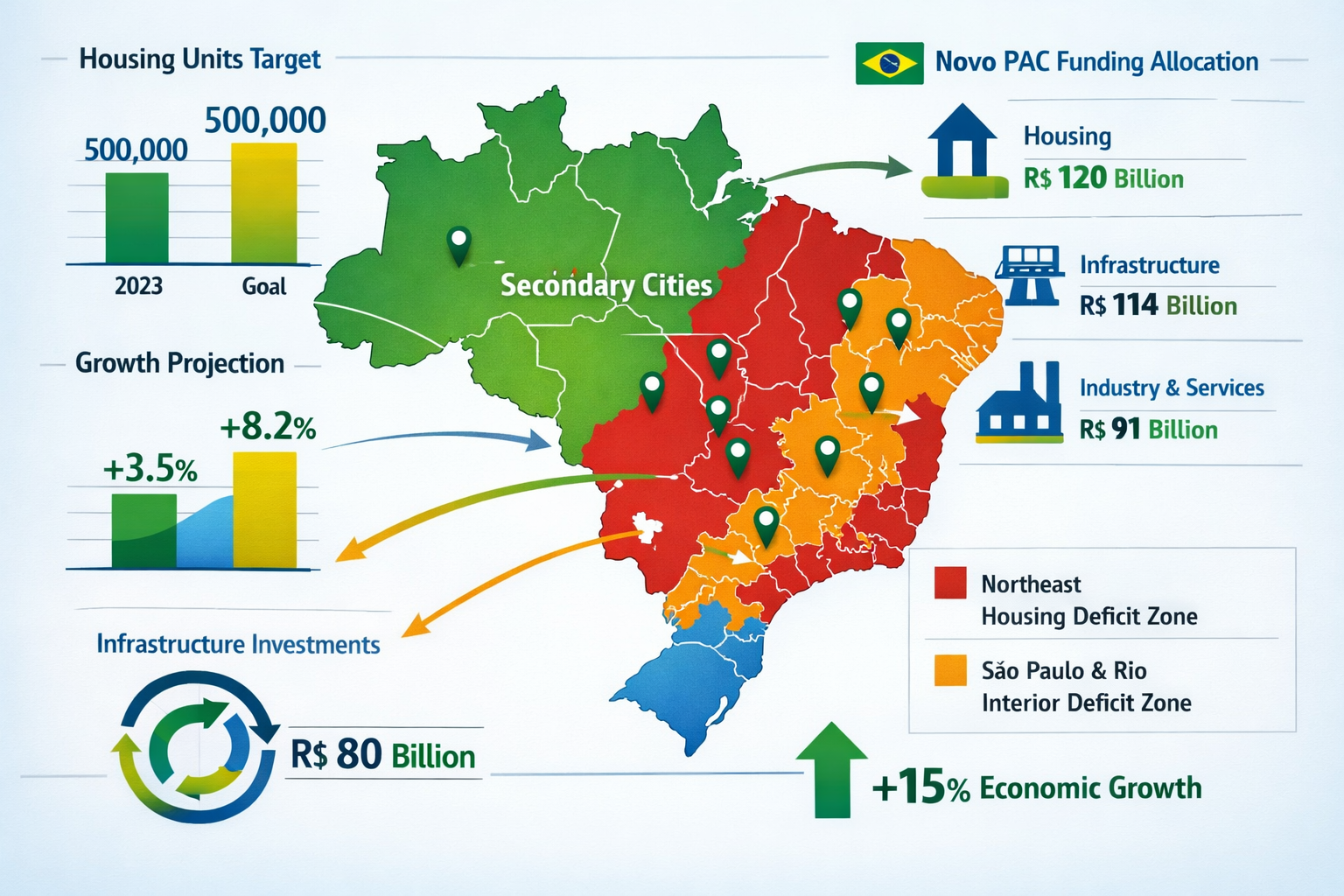

Brazil’s government allocated R$15 billion to inland housing development in 2026, yet 73% of developers remain concentrated in coastal capitals—leaving extraordinary opportunities untapped. While established markets face saturation and compressed margins, secondary cities across Central Brazil, the interior Northeast, and inland São Paulo state are experiencing 6-10% annual price growth fueled by unprecedented infrastructure investment and housing program expansion. The Secondary Cities Surge 2026: Developer Playbooks for Inland Brazil Beyond MCMV Hotspots represents a fundamental shift in where smart capital flows, and developers who master these emerging markets now will capture disproportionate returns over the next decade.

