The Logistics Warehousing Boom Near Port of Santos: Development Strategies for 2026 E-Commerce Driven Demand represents one of Latin America’s most compelling commercial real estate opportunities. With record-low vacancy rates hovering below 3% and the port handling an unprecedented 12.7 million tonnes of cargo in January 2026 alone—a 9.5% year-over-year surge—developers and investors are racing to capitalize on infrastructure synergies that promise exceptional yields. As e-commerce reshapes supply chains and re-shoring trends accelerate, the Santos logistics corridor has emerged as Brazil’s premier gateway for modern warehousing development.

Key Takeaways

✅ Record Port Performance: Santos achieved 467,000 TEUs in January 2026, the strongest January performance ever recorded, driving unprecedented demand for nearby warehousing facilities

✅ Infrastructure Investment Surge: Over $1.5 billion in port expansions, including DP World’s $275 million terminal project and the upcoming STS-10 mega-terminal auction, will increase capacity to 9-10 million TEUs annually

✅ Prime Investment Window: Commercial real estate in Santos logistics hubs forecasts a 3.63% CAGR through 2034, with vacancy rates at historic lows and rental yields reaching 8-12% in strategic corridors

✅ E-Commerce Catalyst: Brazil’s digital commerce explosion combined with re-shoring manufacturing trends has created insatiable appetite for modern, tech-enabled warehouse space within 50km of port terminals

✅ Strategic Site Selection: Proximity to expanded port infrastructure, multimodal transportation access, and last-mile delivery capabilities determine premium positioning for warehouse developments

Understanding the Logistics Warehousing Boom Near Port of Santos in 2026

The Santos metropolitan region has transformed into Brazil’s logistics powerhouse, driven by converging forces that have created perfect conditions for warehouse development. The Logistics Warehousing Boom Near Port of Santos: Development Strategies for 2026 E-Commerce Driven Demand stems from fundamental shifts in global trade patterns, domestic consumption growth, and infrastructure modernization.

The Perfect Storm: Why Santos Now?

Several critical factors have aligned to create this unprecedented opportunity:

📊 Port Capacity Expansion: The Port of Santos handled 180 million tonnes in 2024—a staggering 34% increase from 2019—and is rapidly approaching maximum capacity. The scheduled STS-10 terminal auction in 2026, backed by BRL 6.4 billion (USD 1.2 billion) in investment, will catapult Brazil from 45th to 15th position in global container traffic rankings.

🚢 Operational Bottlenecks Creating Urgency: In early 2026, nearly 60% of vessels arriving at Santos experienced altered operational deadlines, with rates reaching 75% during peak periods in September 2025. These delays generate additional storage costs and fines for exporters, making proximate warehousing facilities invaluable for buffer inventory and rapid turnaround.

📦 E-Commerce Explosion: Brazil’s online retail sector continues explosive growth, requiring sophisticated fulfillment infrastructure near major ports. The demand for last-mile distribution centers, cross-docking facilities, and automated warehouses has outpaced supply by significant margins.

🌍 Re-Shoring and Nearshoring Trends: Global manufacturers increasingly favor Latin American production to reduce supply chain vulnerabilities exposed during recent disruptions. Santos serves as the natural gateway for these operations, requiring modern industrial facilities with advanced logistics capabilities.

Record-Breaking Performance Metrics

The numbers tell a compelling story. January 2026’s 12.7 million tonnes of cargo represented not just a 9.5% increase over January 2025, but also a 6.8% jump above the previous 2024 record of 11.9 million tonnes. Container throughput specifically reached 467,000 TEUs—the strongest January performance in the port’s history.

Agricultural exports drove much of this surge:

- Sugar exports: 1.57 million tonnes (up 36.8% year-over-year)

- Soy complex: 1.56 million tonnes (surging 79.6%)

This agricultural boom creates dual demand: bulk storage facilities for raw commodities and sophisticated warehousing for value-added processing and packaging operations.

