Brazil’s residential real estate market is undergoing a quiet but powerful geographic redistribution. While São Paulo still commands 24.16% of total national real estate activity [1], a new wave of demand is sweeping through smaller inland markets — cities that were largely invisible to institutional developers just five years ago. The Secondary Cities Surge 2026: MCMV and Infrastructure Driving Inland Development Beyond São Paulo and Rio is not a prediction anymore. It is happening now, fueled by two structural forces: the Minha Casa Minha Vida (MCMV) program’s accelerating push into Northeast interiors and São Paulo’s periphery, and the Novo PAC’s infrastructure investments connecting previously isolated municipalities to economic corridors. The result? Price growth of 6–10% in secondary markets that are attracting developers hungry for margins that saturated metros can no longer offer.

Key Takeaways 📌

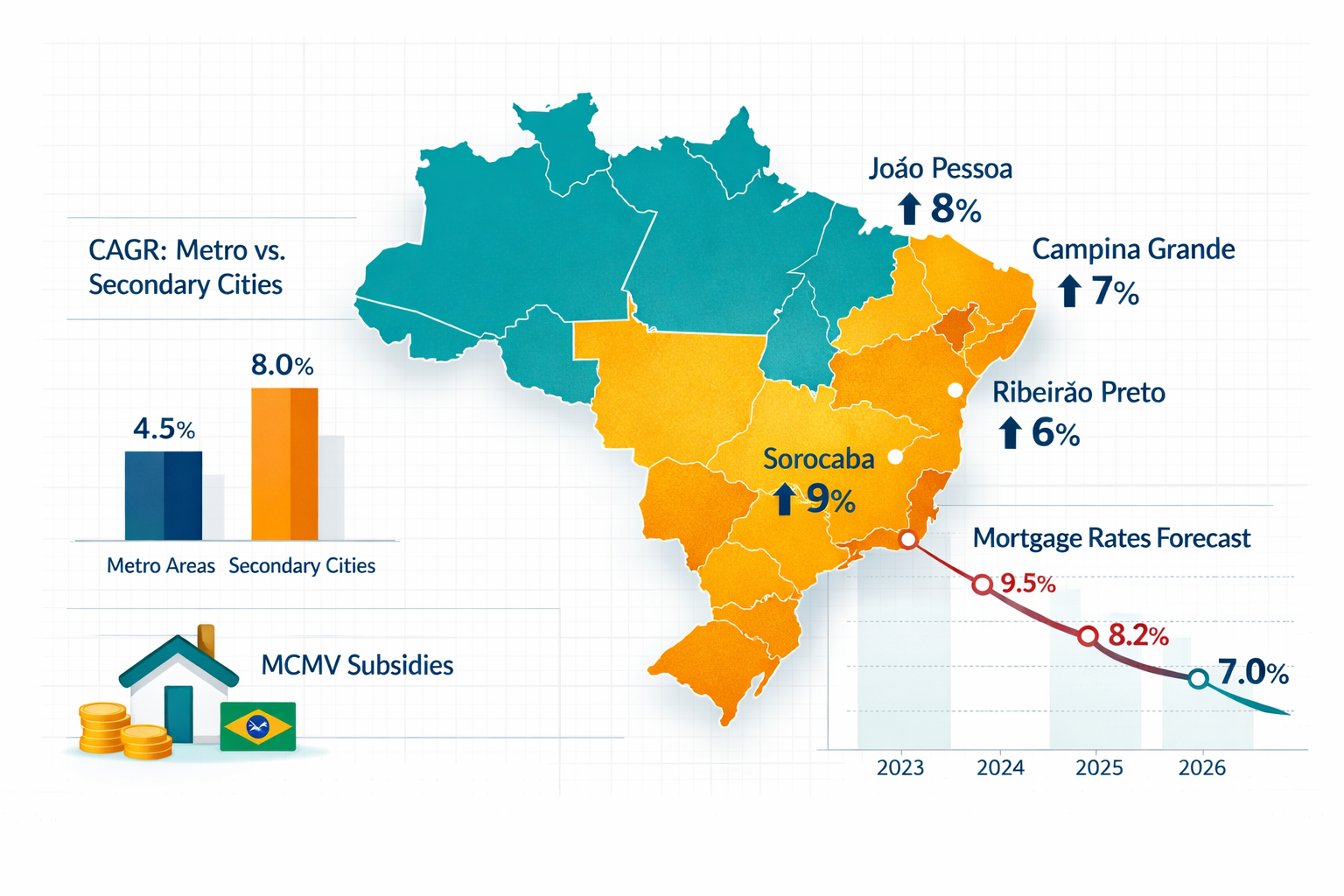

- MCMV mortgage subsidies are projected to add approximately 2.1% to national CAGR forecasts, with the Northeast and São Paulo outskirts as primary beneficiaries [1].

- Secondary cities like João Pessoa are gaining momentum through targeted concessions and zoning reforms that enable vertical densification [1].

- Apartments and condominiums dominate new supply, accounting for 77.17% of 2025 activity — a format perfectly suited to secondary city land economics [1].

- Infrastructure investment through Novo PAC is unlocking land value in inland corridors, creating first-mover advantages for developers willing to enter early.

- Investors who understand the best places to invest in Brazil property are already repositioning capital away from overpriced metro cores.

The MCMV Engine: How Subsidized Mortgages Are Reshaping Brazil’s Interior

The Minha Casa Minha Vida program has always been a demand-side tool. But in 2026, it has evolved into something more powerful: a geographic equalizer. By extending accelerated mortgage subsidies into markets where baseline affordability is tightest — particularly in the Northeast — the program is creating viable demand in cities that previously lacked the mortgage origination infrastructure to support developer launches.

💬 “Accelerated Mortgage Subsidies under MCMV are projected to add approximately 2.1% impact on CAGR forecasts, with particular strength in São Paulo and the Northeast over a medium-term horizon.” [1]

