Brazil’s construction sector stands at a crossroads in 2026. While financial markets anticipate a decline in the country’s benchmark Selic rate from its current 15% to approximately 12.25% by year-end, developers face an uncomfortable reality: real interest rates and construction viability remain fundamentally disconnected from project profitability in high-cost regions. This paradox—where nominal rate improvements fail to unlock development potential—reveals deeper structural challenges that gradual monetary easing simply cannot address.

The issue extends beyond simple arithmetic. Brazil’s Selic benchmark rate stands at 15%—the highest level in nearly two decades since June 2025—and has been maintained for four consecutive monetary policy committee meetings[1]. Yet even as expectations build for rate reductions, the construction industry confronts a sobering truth: real interest rates and construction viability: why 2026’s gradual rate decline won’t solve Brazil’s high-cost development problem centers on structural cost barriers that persist regardless of monetary policy adjustments.

Key Takeaways

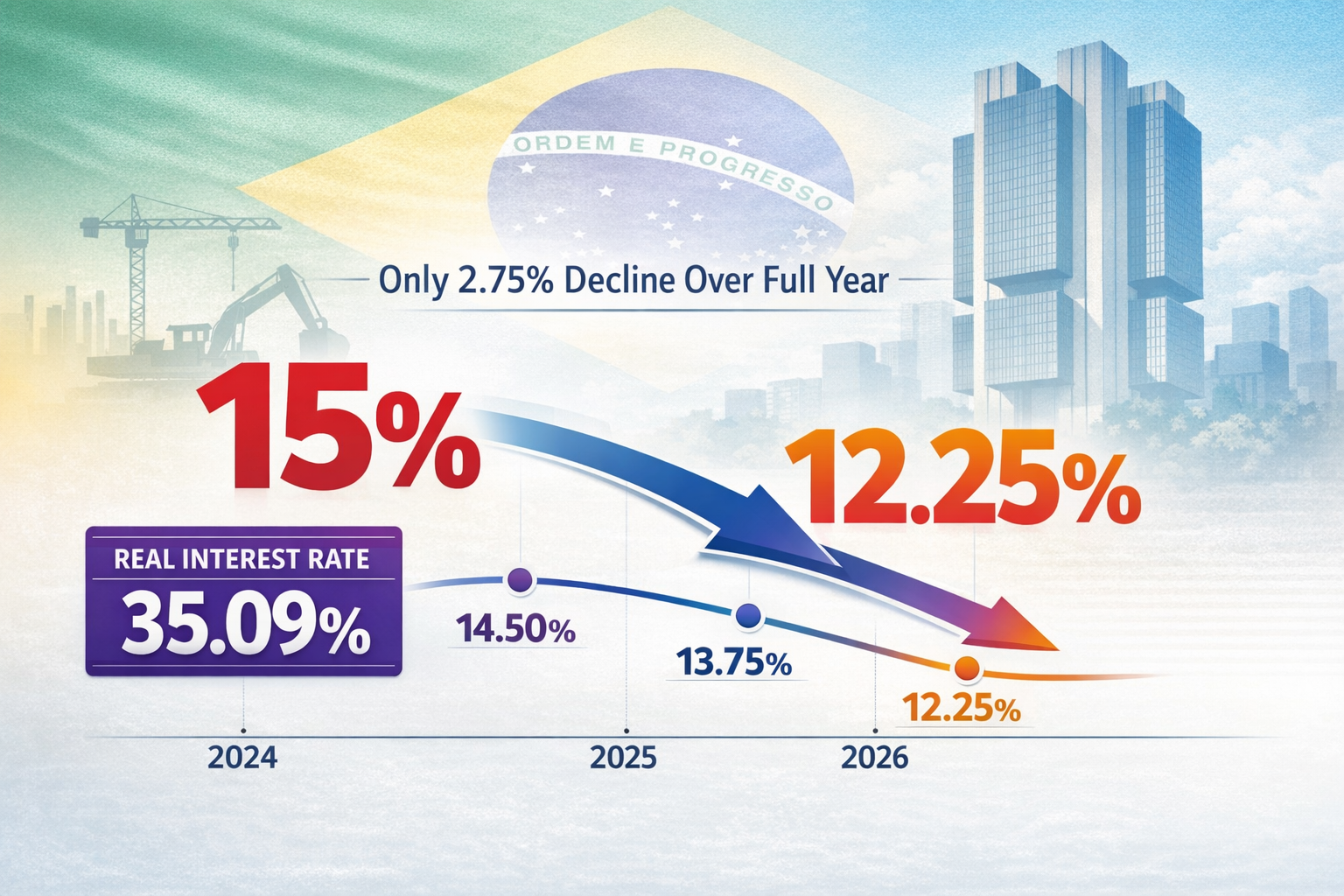

- 🏗️ Brazil’s Selic rate at 15% represents the highest level since 2006, but the projected decline to 12.25% by end of 2026 offers only marginal relief for construction financing

- 📊 Real interest rates reached 35.09% in 2024, creating a structural cost barrier that gradual rate cuts cannot overcome for high-cost development projects

- 💰 Construction growth projections for 2026 remain moderate at 1.7-3.3%, heavily dependent on government programs rather than market-driven demand

- 🏘️ Elevated property inventory from 2025 continues to weigh on new launches, particularly in segments requiring financing accessibility

- ⚠️ The 2.75-point rate reduction expected in 2026 expands buyer purchasing power by only 22-27%—insufficient to activate demand in premium development segments

Understanding Brazil’s Interest Rate Environment in 2026

The Current State of Monetary Policy

Brazil’s central bank has maintained an aggressive stance on interest rates throughout 2025 and into 2026. The Selic benchmark rate stands at 15%—the highest level since 2006—reflecting persistent inflationary pressures and macroeconomic instability[1][3]. This elevated rate environment has created significant headwinds for construction financing, as the cost of capital directly impacts project feasibility calculations.

The financial market expects the Selic rate to decline to 12.25% by the end of 2026[2], representing a 2.75 percentage point reduction over the full year[3]. While this trajectory suggests improvement, industry experts characterize these rate cuts as “very gradual” and insufficient to unlock strong recovery in construction activity[1].

