Brazil’s residential property market launched 19.3% more units in early 2026 than in the same period a year earlier — and that growth is happening even while the Selic benchmark rate sits near a restrictive 14.75% [3]. The central question for developers, investors, and homebuyers is what happens when that rate falls further. Forecasts pointing toward a Selic rate drop to 12.25% by end-2026 — and the broader story of scaling residential launches as buyer pools expand in Brazil — represent one of the most consequential shifts in Latin American real estate in years. Understanding the mechanics behind that shift, and how to position for it, is the focus of this analysis.

Key Takeaways

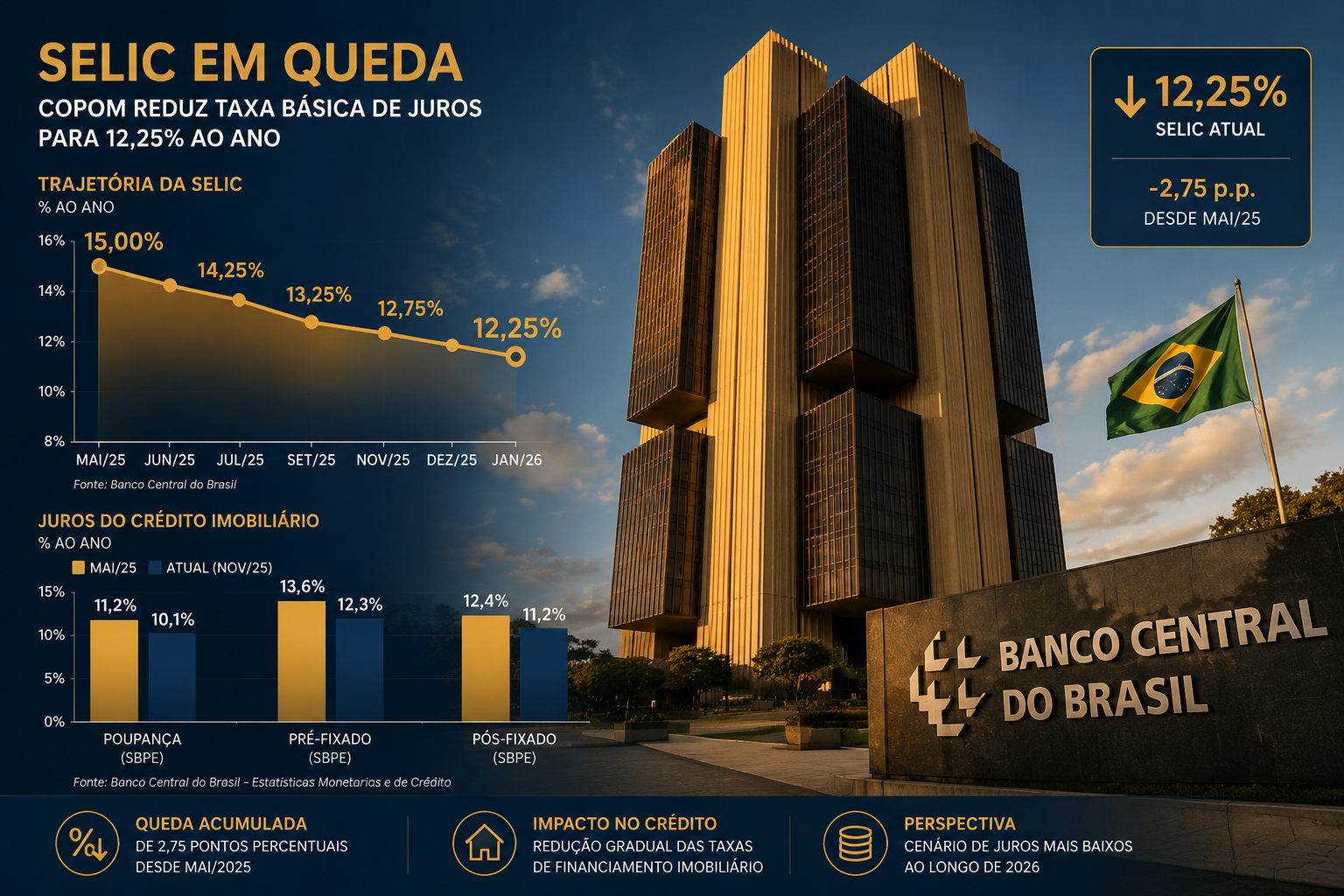

- The Selic rate currently stands at 14.75%, but market forecasts and the article’s central thesis project a trajectory toward 12.25% by end-2026, which would materially lower mortgage costs and expand the eligible buyer pool.