Vacancy Rates at Historic Lows

Modern logistics facilities within the Santos corridor currently maintain vacancy rates below 3%, with Class A properties in prime locations essentially achieving full occupancy. This tight market has pushed rental rates upward by 15-22% annually in select submarkets, creating exceptional opportunities for developers who can deliver quality product quickly.

The scarcity becomes even more pronounced for facilities offering:

- ✨ Automation-ready infrastructure with high clear heights (12+ meters)

- ✨ Multimodal access combining truck, rail, and port connectivity

- ✨ Sustainable certifications (LEED, AQUA-HQE) increasingly required by multinational tenants

- ✨ E-commerce specifications including cross-docking capabilities and last-mile positioning

Development Strategies for Capitalizing on the Logistics Warehousing Boom Near Port of Santos

Strategic warehouse development in the Santos region requires sophisticated understanding of infrastructure timing, site selection criteria, and tenant requirements. The Logistics Warehousing Boom Near Port of Santos: Development Strategies for 2026 E-Commerce Driven Demand rewards developers who align their projects with port expansion timelines and evolving supply chain needs.

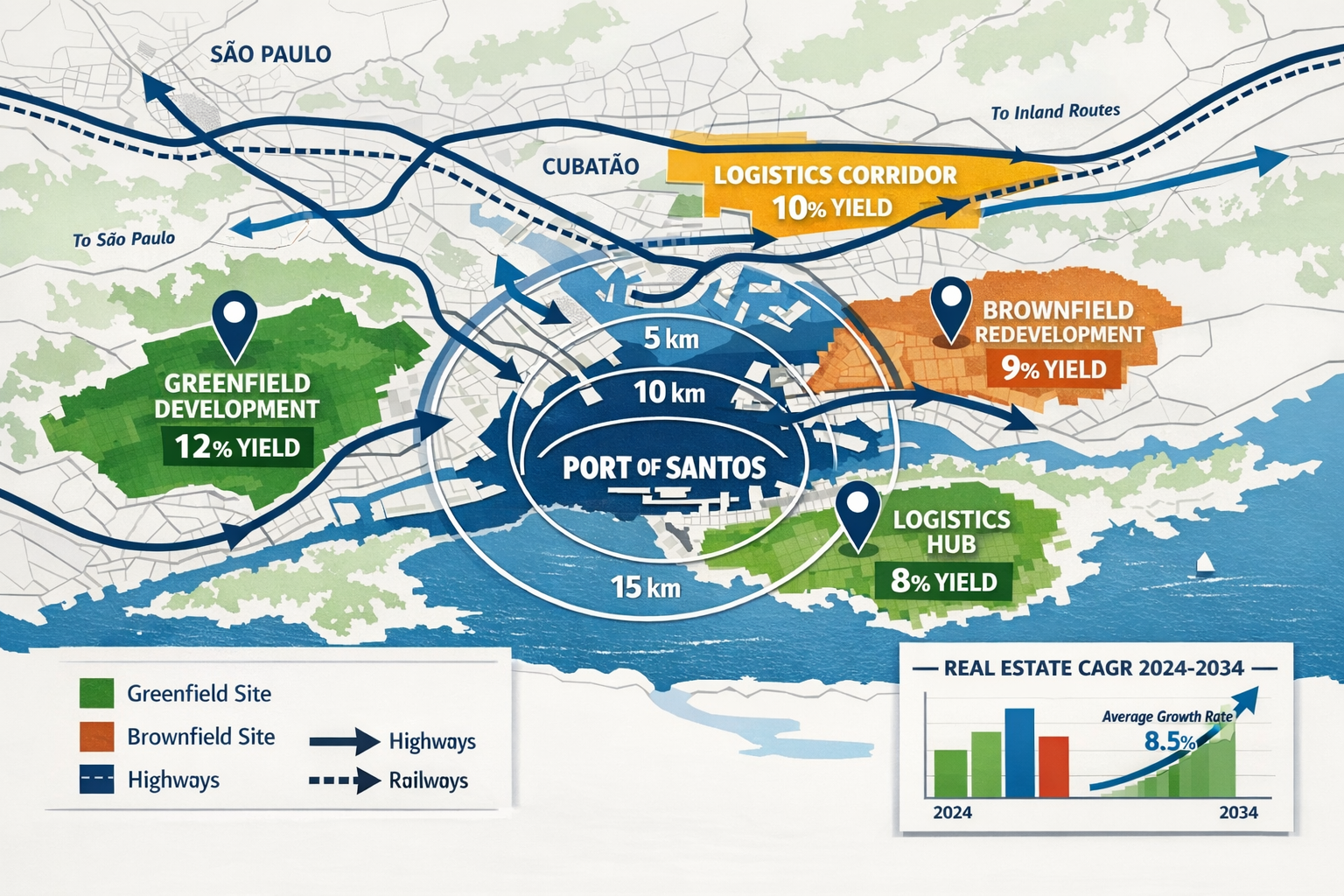

Site Selection: The Foundation of Success

Primary Logistics Corridors 🛣️

The most valuable warehouse locations cluster along specific corridors:

| Corridor Zone | Distance from Port | Primary Advantage | Typical Yield |

|---|---|---|---|

| Port-Adjacent | 0-5 km | Direct terminal access, container storage | 8-10% |

| Primary Ring | 5-15 km | Multimodal hubs, cross-docking | 9-12% |

| Secondary Ring | 15-30 km | E-commerce fulfillment, cost efficiency | 10-13% |

| Extended Zone | 30-50 km | Manufacturing support, bulk storage | 7-9% |

Infrastructure Proximity Factors:

- Highway Access: Properties within 2km of Rodovia dos Imigrantes (SP-160) or Via Anchieta (SP-150) command 20-30% rental premiums due to São Paulo metropolitan area connectivity

- Rail Connectivity: Sites with rail spur access serve agricultural exporters and bulk commodity handlers, reducing truck dependency