Real vs. Nominal Interest Rates: The Critical Distinction

The distinction between nominal and real interest rates proves crucial for understanding construction viability. According to World Bank data, real interest rates in Brazil reached 35.09% in 2024[5], demonstrating the severe structural cost of capital that developers face even as nominal rates begin their gradual descent.

Real interest rates—which account for inflation—provide a more accurate picture of actual borrowing costs. One economist noted that “interest rates will come down, but they will remain extremely high”[1], highlighting the persistent gap between monetary policy adjustments and meaningful relief for capital-intensive construction projects.

For developers evaluating the best places to invest in Brazil property, this distinction between nominal and real rates becomes a critical factor in project selection and market positioning.

Why Real Interest Rates and Construction Viability Remain Disconnected in 2026

The Mathematics of Marginal Rate Decline

A 1% change in interest rates shifts mortgage affordability by roughly 8-10%[3]. Based on this relationship, the projected 2.75-point decline from 15% to 12.25% could theoretically expand buyer purchasing power by approximately 22-27%[3]. However, this mathematical relationship fails to account for several constraining factors:

- High transaction costs that absorb much of the affordability gain

- Elevated household debt levels that limit borrowing capacity

- Limited supply that prevents price adjustments despite financing constraints

- Cash buyer dominance in premium segments that insulates pricing from financing conditions

High interest rates continue putting “significant downward pressure on transaction volumes,” though prices keep rising due to limited supply and demand from cash buyers[3]. This creates a bifurcated market where financing-dependent buyers remain sidelined while cash transactions sustain price levels.

Structural Cost Barriers Beyond Financing

The construction viability challenge extends beyond financing costs to encompass broader structural issues:

| Cost Category | Impact on Viability | Sensitivity to Rate Changes |

|---|---|---|

| Land acquisition | 25-35% of total cost | Low |

| Materials & labor | 40-50% of total cost | Low |

| Financing costs | 15-25% of total cost | High |

| Regulatory compliance | 5-10% of total cost | None |

| Infrastructure gaps | Variable | None |

Even with a 2.75-point rate reduction, financing costs represent only 15-25% of total development costs. The majority of cost structure remains unaffected by monetary policy, explaining why gradual rate decline fails to restore viability to previously unprofitable projects.

