Brazil’s real estate market is experiencing a transformative shift in 2026, and developers who understand this evolution stand to gain significantly. With fixed-rate mortgages rising in Brazil 2026 and a projected 14% credit expansion reshaping the financing landscape, the opportunity to leverage this momentum for mid-range launches has never been stronger. As the Central Bank’s anticipated SELIC rate stabilization at 9.25% enables more predictable financing models, developers can now target the sweet spot between affordability and profitability—particularly in the mid-range segment that’s outperforming luxury markets.

The convergence of government housing programs, evolving buyer preferences, and stabilizing interest rates creates a perfect storm for strategic developers ready to capitalize on how developers can leverage 14% credit expansion for mid-range launches in 2026.

Key Takeaways

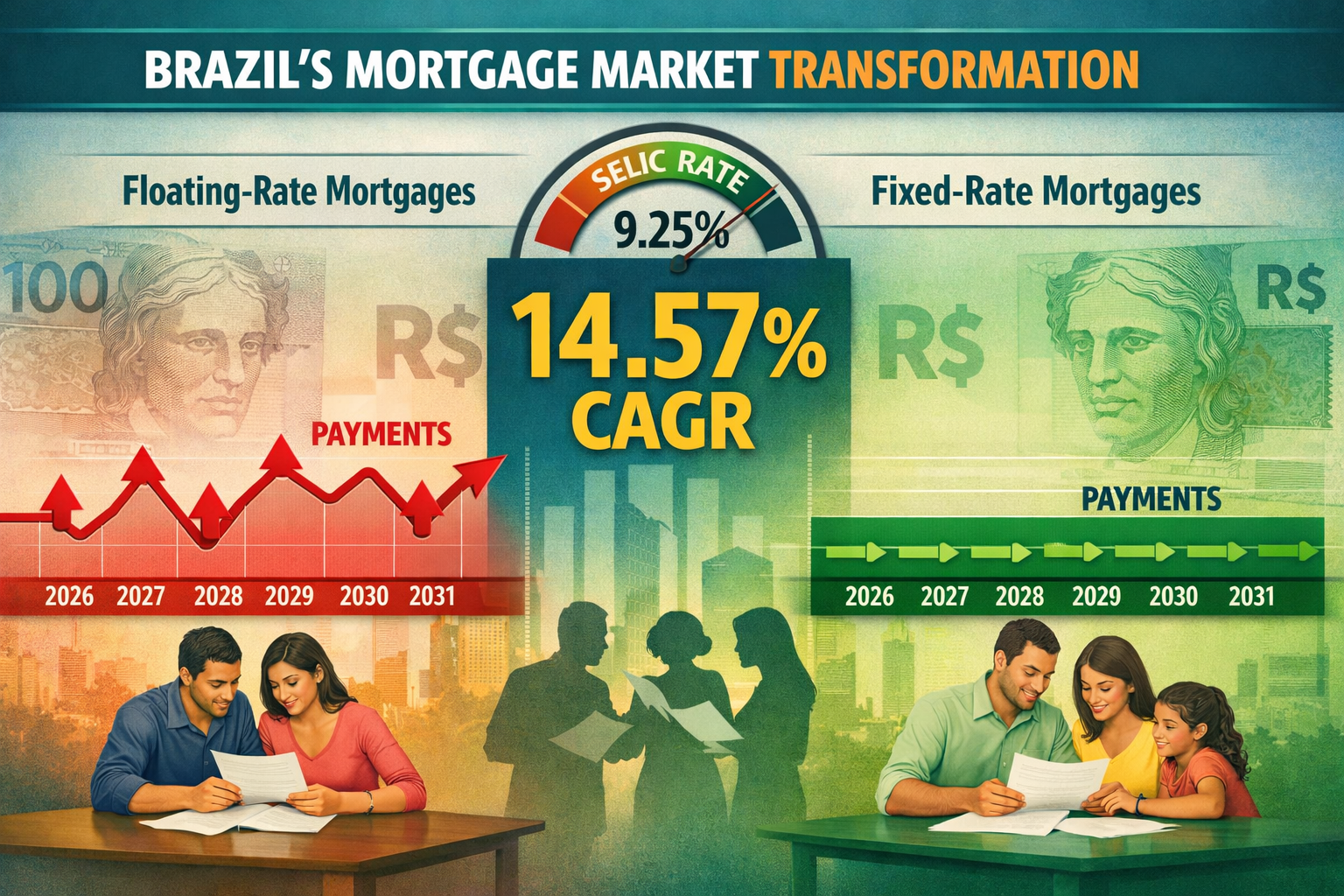

✅ Fixed-rate mortgages are growing at 14.57% CAGR through 2031, significantly outpacing Brazil’s overall mortgage market growth, creating unprecedented demand for predictable financing options [2]

✅ The 11-20 year tenure segment is expanding at 13.67% CAGR, representing the fastest-growing mortgage duration and ideal target for mid-range property launches [2]

✅ Brazil’s SFH ceiling increased to BRL 2.25 million, opening substantial opportunities for developers to position mid-range properties within subsidized financing frameworks [2]

✅ $39.8 billion in housing program investments for 2026 provides a stable demand foundation, with Minha Casa, Minha Vida targeting 1 million additional units [3]

✅ Strategic financing partnerships and pricing optimization enable developers to accelerate sales velocity while maintaining margins in the stabilizing rate environment

Understanding the Fixed-Rate Mortgage Revolution in Brazil’s 2026 Market

The Shift from Floating to Fixed: What’s Driving the Change?

Brazil’s mortgage market has historically been dominated by floating-rate products, which currently account for 93.25% of mortgage balances [2]. However, 2026 marks a pivotal turning point. Fixed-rate financing models are gaining significant traction as borrowers seek greater long-term financial certainty in an uncertain economic environment [1].