- Brazil’s residential market recorded a 19.3% increase in property launches in early 2026, building on a record base of 450,000 units delivered in 2025 [3].

- Government policy — including the expanded Minha Casa, Minha Vida (MCMV) Faixa 4 bracket and a raised SFH ceiling of R$2.25 million — is actively widening demand across income segments [3].

- A clear market bifurcation exists: the low-to-middle income segment is advancing rapidly through MCMV, while the mid-to-high-end segment remains rate-sensitive and is waiting for further Selic relief [3].

- Rental prices rose 4.40% in the first five months of 2026, outpacing inflation and reinforcing the financial case for purchasing over renting [3].

The Selic Rate in 2026: Where It Stands and Where It Is Headed

Current Rate Environment and Revised Projections

The Central Bank of Brazil’s Focus report, published on June 22, 2026, revised the median market forecast for the end-of-year Selic rate upward from 13.75% to 14.00%, citing heightened economic uncertainties and rising oil prices linked to geopolitical tensions in the Middle East [1]. Separately, Citi revised its own end-2026 Selic projection to 13.75% in May 2026, pointing to deteriorating inflation expectations and anticipating the final rate cut of the cycle to occur at the September policy meeting [2].

These revisions are significant. They reflect a more cautious easing path than many analysts predicted at the start of the year. The 12.25% target discussed in this article represents a more optimistic scenario — one that several market participants still consider achievable if inflation pressures ease in the second half of 2026 and the Central Bank resumes its cutting cycle with greater confidence.

“Even a partial reduction in the Selic rate from current levels would meaningfully reduce mortgage servicing costs for millions of Brazilian families, unlocking demand that has been suppressed for over two years.”

Why the Rate Level Matters for Housing

Brazil’s mortgage market is tightly linked to the Selic. As of February 2026, the average mortgage rate stood at 10.71% [7]. While that figure already reflects some discounting below the Selic — thanks to subsidized credit lines and FGTS-linked financing — any downward movement in the benchmark rate tends to reduce the cost of market-rate mortgages and free up household income for debt servicing.

A recent study estimated Brazil’s real neutral interest rate at 9.48% per annum as of May 2026 [6]. With the Selic sitting well above that level, monetary policy remains restrictive. The gap between the current rate and neutral represents both the constraint on the housing market today and the upside potential as that gap closes.

Key rate benchmarks to watch:

| Indicator | Value (2026) |

|---|---|

| Current Selic Rate | 14.75% |

| Focus Report End-2026 Forecast | 14.00% |

| Citi End-2026 Forecast | 13.75% |

| Optimistic Scenario (Article Thesis) | 12.25% |

| Estimated Real Neutral Rate | 9.48% |

| Average Mortgage Rate (Feb 2026) | 10.71% |

Residential Launch Activity: A Market Already in Motion

Record Volumes and Accelerating Pipeline

Even before any significant Selic relief materializes, Brazil’s residential developers have been moving aggressively. The market recorded a 19.3% increase in property launches at the start of 2026, layered on top of a record 450,000 units delivered in 2025 [3]. This is not speculative pipeline-building — it reflects genuine demand absorption and developer confidence in forward sales velocity.

A survey by ABRAINC and Deloitte reinforces this confidence: 97% of executives involved in the MCMV program plan to launch at least one new project within the next 12 months, and 94% intend to acquire new land [4]. These are not incremental adjustments — they represent a sector-wide commitment to scaling output.

For investors evaluating where to place capital, understanding which markets are driving this growth is essential. Coastal cities with strong internal migration and tourism demand — such as Florianópolis — have been outperforming national averages. Exploring the best places to invest in Brazil property provides a useful framework for identifying high-return locations within this broader national trend.

The MCMV Expansion: Widening the Buyer Pool

The Brazilian government has made deliberate structural moves to expand demand. Two policy changes are particularly consequential:

1. MCMV Faixa 4: A new income bracket targeting families earning up to R$13,000 per month, covering properties valued up to R$600,000. This bracket bridges the gap between the traditional subsidized housing market and the open market, capturing a large segment of middle-class buyers who previously fell outside MCMV eligibility [3].

2. Raised SFH Ceiling: The Housing Finance System (SFH) ceiling has been elevated to R$2.25 million, allowing more properties — particularly in high-cost urban markets — to qualify for regulated financing rates rather than free-market rates [3].

Together, these measures structurally expand the buyer pool independent of Selic movements. When rate cuts do materialize, they will amplify an already-widening demand base rather than creating it from scratch.

Government Liquidity Injection

Beyond the MCMV expansion, the government released R$35 billion from compulsory deposits to stimulate the housing sector [3]. This injection directly increases the volume of credit available for residential mortgages, reducing the funding constraint that had limited bank lending even when borrowers were qualified.