Government Dependency vs. Market-Driven Demand

FIESP’s construction growth projection for 2026 ranges from 1.7% to 3.3% depending on scenarios[1]. Notably, the optimistic scenario depends heavily on increased housing credit availability through government programs rather than organic market demand.

Infrastructure has been identified as “the main driver” for construction growth, supported by Novo PAC (Growth Acceleration Program) and social infrastructure funds[1]. Meanwhile, housing segments remain heavily dependent on government programs like MCMV (Minha Casa Minha Vida)[1].

This government dependency reveals a fundamental weakness: market-driven construction demand remains insufficient even with anticipated rate declines. The sector’s reliance on public programs and infrastructure spending suggests that private residential development in high-cost regions faces viability challenges that monetary policy alone cannot resolve.

Experts note that “even with lower interest rates, the impact on housing finance is not that relevant in a macroeconomic environment full of problems”[1], underscoring the limitations of rate policy as a sector recovery tool.

The Inventory Overhang and Its Impact on New Development

Elevated Stock Levels from 2025

Elevated property inventory levels carried over from 2025 are expected to weigh significantly on new project launches in 2026[1]. This inventory overhang creates a challenging environment for developers considering new projects, particularly in segments sensitive to financing conditions.

The inventory accumulation reflects several converging factors:

- 📉 Transaction volume suppression due to high financing costs

- 🏢 Speculative development launched during more optimistic periods

- 💳 Buyer financing constraints that extended sales cycles

- 🎯 Market segmentation with premium units experiencing slower absorption

For developers tracking how sales performance is transforming the real estate market in Florianópolis, the inventory challenge requires strategic repositioning and careful market timing.

Segment-Specific Vulnerability

Not all construction segments face equal vulnerability to the inventory overhang. Financing-dependent segments—particularly middle-income residential units priced between R$300,000-800,000—experience the most acute pressure. These properties require mortgage accessibility that remains constrained despite gradual rate declines.

In contrast, luxury segments targeting cash buyers and government-supported affordable housing continue showing relative resilience. This bifurcation creates strategic implications for developers choosing which segments to pursue in 2026.

Price Forecasts and Market Dynamics for 2026

Property prices in Brazil are expected to increase 6-10% in nominal terms over 2026, with a point estimate around 7.5%[3]. This continued price appreciation despite financing constraints reflects several dynamics:

- 🏗️ Supply constraints from reduced new launches

- 💰 Cash buyer demand insulating premium segments

- 🌍 Foreign investment in select coastal markets

- 📍 Location premiums in high-demand urban centers

However, these price increases occur alongside stagnant transaction volumes, creating a market characterized by price rigidity rather than robust demand. Developers must navigate this environment carefully, as nominal price appreciation may mask underlying demand weakness.

Understanding appreciation potential for those buying off-plan becomes increasingly important in this context, as development timing and market positioning determine ultimate profitability.

Strategic Responses: How Developers Can Navigate the Financing Gap

Focus on Cash Buyer Segments

Given the persistent constraints on financing-dependent demand, successful developers in 2026 increasingly target cash buyer segments. This strategic pivot includes:

- 🏖️ Vacation property development in coastal markets like Florianópolis

- 🏢 Investment-grade units designed for rental income generation

- 💎 Luxury residential targeting high-net-worth individuals

- 🌐 International buyer marketing to diversify demand sources

Markets like the growing Ingleses region in Florianópolis offer particular opportunities for cash buyer-focused development, combining quality of life amenities with appreciation potential.

Alignment with Government Programs

Developers pursuing volume-oriented strategies increasingly align projects with government housing programs. The MCMV program and related initiatives provide financing support that private markets cannot match under current rate conditions.

This alignment requires:

- 📋 Compliance with program specifications for unit size, pricing, and location

- 🤝 Partnership with government agencies to secure program participation

- 💡 Design optimization to meet program requirements while maintaining margins

- 📊 Volume planning to achieve economies of scale

While government-aligned projects offer lower margins than luxury development, they provide volume certainty and reduced market risk in uncertain financing environments.

Cost Optimization and Efficiency Gains

With financing costs remaining elevated and material costs continuing to rise, operational efficiency becomes paramount. Leading developers implement:

- 🏭 Industrialized construction methods to reduce labor costs

- 📦 Bulk purchasing agreements for materials

- ⚡ Project timeline compression to minimize financing duration

- 🔧 Value engineering to maintain quality while controlling costs

These efficiency measures cannot fully offset high financing costs, but they improve project viability at the margin—often making the difference between profitable and unprofitable development.