- Port Terminal Alignment: Proximity to specific terminals matters—facilities near DP World’s expanding container operations serve different tenants than those adjacent to bulk agricultural terminals

- Last-Mile Positioning: For e-commerce fulfillment, locations enabling 2-hour delivery to Greater São Paulo (population 22+ million) justify premium construction costs

Timing Development with Infrastructure Investments

The DP World $275 million expansion adds 190 meters of quay extension, with 150 meters dedicated to container operations targeting 1.7 million TEUs annual capacity by late 2026. Warehouse developments positioned to serve this expanded capacity should aim for delivery in Q3-Q4 2026 to capture initial tenant demand.

The STS-10 mega-terminal auction, while flexible in exact timing, represents the transformational infrastructure project. With over 10 potential bidders including ICTSI, JBS, JSL, COSCO, and Maersk expressing interest, the winning operator will require extensive supporting warehouse infrastructure. Developers securing land positions now can negotiate build-to-suit agreements with the eventual terminal operator.

Design Specifications for Modern Tenants

Today’s logistics tenants demand facilities far beyond basic warehouse shells:

Essential Features ⚙️:

- Clear heights: Minimum 12 meters, preferably 14-16 meters for high-density storage

- Floor loading capacity: 6+ tonnes per square meter

- Column spacing: 24m x 24m or larger for operational flexibility

- Dock doors: Ratio of 1 door per 1,000-1,500 sqm

- Trailer parking: 50+ spaces per 10,000 sqm of warehouse

- Power capacity: 150-200 kVA per 1,000 sqm for automation systems

Technology Integration 💻:

- Fiber optic infrastructure for warehouse management systems (WMS)

- EV charging stations for electric delivery fleets

- IoT sensor readiness for inventory tracking

- Solar panel installations reducing operational costs 15-25%

Sustainability Certifications: Multinational e-commerce and retail tenants increasingly require LEED Silver minimum certification, with Gold or Platinum commanding 8-12% rental premiums. Water recycling systems, LED lighting, and cool roof technologies provide both environmental benefits and operational cost reductions that justify higher rents.