This is a critical shift. In the past, MCMV launches were concentrated in São Paulo’s periphery and major state capitals because that is where the demand base was large enough to justify the fixed costs of a launch. Now, with targeted concessions in the Northeast expanding financial inclusion, cities like João Pessoa, Campina Grande, and Feira de Santana are appearing on developer radars for the first time.

Why Secondary Cities Are Winning the Affordability Battle

The economics are straightforward. Land costs in secondary cities are a fraction of São Paulo or Rio de Janeiro prices. Labor costs are lower. And with MCMV subsidies reducing the effective mortgage rate for qualifying buyers, the gap between what families can afford and what developers need to charge to turn a profit narrows dramatically.

Here is a simplified comparison of the developer margin environment:

| Market Type | Land Cost Index | MCMV Subsidy Access | Margin Potential |

|---|---|---|---|

| São Paulo Core | Very High | Moderate | Compressed |

| Rio de Janeiro | High | Moderate | Moderate |

| Northeast Secondary Cities | Low | High | Elevated |

| São Paulo Outskirts | Moderate | High | Strong |

Developers with industrialized building systems have been particularly well-positioned to capitalize on this dynamic. By standardizing construction processes, they can defend margins even when input costs rise — a critical advantage in markets where price points are constrained by MCMV eligibility thresholds [1].

For developers and investors tracking real estate market trends in Florianópolis and greater Brazil, the MCMV expansion into secondary cities represents a structural shift that will reshape capital allocation for years.

The Compact Unit Formula

Secondary cities are not just absorbing MCMV demand through large family units. The compact studio and two-bedroom format that proved successful in São Paulo’s transit corridors is being adapted for secondary city contexts [1]. In inland markets, the driver is not transit proximity — it is price-per-square-meter accessibility. Younger families and first-time buyers in cities like João Pessoa are demonstrating strong absorption of compact units priced within MCMV eligibility bands, signaling that the format translates well beyond the megacity context.