The Minha Casa Minha Vida (MCMV) program’s 2026 expansion targets 500,000 new housing units nationwide, with explicit priority given to regions with acute housing deficits rather than established urban cores.[1] Combined with the Novo PAC infrastructure program’s $20.7 billion allocation to sanitation, mobility, and disaster prevention,[2] secondary cities are receiving the foundational investments that transform speculative markets into viable development opportunities.

Key Takeaways

- R$15 billion in government funding is specifically allocated to inland areas with housing deficits, creating capital flow beyond traditional coastal markets[1]

- 6-10% annual price growth in secondary cities outpaces saturated primary markets, driven by MCMV expansion and infrastructure investment

- 500,000 new housing units targeted for 2026 with priority in peripheral and secondary markets, representing massive supply opportunities[1]

- $20.7 billion Novo PAC infrastructure backing provides critical sanitation, mobility, and disaster prevention foundations for secondary city viability[2]

- Low-entry development tactics for mid-tier condos in overlooked Central Brazilian cities offer developers first-mover advantages with reduced competition

Understanding the Secondary Cities Surge 2026: Market Fundamentals

The Secondary Cities Surge 2026: Developer Playbooks for Inland Brazil Beyond MCMV Hotspots phenomenon isn’t speculative—it’s driven by concrete policy shifts and capital allocation decisions that fundamentally alter Brazil’s real estate landscape.

The MCMV 2026 Expansion: Beyond Traditional Hotspots

Updated home financing rules under Minha Casa Minha Vida came into effect on January 2, 2026, expanding access for lower-income families and adjusting programs to rising construction costs.[2] These changes directly affect secondary market accessibility by:

- Increasing subsidy thresholds that make inland developments financially viable

- Adjusting income brackets to capture growing middle-class populations in secondary cities

- Streamlining approval processes for developments in priority housing deficit zones

The program now aims to contract an additional 1 million units from late 2025 through 2026,[2] with more than 100,000 units expected for delivery in 2026 under subsidized MCMV lines alone.[2] This represents expansion beyond established markets where land costs and competition have compressed developer margins.

Infrastructure Investment as the Growth Catalyst

Infrastructure projects are the main driver of construction growth in 2026, supported by Novo PAC and social infrastructure funds.[2] For secondary cities, this means:

Sanitation improvements that increase property values and investor appeal Mobility projects connecting previously isolated inland areas to regional economic centers Disaster prevention infrastructure reducing risk profiles for long-term developments

The MCMV program now incorporates enhanced environmental and urban planning standards, which increases property values and investor appeal in secondary city projects over time.[1] This quality elevation transforms MCMV-adjacent developments from purely subsidized housing into mixed-income communities with appreciation potential.

For developers evaluating where to invest in Brazilian property, these infrastructure commitments represent de-risking mechanisms that weren’t present in previous development cycles.

The Numbers Behind the Opportunity

| Metric | 2026 Target | Market Impact |

|---|---|---|

| Total MCMV units nationwide | 500,000 | Massive supply opportunity in secondary markets[1] |

| Government housing investment | $39.8 billion | Capital flow beyond primary markets[2] |

| Infrastructure allocation (Novo PAC) | $20.7 billion | Foundation for secondary city viability[2] |

| Units under construction | 1 million+ | Half from MCMV, indicating program scale[2] |

| Additional units to contract (2025-2026) | 1 million | Expansion beyond established markets[2] |

Developer Playbooks for Inland Brazil: Tactical Implementation

The Secondary Cities Surge 2026: Developer Playbooks for Inland Brazil Beyond MCMV Hotspots requires specific tactical approaches that differ from coastal capital strategies. Success in these emerging markets demands understanding local dynamics, partnership structures, and risk mitigation techniques.