Build-to-Suit vs. Speculative Development

The tight market conditions favor both approaches, but with different risk-return profiles:

Build-to-Suit Advantages:

- ✅ Pre-leased income certainty

- ✅ Tenant-specific customization commands premium rents

- ✅ Easier financing with committed tenant

- ✅ Reduced vacancy risk

Speculative Development Advantages:

- ✅ Higher ultimate rental rates (10-15% premium over BTS)

- ✅ Flexibility to capture market rent growth

- ✅ Faster delivery without tenant approval delays

- ✅ Multiple tenant options increasing negotiating leverage

In the current Santos market, speculative development of Class A facilities in prime corridors achieves full lease-up within 90-120 days of completion, making the vacancy risk minimal for well-positioned projects. This rapid absorption supports speculative strategies for developers with strong balance sheets.

Similar to how real estate development projects require careful timing and execution, logistics warehouse developments benefit from phased construction approaches that allow market testing and adjustment.

Investment Returns and Financial Strategies for 2026 E-Commerce Driven Demand

The financial performance of logistics warehousing near Port of Santos reflects the fundamental supply-demand imbalance and infrastructure-driven growth trajectory. Understanding the Logistics Warehousing Boom Near Port of Santos: Development Strategies for 2026 E-Commerce Driven Demand from an investment perspective reveals compelling risk-adjusted returns.

Projected Returns and Market Growth

Commercial Real Estate CAGR: The Santos logistics corridor forecasts a 3.63% compound annual growth rate through 2034, driven by sustained e-commerce expansion, agricultural export growth, and manufacturing nearshoring. This represents conservative baseline appreciation, with prime properties in strategic locations historically outperforming market averages by 150-200 basis points.

Rental Yield Analysis 💰:

Modern Class A warehouses in the Santos region currently generate:

- Gross rental yields: 8-12% annually

- Net operating income (NOI) yields: 6.5-9.5% after operating expenses

- Cap rates: Compressing from 9-10% (2024) to 7.5-8.5% (2026) as institutional capital flows increase

Development Profit Margins:

- Land acquisition: 8-12% of total project cost

- Construction costs: BRL 2,200-2,800 per sqm for Class A facilities

- Development profit: 18-25% on cost for well-executed projects

- Stabilized value creation: 30-40% above total development cost

Financing Strategies and Capital Structures

Debt Financing Options:

Brazilian commercial real estate debt markets offer several pathways:

- Traditional Bank Financing: 60-70% LTV, interest rates of CDI + 2.5-4.0%, requiring strong sponsor balance sheets

- CRI (Certificados de Recebíveis Imobiliários): Real estate receivables certificates enabling capital markets funding at competitive rates

- International Lenders: Dollar-denominated debt at 7-9% for projects with multinational tenants

- Development Finance: Construction facilities at 65-75% LTC (loan-to-cost) transitioning to permanent financing upon stabilization

Equity Structures:

Sophisticated developers employ varied equity approaches:

- Joint ventures with institutional partners (pension funds, insurance companies) providing 80-90% of equity for 70-80% ownership

- Fund structures aggregating multiple properties for diversification and liquidity

- REIT conversions upon portfolio stabilization for tax efficiency and public market access

The valuation appreciation potential mirrors dynamics seen in other Brazilian real estate sectors, where early-stage positioning in infrastructure-driven markets generates outsized returns.

Risk Mitigation and Tenant Diversification

Primary Risk Factors ⚠️:

- Port capacity constraints: Until STS-10 becomes operational, bottlenecks could limit throughput growth

- Economic cycles: Recession impacts e-commerce volumes and import/export activity

- Tenant concentration: Over-reliance on single tenant or industry sector

- Construction cost inflation: Material and labor costs increasing 12-18% annually

- Regulatory changes: Zoning, environmental, or tax policy shifts

Mitigation Strategies:

✔️ Multi-tenant design: Divisible floor plates enabling 3-5 tenant configurations ✔️ Lease structure: Longer terms (5-10 years) with CPI escalations and renewal options ✔️ Tenant mix: Balance between e-commerce (40%), third-party logistics (30%), and manufacturing/distribution (30%) ✔️ Insurance products: Political risk, construction completion, and revenue protection coverage ✔️ Phased development: Staged construction reducing capital exposure and enabling market response