Novo PAC and Zoning Reform: Infrastructure as the Multiplier

If MCMV is the demand engine, Novo PAC is the land value multiplier. Brazil’s infrastructure investment program is directing capital into roads, sanitation, urban mobility, and digital connectivity in exactly the secondary cities where MCMV demand is building. The combination is creating a compounding effect that developers in saturated metros rarely encounter anymore.

Urban zoning reform enabling vertical residential densification is projected to contribute approximately 0.9% to CAGR forecasts, with long-term effects visible particularly in São Paulo transit corridors and João Pessoa [1]. While 0.9% may sound modest, it compounds powerfully when layered on top of MCMV subsidy effects, infrastructure-driven land appreciation, and the base growth trajectory of markets that are starting from a lower price floor.

The Infrastructure-Development Feedback Loop

The mechanism works like this:

- 🏗️ Novo PAC funds a road, bridge, or sanitation upgrade in or near a secondary city

- 📈 Land values in adjacent areas rise as connectivity and livability improve

- 🏢 Developers launch MCMV-aligned projects on newly viable land

- 👨👩👧 Families move in, creating demand for retail, schools, and services

- 🔄 The city’s economic base expands, justifying further infrastructure investment

This feedback loop is already visible in northeastern markets. João Pessoa, for example, has been explicitly identified as a market where both zoning reform and MCMV concessions are aligning to create a development-ready environment [1]. The city’s combination of relatively low land costs, growing population, and improving connectivity makes it a textbook case for the secondary cities surge thesis.

Rate Cuts Accelerating the Timeline ⚡

The broader macroeconomic context matters too. As interest rate cuts feed through in 2026, metros with ready pipelines and clear policy alignment are expected to lead acceleration in both primary and secondary channels [1]. Secondary cities that have already built MCMV-aligned supply pipelines are positioned to capture disproportionate demand as mortgage affordability improves. The cities that acted early — where developers launched before the rate cycle turned — will see the strongest price appreciation.

This is the window that sophisticated developers and investors are currently navigating. Those who understand the value of buying property off-plan recognize that entering a secondary market during the infrastructure build-out phase — before rate cuts fully materialize — is where outsized returns are generated.

Secondary Cities Surge 2026: Market Data, Opportunities, and Developer Strategies

Understanding the Secondary Cities Surge 2026: MCMV and Infrastructure Driving Inland Development Beyond São Paulo and Rio requires looking at both the macro data and the on-the-ground realities of specific markets. The numbers tell a compelling story.

The São Paulo Paradox

São Paulo remains Brazil’s dominant real estate market by volume — 24.16% of national activity in 2025 [1]. But dominance does not mean opportunity. The city’s mature districts are characterized by compressed developer margins, high land acquisition costs, and intense competition for a relatively stable pool of qualified buyers. Secondary transactions (resales) commanded 68.9% of total sales in 2025 nationally [1], and in São Paulo’s core, this figure is even higher — reflecting a market where new supply struggles to compete with existing stock on price.

The São Paulo outskirts tell a different story. Municipalities at the edge of the metropolitan region — where MCMV eligibility rates are higher, land is cheaper, and infrastructure investment is actively improving connectivity — are functioning more like secondary cities than metro extensions. Developers who understand this distinction are finding stronger absorption rates and better margin profiles in outer São Paulo than in the city’s traditional launch corridors.

Rio de Janeiro’s Repositioning

Rio de Janeiro presents a different opportunity. The city is projected to grow at a faster CAGR of 6.88% through 2031 compared to São Paulo, driven by product repositioning and retrofit economics [1]. This is not a secondary city story per se, but it illustrates a broader principle: markets that were previously overlooked or undervalued by institutional capital can generate superior returns precisely because the starting price base is lower.

For investors already tracking opportunities in Brazil’s high-return property locations, Rio’s trajectory reinforces the thesis that geographic diversification beyond São Paulo’s core is not just viable — it is increasingly necessary for competitive returns.