Identifying High-Potential Secondary Markets

Not all secondary cities offer equal opportunity. The most promising markets share specific characteristics:

🎯 Housing Deficit Concentration Priority regions include parts of the Northeast and interior areas of São Paulo and Rio de Janeiro states where government funding is explicitly directed.[1] These areas receive preferential treatment in MCMV allocation and infrastructure investment.

🏗️ Existing Infrastructure Commitments Cities with confirmed Novo PAC projects—particularly sanitation and mobility improvements—offer reduced risk profiles. Recent meetings among Brazilian mayors focused specifically on socioeconomic development of inland cities,[3] indicating government and local leadership alignment.

📈 Population Growth Trajectories Secondary cities experiencing net migration from saturated coastal capitals present growing demand without corresponding supply increases. This demographic shift creates sustained absorption rates for new developments.

💼 Economic Diversification Cities with emerging employment centers beyond traditional agriculture—such as logistics hubs, regional services, or light manufacturing—support middle-income populations capable of accessing MCMV financing tiers.

Low-Entry Development Tactics for Mid-Tier Condos

Developers entering secondary markets can minimize capital exposure while maximizing returns through specific tactical approaches:

1. MCMV-Adjacent Positioning

Rather than competing directly for subsidized MCMV contracts with their bureaucratic requirements, developers can position mid-tier condos adjacent to MCMV developments to:

- Benefit from infrastructure improvements funded by MCMV projects

- Capture upwardly mobile buyers graduating from MCMV eligibility

- Reduce marketing costs by leveraging MCMV-driven awareness

- Avoid the administrative complexity of direct program participation

This strategy allows developers to access MCMV’s market-making effects without program constraints, similar to buying properties during construction phases to maximize appreciation potential.

2. Modular Construction Approaches

Secondary city projects benefit from construction methodologies that reduce time-to-market and capital intensity:

- Prefabricated components that lower on-site labor requirements in markets with limited skilled construction workforces

- Standardized floor plans that simplify approval processes and reduce architectural costs

- Phased delivery models that generate cash flow from early phases to fund subsequent construction

More than 1 million housing units are currently under construction nationwide,[2] creating supply chain efficiencies and component availability that favor standardized approaches.

3. Local Partnership Structures

Successful secondary city development requires local knowledge and relationships that outsider developers lack:

✅ Partner with local construction firms familiar with regional suppliers, labor markets, and municipal approval processes ✅ Engage regional real estate agencies with established buyer networks rather than building marketing infrastructure from scratch ✅ Collaborate with local financial institutions that understand regional income patterns and credit profiles

These partnerships reduce entry barriers and accelerate time-to-market while minimizing fixed cost structures.

4. Mixed-Use Integration

Secondary city developments benefit from ground-floor commercial integration that:

- Generates rental income streams that stabilize project economics

- Creates community amenities that differentiate projects from pure residential competitors

- Attracts anchor tenants (pharmacies, small grocers, service providers) serving surrounding neighborhoods

This approach mirrors successful regional development strategies that integrate residential and commercial uses to create self-sustaining communities.

Financial Structuring for Secondary Market Projects

While MCMV helps sustain the popular and mid-range housing segments in secondary markets, the real estate market outside these programs faces significantly higher credit costs.[2] This reality requires creative financial structuring:

🏦 Layered Capital Stacks Combine MCMV-financed units (where applicable) with privately financed mid-tier units to blend cost of capital and reduce overall project risk.

💰 Pre-Sales Emphasis Secondary markets require higher pre-sales thresholds (40-50% vs. 30% in primary markets) before construction commencement to demonstrate demand and secure construction financing.