Tax Optimization and Incentive Programs

Available Incentives 🎯:

Several programs enhance project economics:

- Municipal tax holidays: Many Santos-region municipalities offer 5-10 year IPTU (property tax) exemptions for qualifying logistics developments

- Environmental certifications: LEED-certified buildings qualify for accelerated depreciation schedules

- Job creation incentives: Warehouse operations generating 100+ jobs may receive state-level tax credits

- Free trade zone benefits: Specific customs-advantaged zones near the port offer duty deferrals

Depreciation Benefits:

Industrial buildings depreciate over 25 years (4% annually) for tax purposes, while specific warehouse equipment and automation systems qualify for accelerated schedules of 10-15 years, enhancing after-tax returns by 80-120 basis points.

Comparative Investment Analysis

How does Santos logistics warehousing compare to alternative Brazilian commercial real estate investments?

| Property Type | Avg. Yield | Vacancy Risk | Liquidity | Growth Potential |

|---|---|---|---|---|

| Santos Logistics Warehouse | 8-12% | Very Low | Medium | Very High |

| São Paulo Office | 6-8% | Medium | High | Medium |

| Rio Retail | 7-9% | Medium-High | Medium | Low-Medium |

| Industrial Manufacturing | 7-10% | Low-Medium | Low | Medium |

The Santos logistics sector offers superior yield with lower vacancy risk, though with somewhat reduced liquidity compared to core office markets. However, the growth potential significantly exceeds alternative sectors, making it attractive for investors with 5-10 year hold periods.

Those exploring diverse investment strategies in Brazilian real estate should consider logistics warehousing as a core allocation given the structural demand drivers and infrastructure catalysts.

Operational Excellence and Value-Add Strategies

Beyond initial development and leasing, maximizing returns from logistics warehousing requires ongoing operational excellence and strategic value enhancement. The most successful operators in the Santos corridor implement sophisticated management approaches that increase NOI and asset value over time.

Property Management Best Practices

Tenant Retention Focus 🤝:

With lease-up costs averaging 8-12% of annual rent (brokerage commissions, tenant improvements, downtime), retaining existing tenants dramatically improves returns. Leading operators achieve 80-90% renewal rates through:

- Proactive maintenance: Preventing disruptions to tenant operations

- Technology upgrades: Offering automation infrastructure improvements

- Flexible expansion: Providing adjacent space as tenant operations grow

- Service excellence: 24-hour response for critical issues

Operating Expense Management:

Modern warehouses incur operating expenses of 15-25% of gross rental income. Optimization strategies include:

- Energy management: Solar installations, LED retrofits, and smart HVAC reducing utility costs 20-30%

- Preventive maintenance: Scheduled programs preventing costly emergency repairs

- Security technology: Automated systems reducing personnel requirements

- Shared services: Aggregating multiple properties for purchasing power

Value-Add Repositioning Opportunities

The Santos region contains numerous older warehouse facilities ripe for value-add repositioning:

Acquisition Targets 🎯:

- Obsolete warehouses: Low clear-height (6-8m) facilities on well-located land

- Underutilized sites: Properties with 30-40% FAR (floor area ratio) utilization allowing expansion

- Functionally obsolete: Buildings lacking modern dock configurations or technology infrastructure

Repositioning Strategies:

- Demolition and rebuild: Replacing obsolete structures with modern Class A facilities

- Vertical expansion: Adding mezzanines or second levels where zoning permits

- Technology retrofits: Installing automation infrastructure, fiber optics, and power upgrades

- Sustainability improvements: LEED certification through green retrofits

Well-executed repositioning generates IRRs of 18-25%, significantly exceeding ground-up development returns while reducing construction risk and timeline.

Emerging Trends and Future-Proofing

Automation and Robotics 🤖:

The next generation of Santos warehouses will incorporate:

- Autonomous mobile robots (AMRs): Requiring wide aisles and smooth flooring

- Automated storage and retrieval systems (AS/RS): Demanding high clear heights and heavy power

- Conveyor networks: Necessitating structural support and routing flexibility

- Drone inventory systems: Requiring ceiling clearances and charging infrastructure

Designing for these technologies—even if not immediately implemented—preserves future optionality and tenant appeal.