The Apartment Format Advantage 🏢

One structural factor that benefits secondary city development is the dominance of the apartment format. Apartments and condominiums accounted for 77.17% of 2025 activity nationally [1]. This format is ideally suited to secondary city economics for several reasons:

- Land efficiency: Vertical development maximizes return per square meter of land

- MCMV compatibility: Apartment units are the standard format for MCMV launches

- Community infrastructure: Condominium amenities increase perceived value without proportional cost increases

- Absorption speed: Compact apartment units in MCMV price bands absorb faster than horizontal housing in most secondary markets

Developers who have standardized around the apartment format — particularly those using industrialized construction systems — can replicate successful São Paulo launch formulas in secondary cities with relatively low adaptation costs.

Identifying the Right Secondary Cities

Not every secondary city qualifies for the surge thesis. The markets with the strongest fundamentals share several characteristics:

✅ Active MCMV concession zones with expanded eligibility thresholds ✅ Confirmed Novo PAC investment in roads, sanitation, or urban mobility ✅ Zoning reform enabling vertical densification ✅ Population growth above the national average ✅ Existing developer presence signaling validated demand

João Pessoa checks most of these boxes and has been explicitly identified in market research as a key secondary market gaining geographic depth [1]. Other northeastern cities with similar profiles are attracting early-mover developers who recognize that the window for pre-appreciation entry is finite.

Developer Strategies for Secondary Market Entry

For developers considering secondary city expansion, the strategic playbook differs meaningfully from metro launches:

| Strategy Element | Metro Approach | Secondary City Approach |

|---|---|---|

| Land acquisition | Premium corridors | Infrastructure-adjacent parcels |

| Unit mix | Diverse price points | MCMV-concentrated |

| Construction system | Variable | Industrialized preferred |

| Sales timeline | Shorter | Longer pre-sales period |

| Margin profile | Lower but faster | Higher but requires patience |

The supply chain advantage of industrialized building systems is particularly relevant here. Developers who have invested in modular or prefabricated construction can maintain margins even when local labor markets are less developed than in major metros [1]. This is a competitive moat that rewards early investment in construction technology.

For those interested in how successful developers are executing on similar growth markets, the Tramonto development project and Solis development offer concrete examples of how well-positioned projects in growth corridors capture demand ahead of the broader market.

Investors and developers looking to understand the full landscape of available opportunities can explore the complete portfolio of developments to see how leading developers are structuring their secondary and growth-market plays in 2026.

Conclusion: Acting Before the Surge Becomes the Standard

The Secondary Cities Surge 2026: MCMV and Infrastructure Driving Inland Development Beyond São Paulo and Rio is not a speculative thesis — it is a policy-driven, data-supported structural shift in where Brazilian residential real estate value is being created. The combination of MCMV mortgage subsidies adding 2.1% to CAGR forecasts [1], Novo PAC infrastructure unlocking inland land value, and zoning reform enabling vertical densification is creating a rare alignment of demand, supply, and policy support in markets that were previously too small or too underdeveloped to attract institutional attention.

The window for first-mover advantage is real but not unlimited. As rate cuts materialize through 2026 and mortgage affordability improves across all income bands, the secondary cities with established pipelines will see accelerated absorption and price appreciation. The 6–10% price growth already visible in the strongest markets will draw more capital, compress margins, and eventually replicate the saturation dynamics that have made São Paulo’s core less attractive.

Actionable Next Steps for Developers and Investors

- Map MCMV concession zones in the Northeast and São Paulo outskirts to identify markets with the highest subsidy intensity

- Cross-reference with Novo PAC investment schedules to find infrastructure-adjacent land before appreciation is priced in

- Evaluate zoning reform status in target secondary cities to confirm vertical development feasibility

- Prioritize industrialized construction systems to defend margins in markets with less developed local supply chains

- Enter early — secondary city markets reward patience and penalize hesitation once the surge is widely recognized

For developers and investors ready to explore growth-market opportunities, contact the Quadragon team to discuss how Brazil’s secondary city surge is shaping development strategy in 2026 and beyond.

References

[1] Residential Real Estate Market In Brazil – https://www.mordorintelligence.com/industry-reports/residential-real-estate-market-in-brazil