Commercial real estate transactions reached $115 billion in Q2 2025, marking a 3.8% year-over-year increase—but the real story lies in where that capital is flowing.[1] While traditional gateway cities face mounting constraints, secondary inland markets are capturing unprecedented developer attention as structural shifts reshape Brazil’s real estate landscape. The Secondary City Surges 2026: Developer Playbooks for Inland Growth Beyond Metros phenomenon represents more than a temporary trend; it signals a fundamental reordering of investment priorities driven by affordability crises, infrastructure expansion, and changing buyer preferences.

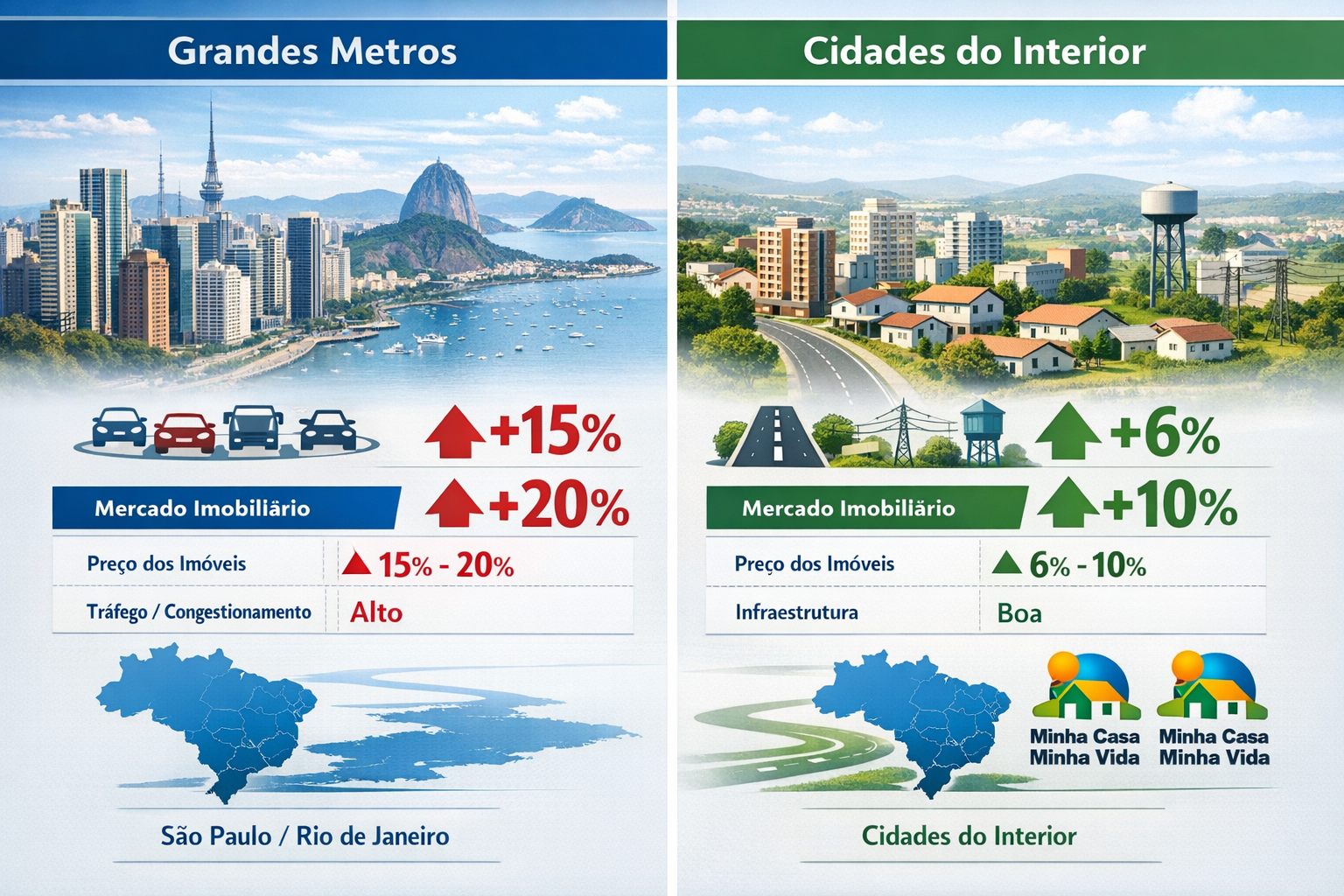

For developers willing to look beyond established metros, secondary cities now offer compelling advantages: annual price appreciation of 6-10%, supply gaps in mid-range housing, and government-backed infrastructure programs creating tangible demand. This article unpacks the strategic playbooks developers are deploying to capitalize on inland growth opportunities in 2026.