Why the sudden shift? Several factors converge:

- 🏦 Updated amortization guidance that stabilizes nominal installments and improves payment predictability for homeowners

- 📉 SELIC rate stabilization projected at 9.25% for 2026, down from the nearly two-decade high of 15% in January 2026 [3][4]

- 💰 Middle-income buyer preferences for household budgeting certainty, especially within the new SFH ceiling band

- 📊 Institutional confidence in Brazil’s economic trajectory encouraging lenders to offer fixed products

The Brazil home loan market was valued at USD 62.99 billion in 2026 and is projected to grow at a CAGR of 10.72% to reach USD 104.81 billion by 2031 [2]. Within this expansion, fixed-rate products are growing at 14.57% CAGR—a growth rate that substantially outpaces the overall market.

The Numbers Behind the 14% Credit Expansion

The 14% real estate credit expansion projected for 2026 [1] represents more than just numerical growth—it signals increased stability in the mortgage sector and anticipated interest rate declines that make homeownership more accessible.

| Market Indicator | 2026 Value | Growth Rate | 2031 Projection |

|---|---|---|---|

| Total Home Loan Market | USD 62.99 billion | 10.72% CAGR | USD 104.81 billion |

| Fixed-Rate Segment | Growing rapidly | 14.57% CAGR | Dominant segment |

| 11-20 Year Tenure | Fastest growing | 13.67% CAGR | Primary tenure choice |

| Credit Expansion | 14% in 2026 | Year-over-year | Continued growth |

This expansion is fueled by:

- Government housing program investments totaling approximately $39.8 billion in 2026, combining federal budget resources, FGTS funds, and the Brazilian Social Fund [3]

- Minha Casa, Minha Vida (MCMV) program aiming to contract an additional 1 million housing units through the end of 2026 [3]

- Reforma Casa Brasil program allocating $7.4 billion exclusively for housing improvements [3]

- Increased SFH ceiling to BRL 2.25 million, supporting mid-tenure and fixed-structure adoption while preserving affordability in subsidy-linked segments [2]

For developers exploring best places to invest in Brazil property, understanding these market dynamics is essential for strategic positioning.