The combined effect of these measures — new income brackets, higher SFH ceilings, and fresh liquidity — creates a policy environment that is actively working to offset the headwinds from elevated interest rates.

Market Bifurcation: Two Speeds, One Sector

Low-to-Middle Income: Full Acceleration

The MCMV segment is operating at high speed. With government subsidies absorbing much of the interest rate burden, buyers in this segment are largely insulated from Selic fluctuations. Developer confidence in this segment is near-universal, as evidenced by the ABRAINC-Deloitte survey data [4].

For developers focused on this segment, the strategic priority is land acquisition and construction capacity rather than demand generation. The buyer pool is there — the constraint is supply.

Developers and investors interested in understanding how sales performance in this environment translates to project-level returns can find relevant analysis in this overview of how sales performance is transforming Florianópolis real estate.

Mid-to-High-End: Rate-Sensitive and Waiting

The medium-to-high-end segment tells a different story. Here, buyers are financing at market rates, and the difference between a 14.75% Selic and a 12.25% Selic translates directly into monthly payment affordability [3]. This segment is not stalled — but it is cautious.

The practical implication is that a significant volume of latent demand exists in this segment, compressed by current financing costs. As the Selic drops, that demand does not gradually unlock — it tends to release in bursts as buyer confidence crosses affordability thresholds.

Segment comparison at a glance:

| Segment | Current Status | Primary Driver | Rate Sensitivity |

|---|---|---|---|

| MCMV / Low-Income | High activity | Government subsidy | Low |

| MCMV Faixa 4 / Middle | Growing fast | New bracket eligibility | Moderate |

| Mid-to-High-End | Cautious | Market-rate financing | High |

| Luxury / Premium | Selective | Equity buyers, FDI | Low-Moderate |

The Rental Market as a Demand Catalyst

One often-overlooked driver of purchase demand is the rental market. Rental prices in Brazil rose 4.40% in the first five months of 2026, outpacing general inflation [3]. When renting becomes more expensive relative to owning — particularly as mortgage rates decline — the rent-versus-buy calculation shifts decisively toward purchase.

This dynamic is already visible in high-demand urban markets. Investors seeking yield through residential property are finding that investing in studios in Florianópolis offers a compelling combination of rental income and capital appreciation in a market where supply remains constrained.

Strategic Implications: Scaling Residential Launches as Buyer Pools Expand in Brazil

Developer Strategy: Pipeline Timing and Land Banking

For developers, the Selic rate drop to 12.25% by end-2026 scenario — or even the more conservative 13.75% to 14.00% range — creates a clear strategic imperative: build the pipeline now, launch when rates fall.

The typical residential development cycle in Brazil runs 24 to 36 months from land acquisition to delivery. Developers who acquire land and begin approvals in 2026 are positioning for deliveries in 2028 and 2029 — precisely when a more accommodative rate environment should be generating peak demand.

Key developer actions in 2026:

- Accelerate land banking in urban peripheries with strong employment and infrastructure growth

- Prioritize mid-tier product that qualifies for MCMV Faixa 4 or upper SFH brackets

- Build sales teams and digital marketing infrastructure to capture demand surges quickly

- Monitor Selic trajectory monthly and adjust launch timing accordingly

For buyers considering off-plan purchases, the dynamics are equally favorable. The value of buying off-plan in Brazilian real estate is particularly pronounced in rising markets where price appreciation between purchase and delivery can be substantial.

Investor Positioning: High-Demand Urban Peripheries

The concept of “urban periphery” deserves specific attention. Brazil’s major metropolitan areas — São Paulo, Rio de Janeiro, Curitiba, Florianópolis — have seen their most dynamic residential growth not in their historic cores but in their expanding peripheries, where land costs are lower, new infrastructure is being built, and first-time buyers can access homeownership.

These zones are precisely where the MCMV Faixa 4 expansion has the most impact. A family earning R$12,000 per month, previously excluded from subsidized programs, can now access financing for a R$550,000 apartment in a well-located peripheral neighborhood. That is a transformative change in buyer pool composition.

Florianópolis exemplifies this dynamic. The growth of the Ingleses region in Florianópolis illustrates how infrastructure investment and quality-of-life factors are driving residential demand in areas that were considered peripheral just five years ago.

The Foreign Investment Angle

Brazil’s real estate sector is also attracting increased foreign direct investment, drawn by the combination of a depreciating real against major currencies, high nominal yields, and the structural growth story in residential demand [5]. For international investors, the Selic rate trajectory matters in two ways: it affects local financing costs for co-investment structures, and it signals the overall health of the Brazilian macroeconomic environment.