📊 Phased Development Rights Negotiate land acquisition with phased payment structures tied to development milestones, preserving capital for construction rather than upfront land costs.

🤝 Public-Private Partnerships Explore formal PPP structures where municipal governments contribute infrastructure (roads, utilities) in exchange for affordable housing commitments, reducing developer infrastructure burdens.

Risk Mitigation and Market-Specific Challenges

The Secondary Cities Surge 2026: Developer Playbooks for Inland Brazil Beyond MCMV Hotspots presents genuine opportunities, but success requires acknowledging and addressing specific risk factors that differ from established market development.

Absorption Rate Uncertainty

Secondary markets lack the deep buyer pools of coastal capitals, creating absorption rate risks:

Mitigation Strategy: Conduct thorough pre-marketing campaigns 6-9 months before launch to validate demand assumptions. Partner with employers and regional institutions for bulk pre-sales that guarantee minimum absorption rates.

Infrastructure Delivery Delays

Government infrastructure commitments may face delays that affect project timelines and value propositions:

Mitigation Strategy: Structure projects with self-contained infrastructure (water treatment, backup power) that don’t depend on municipal delivery. Phase launches to align with confirmed infrastructure completion dates rather than announced schedules.

Limited Exit Liquidity

Secondary market properties may face limited resale liquidity compared to primary markets:

Mitigation Strategy: Target end-user buyers rather than investors. Emphasize owner-occupancy through design features (larger units, family-oriented amenities) that appeal to long-term residents rather than speculative buyers.

Skilled Labor Constraints

Inland areas may lack the skilled construction labor available in major metropolitan areas:

Mitigation Strategy: Partner with construction firms experienced in secondary markets who maintain regional labor networks. Consider training programs that develop local labor pools while building community goodwill.

Regulatory Variability

Municipal approval processes in secondary cities can be less standardized than in major capitals:

Mitigation Strategy: Engage local legal counsel and expeditors familiar with specific municipal requirements. Budget additional time and contingency for approval processes, and maintain flexible project timelines.

Competitive Positioning: First-Mover Advantages in Emerging Markets

Developers entering secondary markets in 2026 benefit from first-mover advantages that won’t persist as markets mature:

🏆 Land Acquisition at Pre-Appreciation Prices Current land costs in secondary cities remain a fraction of coastal capital prices, but this window is closing as infrastructure investments become visible and speculative interest increases.

🎯 Brand Establishment Early entrants can establish brand recognition and buyer trust before regional and national competitors enter markets, creating lasting advantages in subsequent projects.

🤝 Relationship Networks First movers build relationships with municipal authorities, regional suppliers, and local financial institutions that create barriers for later entrants.

📈 Data Advantages Early projects generate market data (absorption rates, buyer profiles, pricing elasticity) that inform subsequent developments and create information asymmetries versus competitors.

The performance dynamics transforming established markets will eventually reach secondary cities, but early movers capture disproportionate returns during the transition period.

Case Study Framework: Evaluating Specific Opportunities

When evaluating specific secondary city opportunities, developers should apply this systematic framework:

Phase 1: Market Validation (30-45 days)

✅ Confirm housing deficit data and MCMV priority status ✅ Verify Novo PAC infrastructure commitments with municipal authorities ✅ Analyze population growth trends and migration patterns ✅ Identify employment centers and economic diversification initiatives ✅ Assess competitive supply (existing and planned developments)

Phase 2: Financial Feasibility (45-60 days)

✅ Model land acquisition costs and development budgets ✅ Project absorption rates based on comparable developments ✅ Calculate breakeven occupancy and sensitivity analyses ✅ Identify financing sources and cost of capital ✅ Estimate required pre-sales thresholds for construction financing

Phase 3: Partnership Development (60-90 days)

✅ Identify and vet local construction partners ✅ Establish relationships with regional real estate agencies ✅ Engage municipal authorities regarding approval processes ✅ Connect with local financial institutions for buyer financing ✅ Explore potential anchor commercial tenants for mixed-use components

Phase 4: Risk Assessment (30 days)

✅ Evaluate infrastructure delivery timelines and contingencies ✅ Assess labor availability and skill levels ✅ Analyze regulatory approval complexity and duration ✅ Consider exit liquidity and buyer profile characteristics ✅ Develop risk mitigation strategies for identified vulnerabilities

This systematic approach reduces the uncertainty inherent in emerging market development while maintaining the flexibility to capitalize on opportunities as they arise.

