With Suzano Warehouse Deal – https://www.globenewswire.com/news-release/2026/02/24/3243788/0/en/DP-World-Grows-Brazil-Contract-Logistics-Footprint-with-Suzano-Warehouse-Deal.html

[2] Building Future Trade Santos How Dp World Expanding Purpose – https://www.3blmedia.com/news/building-future-trade-santos-how-dp-world-expanding-purpose

[3] Dpw Invests Over 1 Billion Reais To Expand Santos Terminal By 25 Percent – https://www.dpworld.com/en/news/usa/dpw-invests-over-1-billion-reais-to-expand-santos-terminal-by-25-percent

[4] Port Auctions To Strengthen Infrastructure At Santos And Sao Sebastiao – https://www.czapp.com/analyst-insights/port-auctions-to-strengthen-infrastructure-at-santos-and-sao-sebastiao/

[5] Port Of Santos Posts Record January Throughput To Open 2026 – https://datamarnews.com/noticias/port-of-santos-posts-record-january-throughput-to-open-2026/

[6] Brazil Projects New Logistics Concessions By 2026 – https://brazilstockguide.com/insights/brazil-projects-new-logistics-concessions-by-2026/