Key Takeaways

- Secondary markets deliver 6-10% annual price growth with lower entry costs and reduced competition compared to saturated metro markets

- Infrastructure investments and MCMV expansions are creating structural demand for mid-range condos in inland cities

- Gateway city constraints—including high costs, land scarcity, and complex permitting—are accelerating capital migration to secondary hubs

- Successful developers focus on lifestyle amenities such as outdoor space, larger units, and community features that secondary cities can deliver more affordably

- Strategic market selection criteria include power grid reliability, efficient permitting processes, favorable tax policies, and employment diversification

Understanding the Secondary City Surge in 2026

Why Capital Is Migrating Inland

The migration of development capital from coastal metros to secondary inland cities stems from multiple converging forces. Over the past five years, U.S. rents jumped 30.4% while wages rose only 20.2%, with similar patterns emerging in Brazilian markets.[2] This rent-to-wage gap has made homeownership increasingly unattainable in traditional hubs, pushing both buyers and developers toward more affordable alternatives.

Gateway cities face hard constraints that no amount of capital can easily overcome:

- Land scarcity: Prime development sites in São Paulo, Rio de Janeiro, and other major metros command premium prices with limited availability

- Permitting complexity: Bureaucratic processes in established metros can extend timelines by 12-18 months

- Infrastructure saturation: Power grids, water systems, and transportation networks in core markets operate at or near capacity[1]

- Cost escalation: Construction and labor costs in metros have risen 25-35% since 2020

Secondary cities, by contrast, offer wider cap rate spreads and higher risk-adjusted returns, though developers must account for higher liquidity risk.[1] The best places to invest in Brazil property increasingly include mid-sized markets with strong fundamentals rather than only traditional hotspots.

The MCMV Factor: Government-Backed Demand

Brazil’s Minha Casa Minha Vida (MCMV) program expansions have created structural demand in secondary markets. These government-backed initiatives provide:

✅ Subsidized financing for middle-income buyers

✅ Reduced developer risk through pre-qualified buyer pools

✅ Infrastructure co-investment in targeted growth corridors

✅ Regulatory streamlining for qualifying projects

The program’s focus on inland expansion means developers who align projects with MCMV criteria gain access to a ready market of creditworthy buyers. This government support reduces absorption risk—a critical factor when entering less-proven markets.

Buyer Preference Shifts Favoring Secondary Markets

National Association of REALTORS data reveals fundamental changes in buyer priorities:[2]

| Buyer Priority | Percentage Seeking | Availability in Secondary Cities |

|---|---|---|

| Outdoor space | 42% | ⭐⭐⭐⭐⭐ High |

| Larger homes | 31% | ⭐⭐⭐⭐ High |

| Quieter environments | 24% | ⭐⭐⭐⭐⭐ Very High |

| Walkable neighborhoods | 28% | ⭐⭐⭐ Moderate |

| Lower cost of living | 38% | ⭐⭐⭐⭐⭐ Very High |

Secondary cities can deliver these amenities at price points 30-50% below metro equivalents, creating natural competitive advantages for developers who design projects around these preferences.