Interest Rate Environment: From 15% to Stabilization

Brazil’s SELIC rate stood at 15% as of January 2026—the highest level in nearly two decades [3][4]. This elevated rate environment kept mortgage costs high, with Q1 2025 mortgage rates averaging 10.02% and Q2 reaching 10.29% [5].

However, the Central Bank’s projected SELIC rate of 9.25% for 2026 signals a strategic move towards stabilization [1]. This adjustment is expected to:

- ✅ Directly lower mortgage costs for new borrowers

- ✅ Increase affordability in the mid-range segment

- ✅ Encourage fixed-rate adoption as rate certainty becomes more attractive

- ✅ Accelerate purchase decisions among fence-sitting buyers

“The transition to fixed-rate mortgages represents a fundamental shift in how Brazilian buyers approach homeownership—from uncertainty to predictability, from hesitation to confidence.”

Strategic Opportunities: How Developers Can Leverage 14% Credit Expansion for Mid-Range Launches

Targeting the Sweet Spot: Mid-Range Properties Under BRL 2.25 Million

The increase in the SFH (Sistema Financeiro de Habitação) ceiling to BRL 2.25 million [2] creates a substantial opportunity zone for developers. Properties priced within this threshold qualify for subsidized financing frameworks, making them significantly more attractive to middle-income buyers.

Why mid-range outperforms luxury in 2026:

- 📈 Broader buyer pool: Middle-income families represent the largest demographic segment

- 💳 Financing accessibility: SFH qualification opens doors to favorable terms

- 🎯 Government program alignment: MCMV and related initiatives target this segment

- ⚡ Faster sales velocity: Higher demand translates to quicker inventory turnover

- 🔒 Lower market risk: Economic volatility impacts luxury segments more severely

Developers should focus on unit configurations that maximize value perception while staying comfortably under the SFH ceiling:

- 2-bedroom apartments: 55-70m² in emerging neighborhoods

- 3-bedroom units: 70-90m² in established areas with infrastructure

- Studio and 1-bedroom: High-density urban areas near employment centers

For insights on studio investments, review the advantages of investing in studios in Florianópolis.

Optimizing Pricing Strategy in the Fixed-Rate Era

With fixed-rate mortgages gaining traction, developers must recalibrate pricing strategies to align with buyer psychology and financing realities.

Key pricing considerations:

Payment predictability premium: Buyers will pay slightly more for properties that qualify for fixed-rate financing with stable monthly payments

Tenure-aligned pricing: The 11-20 year tenure segment growing at 13.67% CAGR [2] indicates buyers are balancing affordability with total interest costs—price units to optimize monthly payments in this range

Financing-inclusive marketing: Present total cost of ownership (TCO) including fixed-rate mortgage scenarios, not just purchase price

Phased pricing strategies: Early-bird discounts for pre-construction purchases that lock in favorable financing terms

Example Pricing Framework:

| Unit Type | Target Price | Monthly Payment (15-year fixed @ 9.5%) | Target Buyer |

|---|---|---|---|

| Studio 35m² | BRL 350,000 | BRL 3,655 | Young professionals |

| 2BR 65m² | BRL 650,000 | BRL 6,788 | Small families |

| 3BR 85m² | BRL 950,000 | BRL 9,919 | Growing families |

Building Strategic Financing Partnerships

The rise of fixed-rate mortgages in Brazil 2026 creates opportunities for developers to differentiate through strategic financing partnerships with banks and financial institutions.

Partnership strategies that accelerate sales:

🤝 Pre-approved financing programs: Work with lenders to offer conditional pre-approvals during launch events, reducing buyer decision friction

🤝 Co-branded financing products: Develop exclusive fixed-rate mortgage products with partner banks that offer competitive rates for your developments

🤝 Streamlined documentation: Establish digital documentation workflows with lending partners to reduce approval timelines from weeks to days

🤝 Financing education programs: Host buyer seminars explaining fixed-rate advantages, featuring partner bank representatives to build trust

🤝 Construction-to-permanent loans: Offer seamless transitions from construction financing to permanent fixed-rate mortgages, simplifying the buyer journey

Developers working in high-growth regions like Ingleses in Florianópolis can particularly benefit from these partnership models, as infrastructure improvements and quality of life factors amplify buyer interest.