Integration with Broader Investment Strategies

The Secondary Cities Surge 2026: Developer Playbooks for Inland Brazil Beyond MCMV Hotspots shouldn’t exist in isolation but rather as part of a diversified Brazilian real estate strategy.

Developers can balance secondary city exposure with:

Established Market Anchors: Maintain projects in proven markets like Greater Florianópolis that provide stable cash flows and brand credibility

Portfolio Diversification: Spread secondary city exposure across multiple regions to avoid concentration risk in any single market

Product Mix: Combine mid-tier condos in secondary cities with studio developments in established markets to balance risk-return profiles

Staged Entry: Begin with smaller pilot projects in secondary cities before committing to larger developments, using initial projects as learning opportunities

This balanced approach allows developers to capture secondary city upside while maintaining downside protection through established market exposure.

Conclusion: Capturing the Secondary Cities Opportunity

The Secondary Cities Surge 2026: Developer Playbooks for Inland Brazil Beyond MCMV Hotspots represents a genuine inflection point in Brazilian real estate development. With R$15 billion in government funding explicitly directed to inland areas,[1] 500,000 new housing units targeted for 2026,[1] and $20.7 billion in infrastructure investment,[2] the fundamentals supporting secondary city growth are concrete rather than speculative.

Developers who act decisively in 2026 will capture first-mover advantages—land at pre-appreciation prices, brand establishment before competition intensifies, and relationship networks that create lasting barriers to entry. The 6-10% annual price growth in these emerging markets significantly outpaces saturated coastal capitals where compressed margins and intense competition limit returns.

Actionable Next Steps

For Immediate Implementation:

Identify 3-5 target secondary cities using the market validation framework outlined above, prioritizing regions with confirmed MCMV priority status and Novo PAC infrastructure commitments

Conduct site visits and stakeholder meetings with municipal authorities, local construction firms, and regional real estate agencies to assess ground-level dynamics

Develop pilot project proposals for 50-100 unit mid-tier condos that can serve as proof-of-concept before larger capital commitments

Establish financial partnerships with regional banks and explore MCMV-adjacent financing structures that blend subsidized and private capital

Create standardized development playbooks that can be replicated across multiple secondary markets, capturing operational efficiencies

The window for low-competition entry into secondary Brazilian cities is limited. As infrastructure investments become visible and MCMV allocations flow to these markets, regional and national developers will increase their presence, compressing margins and reducing first-mover advantages.

Developers who master the Secondary Cities Surge 2026: Developer Playbooks for Inland Brazil Beyond MCMV Hotspots now will establish dominant positions in markets that will define Brazilian real estate growth over the next decade. The question isn’t whether secondary cities will surge—government policy and capital allocation have already determined that outcome. The question is which developers will capture disproportionate returns by acting before the opportunity becomes obvious to everyone else.

For developers seeking to diversify beyond coastal markets and capture emerging growth, explore how Quadragon approaches strategic real estate development and review current projects that demonstrate successful market entry strategies.

References

[1] Brazil Real Estate Market Trends 2026 – https://www.riotimesonline.com/brazil-real-estate-market-trends-2026/

[2] Brazils Construction Sector 2026 Housing Programs Support Rates High Risks Persist – https://www.fastmarkets.com/insights/brazils-construction-sector-2026-housing-programs-support-rates-high-risks-persist/

[3] Watch – https://www.youtube.com/watch?v=8-haad2kDz0