Developer Playbooks for Secondary City Success

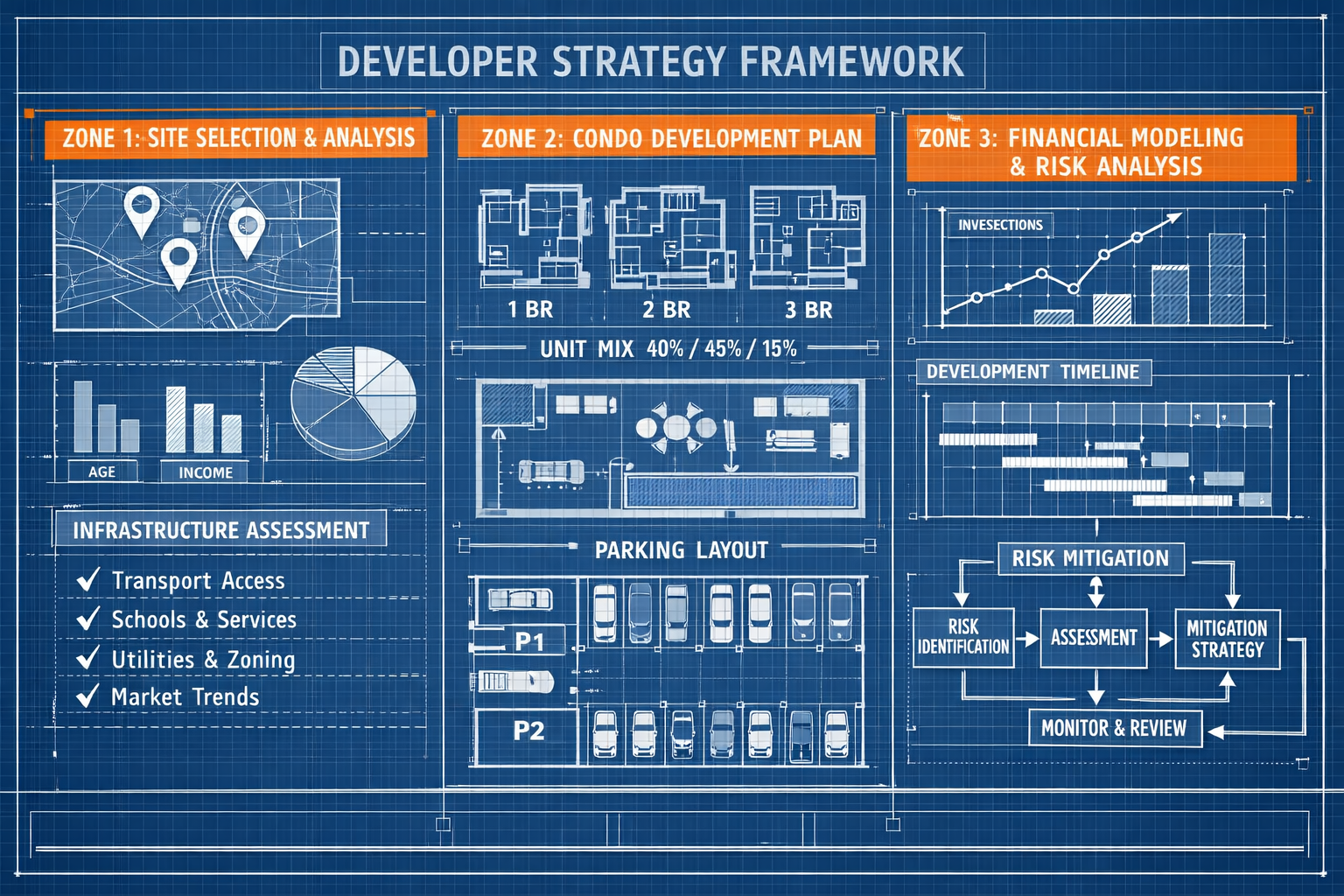

Market Selection: Identifying High-Potential Secondary Cities

Not all secondary markets offer equal opportunity. Successful developers apply rigorous selection criteria before committing capital:

Infrastructure Backbone Assessment 🏗️

Markets offering reliable power grids, efficient permitting, and favorable tax policies draw the most institutional attention, while markets lacking infrastructure backbones fall behind.[1] Developers should evaluate:

- Electrical capacity and grid reliability (critical for residential and commercial projects)

- Water and sewage system capacity for population growth

- Transportation connectivity (highways, airports, public transit plans)

- Digital infrastructure (fiber optic availability, 5G deployment)

Employment Diversification Analysis 💼

Single-industry towns carry concentration risk. The strongest secondary markets feature multiple employment sectors. Consider these successful models:

- Columbus, Ohio: Intel’s $20 billion semiconductor factory investment is attracting talent and tech firms, positioning the city as a Midwestern hub blending big-city ambition with accessibility.[2]

- Raleigh, North Carolina: The Research Triangle functions as a talent magnet for students, scientists, and tech innovators seeking city energy without coastal-hub frenzy.[2][3]

- Nashville, Tennessee: Music/entertainment industry coupled with growing healthcare sector creates dual-sector stability.[3]

Brazilian equivalents might include cities with combinations of agribusiness, manufacturing, education, and tourism sectors rather than dependence on a single economic driver.