Market Timing and Phased Development

Rather than launching large projects simultaneously, sophisticated developers adopt phased development strategies that:

- 🎯 Match supply to absorption capacity in constrained markets

- 💰 Generate cash flow from early phases to fund later construction

- 📉 Reduce inventory risk by limiting unsold unit accumulation

- 🔄 Allow strategy adjustment based on evolving market conditions

Monitoring construction progress and accelerated development pace provides valuable insights into effective phasing strategies that maintain momentum while managing risk.

Regional Variations: Where Construction Remains Viable

Infrastructure-Driven Opportunities

Infrastructure development—supported by Novo PAC and social infrastructure funds—creates localized construction opportunities even in challenging financing environments. Regions benefiting from major infrastructure investments experience:

- 🚇 Transportation improvements that enhance accessibility

- 💧 Utility infrastructure that enables new development

- 🏫 Social infrastructure (schools, hospitals) that attracts residents

- 🏗️ Commercial development following infrastructure investment

Developers who position projects near infrastructure investments can capture appreciation benefits that offset financing cost pressures.

High-Growth Urban Centers

Certain Brazilian cities demonstrate resilient construction markets despite national financing constraints. These markets typically feature:

- 📈 Strong economic fundamentals supporting employment and income growth

- 🌊 Lifestyle amenities attracting domestic migration

- 🏢 Diversified economies reducing sector-specific risk

- 🎓 Educational institutions creating stable rental demand

Florianópolis exemplifies this dynamic, with strong market performance driven by quality of life, economic diversification, and demographic trends favoring coastal migration.

Studio and Compact Unit Opportunities

Studio apartments and compact units demonstrate particular resilience in high-cost financing environments. The advantages of investing in studios in Florianópolis include:

- 💵 Lower absolute prices improving financing accessibility

- 🎓 Student and young professional demand providing stable absorption

- 💰 Investment buyer appeal for rental income generation

- 📊 Higher yields relative to larger units

These units occupy a market sweet spot where financing remains accessible despite elevated rates, while investment fundamentals support cash buyer demand.

The Macroeconomic Context: Why Problems Persist Beyond Interest Rates

Household Indebtedness Trends

Household indebtedness continues to rise in Brazil, creating a structural constraint on mortgage demand that persists regardless of interest rate levels[1]. High existing debt burdens limit households’ capacity to take on additional mortgage obligations, even as rates decline.

This indebtedness reflects:

- 💳 Consumer credit expansion during previous lower-rate periods

- 📱 Buy-now-pay-later adoption increasing short-term obligations

- 🏥 Healthcare and education costs consuming disposable income

- ⚡ Utility and essential expense inflation reducing debt service capacity

The combination of high debt levels and elevated interest rates creates a double constraint on housing demand that gradual rate decline cannot quickly resolve.

Inflation Persistence and Real Income Pressure

While nominal interest rates may decline, inflation persistence limits the real benefit to borrowers and maintains pressure on household budgets. Real income growth remains constrained, reducing the pool of qualified mortgage borrowers regardless of interest rate trajectory.

Regulatory and Bureaucratic Costs

Brazil’s construction sector faces significant regulatory and bureaucratic costs that remain unaffected by monetary policy:

- 📋 Permitting delays extending project timelines

- 💼 Compliance requirements adding administrative overhead

- 🏛️ Environmental regulations increasing approval complexity

- 💰 Tax burdens on construction materials and transactions

These structural costs compound financing pressures, making marginal rate improvements insufficient to restore viability to previously unprofitable projects.

Looking Ahead: What Developers Should Expect Beyond 2026

Limited Near-Term Relief

The evidence suggests that real interest rates and construction viability will remain disconnected beyond 2026’s gradual rate decline. Structural factors—including household debt, regulatory costs, and material price inflation—will continue constraining development profitability in high-cost regions.