Location Selection: Where Mid-Range Launches Excel

Not all markets are created equal when leveraging the 14% credit expansion. Developers should prioritize locations where:

✅ Infrastructure investment is accelerating (transportation, schools, healthcare)

✅ Employment centers are expanding (technology hubs, industrial zones)

✅ Government housing programs are concentrated (MCMV target areas)

✅ Middle-income demographics are growing (emerging neighborhoods)

✅ Land costs remain reasonable (preserving margin while staying under SFH ceiling)

Top-performing market characteristics in 2026:

- Secondary cities experiencing population growth from major metro areas

- Suburban corridors with improving connectivity to urban centers

- Coastal regions with tourism and remote work appeal

- University towns with stable rental demand supporting investment buyers

For comprehensive market analysis, explore the Greater Florianópolis real estate market outlook and understand regional performance dynamics.

Sales Acceleration Tactics in the Stabilizing Rate Environment

As interest rates stabilize and fixed-rate products become more accessible, developers can implement tactical approaches to accelerate sales velocity:

1. Rate-Lock Incentives

Offer buyers the ability to lock in current fixed rates during pre-construction phases, protecting them from potential rate increases during the construction period.

2. Financing Contingency Removal Bonuses

Provide price discounts or upgrade packages for buyers who waive financing contingencies by securing pre-approved fixed-rate mortgages before contract signing.

3. Payment Plan Flexibility

Structure payment plans that mirror the predictability of fixed-rate mortgages—equal installments during construction that transition seamlessly to mortgage payments upon delivery.

4. Total Cost Transparency

Create comprehensive cost calculators showing:

- Purchase price

- Fixed-rate mortgage monthly payment (15, 18, and 20-year scenarios)

- Property taxes and HOA fees

- Total cost of ownership over tenure period

5. Competitive Comparison Marketing

Demonstrate how mid-range properties with fixed-rate financing offer superior value compared to:

- Luxury properties with higher financing costs

- Rental alternatives with annual increases

- Older properties requiring renovation investments

6. Digital-First Sales Processes

Implement virtual tours, digital documentation, and online financing applications to reduce friction and accelerate decision-making among tech-savvy middle-income buyers.

Developers can learn from successful sales performance transformations in Florianópolis to optimize their approach.

Construction and Delivery Timing Optimization

With the 14% credit expansion and fixed-rate adoption accelerating buyer interest, developers must align construction timelines with market momentum:

Strategic timing considerations:

- ⏱️ Launch during rate stabilization windows: Capitalize on buyer confidence when SELIC stabilizes

- ⏱️ Stagger unit releases: Create urgency through phased releases rather than full inventory launches

- ⏱️ Accelerate construction schedules: Reduce time-to-delivery to capture buyers before potential market shifts

- ⏱️ Coordinate with government program cycles: Align deliveries with MCMV funding disbursement periods

For example, review the accelerated construction progress at Tramonto developments to understand how construction velocity impacts market positioning.

Risk Mitigation in the Evolving Credit Landscape

While the 14% credit expansion presents opportunities, prudent developers must also manage associated risks:

Key risk factors and mitigation strategies:

| Risk Factor | Mitigation Strategy |

|---|---|

| Interest rate volatility | Partner with lenders offering rate-lock programs; price conservatively |

| Buyer financing failures | Implement robust pre-qualification processes; maintain buyer pipeline depth |

| Construction cost inflation | Lock in material contracts early; build contingency buffers into budgets |

| Regulatory changes | Monitor SFH ceiling adjustments; maintain flexible pricing structures |

| Market oversupply | Conduct thorough market absorption studies; phase releases strategically |

Maximizing Returns: Advanced Strategies for Mid-Range Development Success

Value Engineering Without Compromising Quality

To maintain margins while pricing under the BRL 2.25 million SFH ceiling, developers must master value engineering—optimizing costs without sacrificing buyer perception of quality.