Cold Chain and Specialized Storage:

Growing demand for temperature-controlled facilities serves:

- E-grocery fulfillment: Requiring multi-temperature zones

- Pharmaceutical logistics: Demanding precise climate control and security

- Agricultural exports: Needing refrigeration for perishables

Cold storage facilities command 20-35% rental premiums but require specialized construction and higher operating expertise.

Sustainability and ESG Requirements:

Institutional investors increasingly apply ESG (Environmental, Social, Governance) screens to real estate allocations. Leading practices include:

- Carbon neutrality: Solar power, electric vehicle fleets, renewable energy purchasing

- Water conservation: Rainwater harvesting, recycling systems

- Social impact: Local employment, community engagement, safety excellence

- Governance: Transparent reporting, stakeholder communication

Properties meeting rigorous ESG standards access lower-cost institutional capital and command valuation premiums of 5-10%.

For developers seeking to understand how market performance transforms real estate sectors, the Santos logistics market provides a compelling case study in infrastructure-driven transformation.

Navigating Regulatory and Competitive Landscapes

Success in the Santos logistics warehousing market requires sophisticated understanding of regulatory frameworks, competitive dynamics, and stakeholder relationships. The Logistics Warehousing Boom Near Port of Santos: Development Strategies for 2026 E-Commerce Driven Demand operates within complex legal and competitive environments that shape project feasibility and returns.

Zoning and Environmental Regulations

Municipal Zoning Requirements:

Santos and surrounding municipalities maintain specific industrial and logistics zoning designations:

- Minimum lot sizes: Typically 5,000-10,000 sqm for logistics facilities

- Setback requirements: 5-10 meters from property lines

- Height restrictions: Varying by zone, generally 15-20 meters maximum

- FAR (Floor Area Ratio): Usually 0.6-1.2 for industrial zones

- Parking ratios: 1 space per 100-150 sqm of warehouse area

Environmental Licensing:

All warehouse developments exceeding 10,000 sqm require environmental impact assessments and licensing:

- EIA/RIMA: Environmental Impact Study for projects over 50,000 sqm

- Water management: Stormwater retention and treatment systems

- Vegetation preservation: Maintaining required green space percentages

- Noise mitigation: Especially for 24-hour operations near residential areas

Processing times for environmental approvals range from 6-18 months, making early engagement with environmental agencies critical to project timelines.

Competitive Landscape Analysis

Major Players and Market Share:

The Santos logistics real estate market includes several dominant developers and operators:

- International REITs and Funds: Blackstone, Prologis, GLP controlling 30-35% of Class A inventory

- Brazilian Developers: Log Commercial Properties, Cyrela Commercial Properties with 20-25% share

- Private Developers: Regional players and family offices holding 25-30%

- Owner-Occupiers: Manufacturers and retailers owning dedicated facilities representing 15-20%

Competitive Advantages:

Successful developers differentiate through:

- Land banking: Securing prime sites ahead of infrastructure announcements

- Tenant relationships: Pre-existing connections with major e-commerce and logistics operators

- Construction efficiency: Proven ability to deliver on time and budget

- Capital access: Relationships with institutional equity and debt providers

- Operational expertise: In-house property management capabilities

Strategic Partnerships and Stakeholder Engagement

Port Authority Relationships ⚓:

Maintaining strong connections with Santos Port Authority (SPA) provides:

- Infrastructure timing intelligence: Advance notice of expansion schedules

- Tenant referrals: Port users seeking nearby warehousing

- Regulatory navigation: Assistance with permits and approvals

- Marketing collaboration: Joint promotion of Santos logistics ecosystem

Government Engagement:

Productive relationships with municipal and state officials facilitate:

- Incentive negotiations: Tax holidays and development subsidies

- Infrastructure coordination: Road improvements and utility extensions

- Expedited approvals: Faster permitting and licensing processes

- Public-private partnerships: Collaborative infrastructure projects

Industry Associations:

Active participation in logistics and real estate associations provides market intelligence, networking opportunities, and policy advocacy platforms. Key organizations include ABRALOG (Brazilian Logistics Association) and SECOVI-SP (Real Estate Union).