Developers should plan for:

- 📊 Continued moderate growth in the 2-4% range annually

- 🏛️ Persistent government program dependency for volume segments

- 💰 Cash buyer focus as the most viable private market strategy

- 🎯 Selective market entry based on location-specific fundamentals

Potential Structural Reforms

Meaningful improvement in construction viability requires structural reforms beyond monetary policy, including:

- 🏗️ Regulatory streamlining to reduce permitting timelines and costs

- 💼 Tax reform to lower transaction and construction material burdens

- 🏘️ Land use policy improvements to increase developable supply

- 🏦 Housing finance innovation to improve mortgage accessibility

Until such reforms materialize, developers must navigate the challenging environment with strategic positioning and operational excellence rather than relying on macroeconomic tailwinds.

Technology and Innovation as Differentiators

Forward-looking developers increasingly leverage technology and construction innovation to maintain viability despite unfavorable financing conditions:

- 🏭 Modular construction reducing labor costs and timelines

- 📱 Digital marketing improving sales efficiency and reducing carrying costs

- 🤖 Project management software optimizing resource allocation

- 🌱 Sustainable building practices accessing green financing and premium pricing

These innovations provide competitive advantages that compound over time, creating differentiation in commoditized markets.

Conclusion

Real interest rates and construction viability: why 2026’s gradual rate decline won’t solve Brazil’s high-cost development problem represents more than a temporary market challenge—it reflects fundamental structural disconnects between monetary policy and construction economics. While the expected decline from 15% to 12.25% in the Selic rate provides marginal relief, it fails to address the deeper cost barriers, household debt constraints, and regulatory burdens that prevent viable development in many high-cost regions.

The construction sector’s projected growth of 1.7-3.3% in 2026 remains heavily dependent on government programs and infrastructure spending rather than market-driven residential demand[1]. With real interest rates having reached 35.09% in 2024[5] and remaining “extremely high” despite nominal rate improvements[1], developers face a challenging environment requiring strategic adaptation rather than passive reliance on improving financing conditions.

Actionable Next Steps for Developers

✅ Segment strategically: Focus on cash buyer segments, government-aligned affordable housing, or infrastructure-adjacent opportunities rather than financing-dependent middle-market residential

✅ Optimize operations: Implement industrialized construction methods, value engineering, and timeline compression to offset persistent financing cost pressures

✅ Phase development: Adopt phased project launches that match supply to realistic absorption capacity while generating cash flow to fund subsequent phases

✅ Target resilient markets: Concentrate efforts in high-growth urban centers with strong economic fundamentals and lifestyle amenities that support premium pricing

✅ Leverage technology: Invest in construction innovation, digital marketing, and project management tools that provide competitive advantages in challenging markets

✅ Monitor policy developments: Track government program evolution and infrastructure investment plans to position projects for maximum program alignment and location benefits

The path forward requires acknowledging that gradual interest rate decline alone cannot restore construction viability in high-cost development contexts. Success in 2026 and beyond depends on strategic positioning, operational excellence, and realistic assessment of structural constraints that persist regardless of monetary policy adjustments. Developers who adapt their strategies to this reality—rather than waiting for financing conditions that may never materialize—will capture the opportunities that exist within Brazil’s challenging but dynamic construction landscape.

References

[1] Brazils Construction Sector 2026 Housing Programs Support Rates High Risks Persist – https://www.fastmarkets.com/insights/brazils-construction-sector-2026-housing-programs-support-rates-high-risks-persist/

[2] Condicoes Macroeconomicas Investimentos Infraestrutura Brasil 2025 2026 – https://news.griinstitute.org/en/infrastructure/condicoes-macroeconomicas-investimentos-infraestrutura-brasil-2025-2026

[3] Brazil Price Forecasts – https://thelatinvestor.com/blogs/news/brazil-price-forecasts

[4] Brazil Economic Outlook – https://www.deloitte.com/us/en/insights/topics/economy/americas/brazil-economic-outlook.html

[5] Real Interest Rate Percent Wb Data – https://tradingeconomics.com/brazil/real-interest-rate-percent-wb-data.html

[6] 121025 Interview Strong Brazil Construction Market Key For Rebar Sales To Continue Cbic President – https://www.spglobal.com/energy/en/news-research/latest-news/metals/121025-interview-strong-brazil-construction-market-key-for-rebar-sales-to-continue-cbic-president

[7] Bra Real Interest Rate – https://statbase.org/data/bra-real-interest-rate/