Population and Migration Trends 📊

Analyze five-year population growth rates, net migration patterns, and demographic composition. Markets attracting young families and skilled professionals offer the strongest residential demand. Cities experiencing brain drain or population decline should be avoided regardless of other positive factors.

Product Design: What to Build in Secondary Markets

The Secondary City Surges 2026: Developer Playbooks for Inland Growth Beyond Metros emphasizes mid-range condo development as the sweet spot for inland markets. Here’s why:

The Mid-Range Sweet Spot

Secondary cities face acute supply gaps in the R$300,000-R$600,000 price range (approximately $60,000-$120,000 USD). This segment captures:

- First-time homebuyers utilizing MCMV financing

- Young professionals relocating from metros

- Investors seeking rental income properties

- Downsizing empty-nesters seeking maintenance-free living

Unit Mix Strategy

Optimal unit mixes for secondary markets differ from metro projects:

- 40-50% two-bedroom units (65-80 m²): Core product for young families and professionals

- 25-30% one-bedroom plus units (50-60 m²): Captures singles and couples

- 15-20% three-bedroom units (85-100 m²): Serves larger families and premium buyers

- 5-10% studio units (35-45 m²): Investor-focused rental products

This contrasts with metro markets where studios and one-bedrooms often dominate. Secondary city buyers prioritize space and value over location prestige.

Amenity Packages That Differentiate

In markets where land costs remain reasonable, developers can include amenities that would be cost-prohibitive in metros:

🏊 Outdoor recreation: Pools, sports courts, green spaces (42% of buyers prioritize outdoor space)[2]

🏋️ Fitness and wellness: Gyms, yoga studios, walking trails

👨👩👧👦 Family-focused: Playgrounds, party rooms, coworking spaces

🔒 Security: Gated access, surveillance, on-site management

🌳 Sustainability: Solar panels, rainwater collection, bike storage

These amenities justify price premiums while remaining affordable due to lower land costs. The growth of regions like Ingleses in Florianópolis demonstrates how quality-of-life features drive valuation in secondary markets.

Financial Modeling: Making the Numbers Work

Revenue Assumptions

Secondary markets typically deliver:

- 6-10% annual price appreciation (versus 3-5% in mature metros)

- 12-18 month absorption periods for well-located projects

- 15-25% pre-sale requirements before construction financing approval

- Lower price per square meter but higher percentage margins

Cost Advantages

Developers benefit from:

| Cost Category | Metro Market | Secondary Market | Savings |

|---|---|---|---|

| Land acquisition | R$2,500-4,000/m² | R$800-1,500/m² | 60-70% |

| Construction labor | R$1,200-1,500/m² | R$900-1,100/m² | 25-35% |

| Permitting timeline | 18-24 months | 8-12 months | 40-50% |

| Marketing costs | 6-8% of sales | 4-6% of sales | 25-35% |

These cost advantages enable competitive pricing while maintaining healthy margins. Projects that would be marginal in metros become highly profitable in secondary markets.

Risk Mitigation Strategies

Smart developers implement multiple risk controls:

✓ Phased development: Start with smaller initial phases to test market absorption

✓ Pre-sale thresholds: Require 20-30% pre-sales before breaking ground

✓ Local partnerships: Joint ventures with established local developers reduce execution risk

✓ Exit flexibility: Design projects that can pivot to rental if sales slow

✓ Conservative underwriting: Model 15-20% longer absorption than projections suggest

The advantages of investing in studios in Florianópolis illustrate how specific product types can reduce risk in secondary markets.

Operational Excellence in Secondary Markets

Local Market Intelligence

National developers entering secondary markets must invest in local market intelligence:

Ground-Level Research

- Meet with local real estate brokers and property managers

- Interview recent buyers about decision factors

- Survey competing projects for pricing, features, and absorption rates

- Engage with municipal planning departments about infrastructure plans

- Connect with major employers about expansion or relocation plans

Competitive Positioning

Secondary markets often feature less sophisticated competition. Developers bringing metro-market professionalism—quality construction, professional marketing, transparent sales processes—gain immediate advantages.