Effective value engineering approaches:

- 🏗️ Standardized floor plans: Reduce architectural complexity while maximizing functional space

- 🏗️ Efficient building systems: Invest in construction methods that reduce labor and timeline costs

- 🏗️ Strategic material selection: Choose durable, attractive materials with favorable cost-performance ratios

- 🏗️ Shared amenities: Provide high-impact common areas (fitness centers, coworking spaces) that enhance value perception at lower per-unit costs

- 🏗️ Technology integration: Smart home features and energy efficiency that command premium pricing with minimal cost additions

Buyer Persona Alignment for Mid-Range Success

Understanding the 11-20 year tenure buyer [2]—the fastest-growing segment—is critical for product development and marketing success.

Primary buyer personas in the mid-range fixed-rate segment:

Persona 1: The Young Professional Couple

- Age: 28-35

- Income: Combined BRL 12,000-18,000/month

- Priorities: Location near employment, modern amenities, investment potential

- Financing preference: 15-year fixed-rate for faster equity building

Persona 2: The Growing Family

- Age: 32-42

- Income: Combined BRL 15,000-25,000/month

- Priorities: School proximity, safety, space for children, community

- Financing preference: 18-20 year fixed-rate for payment affordability

Persona 3: The Strategic Investor

- Age: 35-50

- Income: BRL 20,000+/month

- Priorities: Rental yield, appreciation potential, financing leverage

- Financing preference: Maximum tenure to optimize cash flow

Tailor unit configurations, amenities, and marketing messages to these distinct personas for maximum conversion efficiency.

Marketing in the Fixed-Rate Era

Traditional real estate marketing emphasized property features and location. In 2026, successful marketing emphasizes financial predictability and total cost of ownership.

Effective marketing messages for mid-range fixed-rate launches:

✨ “Own Your Future: Fixed Payments for 15 Years—No Surprises”

✨ “BRL 4,500/Month Today, BRL 4,500/Month in 2041—Guaranteed”

✨ “Stop Paying Rising Rent—Lock Your Housing Cost Forever”

✨ “Qualify for SFH Financing: Lower Rates, Better Terms, Faster Approval”

✨ “Build Equity While Others Build Their Landlord’s Wealth”

Marketing channel optimization:

- 📱 Digital-first approach: Target middle-income buyers on social media with financing calculators and payment comparison tools

- 📱 Content marketing: Educational content explaining fixed-rate advantages and SFH qualification

- 📱 Partnership marketing: Co-branded campaigns with financing partners highlighting exclusive fixed-rate products

- 📱 Testimonial marketing: Showcase early buyers who secured favorable fixed-rate terms

- 📱 Local community engagement: Sponsor neighborhood events in target demographics

Explore current market news and trends to stay informed about evolving buyer preferences and marketing opportunities.

Leveraging Government Programs for Competitive Advantage

The Minha Casa, Minha Vida program’s goal of contracting 1 million additional housing units through the end of 2026 [3] creates substantial opportunities for developers who understand program mechanics.

MCMV integration strategies:

- Design for program compliance: Ensure unit specifications meet MCMV requirements from the planning phase

- Streamlined program registration: Establish relationships with program administrators for faster approvals

- Buyer education: Help qualified buyers navigate MCMV application processes

- Hybrid inventory approach: Mix MCMV-qualifying units with market-rate units to optimize revenue

- Subsidy maximization: Structure pricing to capture maximum available subsidies while maintaining margins

The Reforma Casa Brasil program’s $7.4 billion allocation [3] for housing improvements also creates opportunities for developers offering renovation-friendly units or partnering on improvement programs.