A declining Selic — even to the 13.75% to 14.00% range forecast by major banks — signals that inflation is being managed and that the economy is stabilizing. That signal alone can unlock foreign capital that has been waiting on the sidelines.

Risks and Considerations

No analysis of the Selic rate drop to 12.25% scenario would be complete without acknowledging the risks. The Focus report revision to 14.00% [1] and Citi’s 13.75% projection [2] both reflect genuine uncertainty. Several factors could delay or reverse the easing cycle:

- Persistent inflation: If core inflation remains above target, the Central Bank will maintain a restrictive stance longer than markets expect.

- Geopolitical oil shocks: Rising energy prices feed directly into Brazilian inflation, given the country’s fuel pricing dynamics.

- Fiscal concerns: Any deterioration in Brazil’s fiscal position could weaken the real and import inflationary pressure, constraining rate cuts.

- Global rate environment: If the U.S. Federal Reserve delays its own easing cycle, emerging market central banks including Brazil face pressure to maintain higher rates to prevent capital outflows.

Developers and investors should stress-test their business cases against a scenario where the Selic ends 2026 at 14.00% rather than 12.25%. Projects that are viable at 14.00% with MCMV support are more resilient than those dependent on market-rate financing improvement alone.

Conclusion

The thesis of a Selic rate drop to 12.25% by end-2026 — and the consequent scaling of residential launches as buyer pools expand in Brazil — represents a high-conviction opportunity with meaningful execution risk. The structural foundations are solid: record launch volumes, a 19.3% year-on-year increase in new projects [3], near-universal developer confidence [4], government policy actively widening eligibility, and a rental market that is pushing households toward ownership.

The rate trajectory is less certain than the structural story. Revised forecasts from the Focus report and Citi place the likely end-2026 Selic in the 13.75% to 14.00% range [1][2], which is meaningfully higher than 12.25% but still represents continued easing from the current 14.75% level.

Actionable next steps for different stakeholders:

- Developers: Accelerate land acquisition in MCMV-eligible urban peripheries now. Build pipeline for 2028-2029 delivery windows. Prioritize Faixa 4-compatible product specifications.

- Investors: Evaluate off-plan purchases in high-demand coastal and metropolitan markets. Model returns under both the 12.25% and 14.00% Selic scenarios. Consider rental yield as a base case with capital appreciation as upside.

- Homebuyers: Monitor the September 2026 Copom meeting closely — Citi anticipates a rate cut at that meeting [2]. Use the current period to complete credit pre-approval and identify target properties before demand surges.

- Foreign investors: Engage with local developers and legal advisors now to structure investment vehicles that can move quickly when the rate environment confirms the easing trend.

The Brazilian residential market in 2026 is not waiting for perfect conditions. It is building toward them — and the buyers, developers, and investors who position early will capture the most value from the cycle that follows.

For those exploring specific opportunities in Brazil’s most dynamic residential markets, reviewing current residential developments and launches provides a direct window into where the market is moving.

References

[1] Expectativa Para A Selic No Fim De 2026 Passa De 1375 Para 1400 No Focus Do Bc – https://www.bol.uol.com.br/economia/2026/06/22/expectativa-para-a-selic-no-fim-de-2026-passa-de-1375-para-1400-no-focus-do-bc.htm?utm_source=openai

[2] Citi Eleva A 1375 Projecao De Selic No Final De 2026 Citando Deterioracao De Expectativas Para Inflacao – https://economia.uol.com.br/noticias/reuters/2026/05/26/citi-eleva-a-1375-projecao-de-selic-no-final-de-2026-citando-deterioracao-de-expectativas-para-inflacao.htm?utm_source=openai

[3] Gri Residencial Brasil 2026 Radar Mercado Ciclo Imobiliario – https://news.griinstitute.org/pt/mercado-imobiliario/gri-residencial-brasil-2026-radar-mercado-ciclo-imobiliario?utm_source=openai

[4] Deloitte Abrainc Quarto Trimestre – https://www.deloitte.com/br/pt/about/press-room/deloitte-abrainc-quarto-trimestre.html?utm_source=openai

[5] Mercado Imobiliario Aquecido Aponta Para Novo Boom Do Setor Em 2026 – https://www.cnnbrasil.com.br/economia/macroeconomia/mercado-imobiliario-aquecido-aponta-para-novo-boom-do-setor-em-2026/?utm_source=openai

[6] arxiv – https://arxiv.org/abs/2606.19000?utm_source=openai

[7] Price History – https://www.globalpropertyguide.com/latin-america/brazil/price-history?utm_source=openai