Construction and Timeline Management

Contractor Selection

Local contractors may lack experience with modern mid-rise construction. Consider:

- Bringing experienced project managers from metro markets

- Partnering with regional contractors who have multi-city experience

- Investing in contractor training and quality control systems

- Building contingency budgets for learning-curve inefficiencies

Accelerated Timelines

Streamlined permitting in secondary markets enables faster project delivery:

- 8-12 month permitting (versus 18-24 months in metros)

- 14-18 month construction for mid-rise projects

- Total development cycle: 24-30 months from land acquisition to delivery

Faster cycles reduce carrying costs and interest expense while enabling quicker capital recycling. The accelerated pace of projects like Tramonto demonstrates execution advantages in well-managed markets.

Marketing and Sales Strategy

Digital-First Approach

Secondary market buyers increasingly research online before visiting sales centers:

📱 Virtual tours: 3D walkthroughs and drone footage

💻 Social media targeting: Facebook and Instagram ads geo-targeted to metro areas

📧 Email nurture campaigns: Educational content about secondary city lifestyle benefits

🎥 Video testimonials: Feature early buyers explaining their decision rationale

Metro Market Outreach

Many secondary city buyers currently live in metros. Effective strategies include:

- Roadshow events in major metros showcasing projects

- Partnership with metro-based brokers offering referral commissions

- Comparative cost-of-living calculators demonstrating savings

- Remote purchasing processes enabling metro buyers to transact digitally

The real estate market performance in Florianópolis shows how professional marketing drives results in secondary markets.

Post-Delivery Value Creation

Property Management Excellence

Quality property management protects asset values and supports resale:

- Professional on-site management teams

- Proactive maintenance programs

- Community-building events and communications

- Responsive owner and tenant service

Resale Market Development

Developers benefit from supporting robust resale markets:

- Maintain relationships with local brokers

- Provide market data and comps to support valuations

- Offer financing assistance programs for resale buyers

- Host periodic community events that maintain project visibility

Strong resale markets validate initial buyer decisions and support future project sales. The appreciation potential for pre-construction buyers demonstrates the importance of long-term value creation.

Emerging Secondary Markets to Watch in 2026

Brazilian Secondary City Opportunities

While much of the research focuses on U.S. markets, Brazilian developers can apply similar frameworks to identify opportunities:

Interior São Paulo State

Cities like Campinas, São José dos Campos, and Ribeirão Preto offer:

- Strong employment bases (technology, manufacturing, education)

- Excellent highway connectivity to São Paulo capital

- Growing populations of young professionals

- Significant supply gaps in mid-range housing

Southern Region Expansion

Beyond established markets like Florianópolis, cities including Joinville, Blumenau, and Caxias do Sul present opportunities:

- High quality-of-life indicators

- Diversified industrial bases

- Strong German and Italian cultural heritage attracting tourism

- Lower crime rates than major metros

The Florianópolis real estate market outlook provides insights applicable to similar secondary markets throughout Brazil.

Central-West Agribusiness Hubs

Cities serving Brazil’s agricultural heartland—including Uberlândia, Dourados, and Sinop—benefit from:

- Agribusiness wealth creation

- Infrastructure investments in transportation and logistics

- Growing middle-class populations

- Minimal existing mid-rise housing supply

International Parallels

The Secondary City Surges 2026: Developer Playbooks for Inland Growth Beyond Metros phenomenon extends globally:

Austin, Texas maintains investment appeal through job market strength in tech, healthcare, and advanced manufacturing, allowing wages to pace with rising real estate costs.[2][3]

Boise, Idaho combines outdoorsy culture, lower cost of living, downtown revitalization, and easy outdoor access—attracting young families and offering solid rental returns.[2]

Phoenix and Dallas are drawing industrial and data center developers facing power and land scarcity in core markets.[1]

These international examples validate the structural drivers behind secondary city growth and provide benchmarks for Brazilian developers.