Portfolio Diversification Across Tenure Segments

While the 11-20 year tenure segment grows at 13.67% CAGR [2], sophisticated developers diversify across multiple tenure targets:

Multi-tenure product strategy:

- 10-15 year products: Higher monthly payments, faster equity building, appeals to high-income buyers

- 15-18 year products: Sweet spot balancing affordability and total interest costs

- 18-20 year products: Maximum affordability, targets first-time buyers and lower-income segments

- 20+ year products: Emerging segment for maximum payment reduction

By offering units at various price points aligned with different tenure preferences, developers can capture broader market segments and reduce concentration risk.

Implementation Roadmap: Launching Mid-Range Developments in 2026

Phase 1: Market Analysis and Site Selection (Months 1-3)

Critical activities:

- ✅ Conduct detailed absorption studies in target markets

- ✅ Analyze competitive mid-range inventory and pricing

- ✅ Identify sites within SFH ceiling price feasibility

- ✅ Assess proximity to infrastructure, employment, and amenities

- ✅ Evaluate local government program participation rates

Deliverables: Site acquisition strategy, preliminary financial pro forma, target buyer persona definition

Phase 2: Product Development and Financing Partnerships (Months 4-6)

Critical activities:

- ✅ Design unit mix optimized for 11-20 year tenure buyers

- ✅ Develop value engineering specifications

- ✅ Establish partnerships with 2-3 lending institutions

- ✅ Create co-branded fixed-rate financing products

- ✅ Obtain necessary permits and approvals

Deliverables: Final architectural plans, financing partnership agreements, construction timeline, marketing strategy

Phase 3: Pre-Launch Marketing and Sales Preparation (Months 7-8)

Critical activities:

- ✅ Build digital marketing infrastructure (website, calculators, virtual tours)

- ✅ Train sales team on fixed-rate financing advantages

- ✅ Develop comprehensive buyer education materials

- ✅ Establish pre-qualification processes with lending partners

- ✅ Create launch event strategy and materials

Deliverables: Marketing assets, sales team training completion, pre-qualified buyer pipeline, launch event plan

Phase 4: Launch and Sales Acceleration (Months 9-12)

Critical activities:

- ✅ Execute launch event with financing partner participation

- ✅ Implement rate-lock and early-buyer incentive programs

- ✅ Monitor sales velocity and adjust pricing/incentives as needed

- ✅ Begin construction on schedule

- ✅ Maintain buyer communication and confidence

Deliverables: Target 40-60% sales within first 6 months, construction progress milestones, buyer satisfaction metrics

Phase 5: Construction and Delivery (Months 13-30)

Critical activities:

- ✅ Maintain accelerated construction schedule

- ✅ Provide regular progress updates to buyers

- ✅ Coordinate mortgage conversion from construction to permanent financing

- ✅ Prepare units for delivery

- ✅ Execute smooth handover process

Deliverables: On-time unit delivery, successful mortgage conversions, positive buyer testimonials, portfolio expansion planning

For developers interested in learning more about successful development approaches, explore Quadragon’s development portfolio and company background.

Case Study: Mid-Range Success in Brazil’s Emerging Markets

Project Profile: Hypothetical “Vista Verde” Development

- Location: Emerging suburban corridor, 25km from major employment center

- Units: 240 apartments (mix of 2BR and 3BR)

- Price range: BRL 550,000 – BRL 850,000 (well under SFH ceiling)

- Target tenure: 15-18 years

- Financing partnership: Co-branded fixed-rate product at 9.2%

Strategic Implementation:

- Pricing strategy: Units priced to deliver monthly payments of BRL 4,200-6,500 on 15-year fixed mortgages

- Buyer targeting: Young professional couples and growing families within 30-minute commute

- Amenity package: Coworking space, fitness center, children’s play area, green spaces

- Marketing approach: Digital-first with financing calculator prominence, educational webinars on fixed-rate advantages

- Sales incentives: 5% discount for buyers with pre-approved fixed-rate financing

Results (Projected):

- ✅ 55% sales within 6 months of launch

- ✅ 85% sales within 12 months

- ✅ Average time from first contact to contract: 21 days

- ✅ 92% buyer satisfaction with financing process

- ✅ 15% margin on total project cost

Key Success Factors:

- Strategic location in growth corridor with improving infrastructure

- Pricing optimization for target tenure segment

- Strong financing partnership reducing buyer friction

- Value engineering maintaining quality while preserving margins

- Marketing emphasis on payment predictability and total cost of ownership

Future Outlook: Beyond 2026

While 2026 presents exceptional opportunities for developers leveraging fixed-rate mortgage growth and credit expansion, forward-thinking developers should also consider longer-term trends:

Emerging trends to monitor:

📊 Continued fixed-rate adoption: As floating-rate mortgages currently hold 93.25% of balances [2], the multi-year transition to fixed products will create sustained demand

📊 Technology integration: Smart home features and energy efficiency will become table stakes in mid-range developments

📊 Demographic shifts: Remote work trends may continue driving demand in secondary cities and coastal regions

📊 Sustainability requirements: Environmental regulations and buyer preferences will increasingly favor green building practices

📊 Financing innovation: New mortgage products blending fixed and floating elements may emerge to optimize buyer flexibility

Developers who establish strong positions in the mid-range segment during 2026’s favorable conditions will be well-positioned to capitalize on these longer-term trends.

For insights into living in high-growth regions, explore life in Florianópolis and understand lifestyle factors driving buyer decisions.

Conclusion

Fixed-rate mortgages rise in Brazil 2026 represents far more than a financing trend—it’s a fundamental transformation in how Brazilians approach homeownership, and how developers can leverage 14% credit expansion for mid-range launches will determine market leadership in the years ahead.

The convergence of stabilizing interest rates, government housing program investments totaling $39.8 billion, the increased SFH ceiling to BRL 2.25 million, and the explosive 14.57% CAGR growth in fixed-rate products creates an unprecedented window of opportunity for strategic developers.

Key success factors for 2026 and beyond:

✅ Target the mid-range segment under the SFH ceiling where demand, affordability, and government support converge

✅ Build strategic financing partnerships that reduce buyer friction and differentiate your developments

✅ Optimize for the 11-20 year tenure buyer who represents the fastest-growing segment at 13.67% CAGR

✅ Emphasize payment predictability in marketing and sales, not just property features

✅ Implement value engineering to maintain margins while staying within SFH qualification thresholds

✅ Accelerate sales velocity through rate-lock programs, pre-approvals, and digital-first processes

The developers who will thrive are those who recognize that in 2026, they’re not just selling properties—they’re selling financial predictability, homeownership accessibility, and long-term wealth building to Brazil’s expanding middle class.

Next Steps for Developers

Immediate actions to capitalize on this opportunity:

- Conduct market analysis in your target regions to identify optimal mid-range development sites

- Initiate conversations with lending partners to explore co-branded fixed-rate financing products

- Review your current portfolio and identify opportunities to reposition existing inventory for the fixed-rate market

- Develop buyer education materials explaining fixed-rate advantages and SFH qualification

- Engage with government housing programs to understand MCMV and Reforma Casa Brasil opportunities

For personalized guidance on leveraging Brazil’s 2026 real estate opportunities, contact Quadragon’s development team to discuss strategic partnership opportunities.

The fixed-rate mortgage revolution is here. The 14% credit expansion is real. The mid-range segment is ready. The only question is: Will you lead, or will you follow?

References

[1] Brazil Real Estate Market Trends 2026 An Institutional Investors Guide – https://www.riotimesonline.com/brazil-real-estate-market-trends-2026-an-institutional-investors-guide/

[2] Brazil Home Loan Market – https://www.mordorintelligence.com/industry-reports/brazil-home-loan-market

[3] Brazils Construction Sector 2026 Housing Programs Support Rates High Risks Persist – https://www.fastmarkets.com/insights/brazils-construction-sector-2026-housing-programs-support-rates-high-risks-persist/

[4] Brazil Price Forecasts – https://thelatinvestor.com/blogs/news/brazil-price-forecasts

[5] Mortgage Interest Rate – https://www.globalpropertyguide.com/latin-america/brazil/mortgage-interest-rate