For those interested in exploring broader real estate opportunities in Brazil, understanding the Santos logistics market provides valuable insights into infrastructure-driven development strategies applicable across sectors.

Conclusion: Seizing the Santos Logistics Warehousing Opportunity

The Logistics Warehousing Boom Near Port of Santos: Development Strategies for 2026 E-Commerce Driven Demand represents a generational opportunity for informed developers and investors. With record port throughput of 12.7 million tonnes in January 2026, over $1.5 billion in infrastructure investments underway, and vacancy rates below 3%, the fundamental supply-demand dynamics strongly favor new development.

Key Success Factors

Capturing superior returns in this market requires:

🎯 Strategic Site Selection: Prioritizing locations within 15km of port terminals with multimodal transportation access and last-mile delivery capabilities

🎯 Infrastructure Timing: Aligning project delivery with the DP World expansion completion (late 2026) and STS-10 terminal operational timeline (2027-2028)

🎯 Modern Design Standards: Delivering Class A facilities with 12+ meter clear heights, automation-ready infrastructure, and sustainability certifications

🎯 Tenant Diversification: Balancing e-commerce fulfillment, third-party logistics, and manufacturing tenants to reduce concentration risk

🎯 Financial Optimization: Employing appropriate capital structures, capturing available incentives, and implementing tax-efficient ownership vehicles

🎯 Operational Excellence: Maintaining high tenant retention through proactive management and continuous value enhancement

Market Outlook Through 2034

The Santos logistics corridor is projected to sustain strong performance through the next decade, driven by:

- E-commerce growth: Brazilian online retail expanding 15-20% annually

- Agricultural exports: Continued strength in soy, sugar, and protein exports

- Manufacturing nearshoring: Global supply chain restructuring favoring Latin American production

- Infrastructure capacity: Port expansions enabling throughput growth to 9-10 million TEUs annually

- Urbanization: Greater São Paulo’s growing population requiring sophisticated distribution networks

The forecasted 3.63% commercial CAGR through 2034 represents conservative baseline appreciation, with prime properties likely outperforming by significant margins as institutional capital increasingly targets the sector.

Actionable Next Steps

For developers and investors ready to capitalize on this opportunity:

Immediate Actions (Next 30-60 Days):

- Conduct site reconnaissance: Identify available land parcels in prime corridors

- Engage local advisors: Establish relationships with brokers, attorneys, and consultants

- Assess capital sources: Determine optimal financing structures for your investment profile

- Analyze competitive supply: Understand pipeline projects and absorption rates

Near-Term Actions (Next 3-6 Months):

- Secure land positions: Execute purchase agreements or options on strategic sites

- Initiate due diligence: Environmental assessments, zoning confirmation, title review

- Develop tenant pipeline: Begin marketing to potential build-to-suit candidates

- Finalize capital structure: Close equity commitments and arrange construction financing

Medium-Term Actions (6-18 Months):

- Obtain approvals: Complete environmental licensing and building permits

- Execute construction: Begin development with target completion aligned to infrastructure timing

- Pre-lease space: Secure anchor tenants prior to completion

- Implement operations: Establish property management and tenant services

The convergence of record port performance, massive infrastructure investment, and e-commerce-driven demand has created ideal conditions for logistics warehouse development near Port of Santos. Developers who act decisively with informed strategies will capture exceptional risk-adjusted returns in this transforming market.

For those seeking to explore this opportunity further or discuss specific development strategies, connecting with experienced real estate professionals can provide valuable market insights and partnership opportunities.

The Logistics Warehousing Boom Near Port of Santos: Development Strategies for 2026 E-Commerce Driven Demand is not merely a short-term trend—it represents a fundamental restructuring of Brazil’s logistics infrastructure that will create value for decades to come. The question is not whether to participate, but how to position for maximum advantage in this exceptional market.