Risk Factors and Mitigation Strategies

Market-Specific Risks

Liquidity Constraints 💧

Secondary markets feature thinner transaction volumes, making exits more challenging. Mitigation strategies:

- Build longer hold periods into financial models (5-7 years versus 3-5 years)

- Develop rental operations capabilities as alternative to sale exits

- Maintain relationships with regional and national institutional buyers

- Create portfolio scale across multiple secondary markets to attract larger buyers

Economic Concentration 🏭

Cities dependent on single industries face recession vulnerability. Due diligence should include:

- Stress-testing employment scenarios if major employer reduces presence

- Analyzing historical resilience during past economic cycles

- Evaluating municipal fiscal health and debt levels

- Assessing diversification initiatives by local economic development agencies

Infrastructure Execution Risk 🚧

Promised infrastructure improvements may face delays or cancellations. Protect downside by:

- Underwriting projects assuming current infrastructure only

- Treating planned improvements as upside rather than base case

- Negotiating developer agreements with municipalities for infrastructure commitments

- Selecting sites with existing infrastructure rather than depending on future improvements

Regulatory and Political Risks

Zoning Changes

Secondary markets may lack sophisticated zoning frameworks, creating uncertainty. Strategies include:

- Engaging early with planning departments to understand long-term vision

- Advocating for clear, predictable zoning codes

- Securing development approvals with vesting rights before major capital commitments

- Building relationships with local political leadership

MCMV Program Changes

Government housing programs can shift with political changes. Reduce dependency by:

- Designing projects that work with or without MCMV subsidies

- Diversifying buyer segments beyond MCMV-eligible purchasers

- Maintaining flexibility to adjust unit mixes and pricing

- Monitoring federal housing policy developments closely

Conclusion

The Secondary City Surges 2026: Developer Playbooks for Inland Growth Beyond Metros represents a structural shift rather than a cyclical trend. Gateway city constraints—high costs, land scarcity, infrastructure saturation—are pushing capital and residents toward inland alternatives offering better value propositions. With secondary markets delivering 6-10% annual appreciation, government programs creating structural demand, and buyer preferences shifting toward space and affordability, developers who master secondary city execution will capture outsized returns.

Success requires adapting metro-market sophistication to secondary-market realities: rigorous market selection focusing on infrastructure and employment diversification, product designs emphasizing mid-range condos with lifestyle amenities, conservative financial modeling with appropriate risk controls, and operational excellence in construction, marketing, and property management.

Actionable Next Steps

For Developers Ready to Enter Secondary Markets:

- Conduct market screening using the criteria outlined above—infrastructure, employment diversity, migration trends, and competitive landscape

- Visit target markets for ground-level research including broker interviews, competitor analysis, and municipal engagement

- Build local partnerships through joint ventures with established regional developers who understand market nuances

- Start small with pilot projects that test market assumptions before scaling capital commitments

- Invest in marketing that reaches metro-area buyers considering relocation to secondary cities

For Investors Evaluating Secondary Market Opportunities:

- Assess developer track records in secondary markets specifically, not just metro-market success

- Evaluate market fundamentals independently rather than relying solely on developer projections

- Understand exit strategies and liquidity constraints inherent in secondary markets

- Diversify across multiple secondary markets rather than concentrating in single cities

- Monitor infrastructure delivery and economic development initiatives that support long-term growth

The developers who move decisively into high-potential secondary markets in 2026 will establish competitive advantages that compound over the next decade. The opportunity is substantial, the playbooks are proven, and the structural drivers are accelerating. The question is not whether secondary cities will surge—it’s whether your development strategy will capture the growth.

Explore more about strategic real estate development opportunities and stay informed about market trends and insights to position your portfolio for success in this transformative period.

References

[1] The Rise Of Secondary Cre Markets In 2026 Why Investors Are Looking Beyond The Core – https://www.cbcworldwide.com/blog/the-rise-of-secondary-cre-markets-in-2026-why-investors-are-looking-beyond-the-core

[2] Next Booming Us Cities 2026 Real Estate – https://www.housebeautiful.com/design-inspiration/real-estate/a70178384/next-booming-us-cities-2026-real-estate/

[3] 10 Real Estate Markets Poised To Surge In 2026 – https://goliathdata.com/10-real-estate-markets-poised-to-surge-in-2026