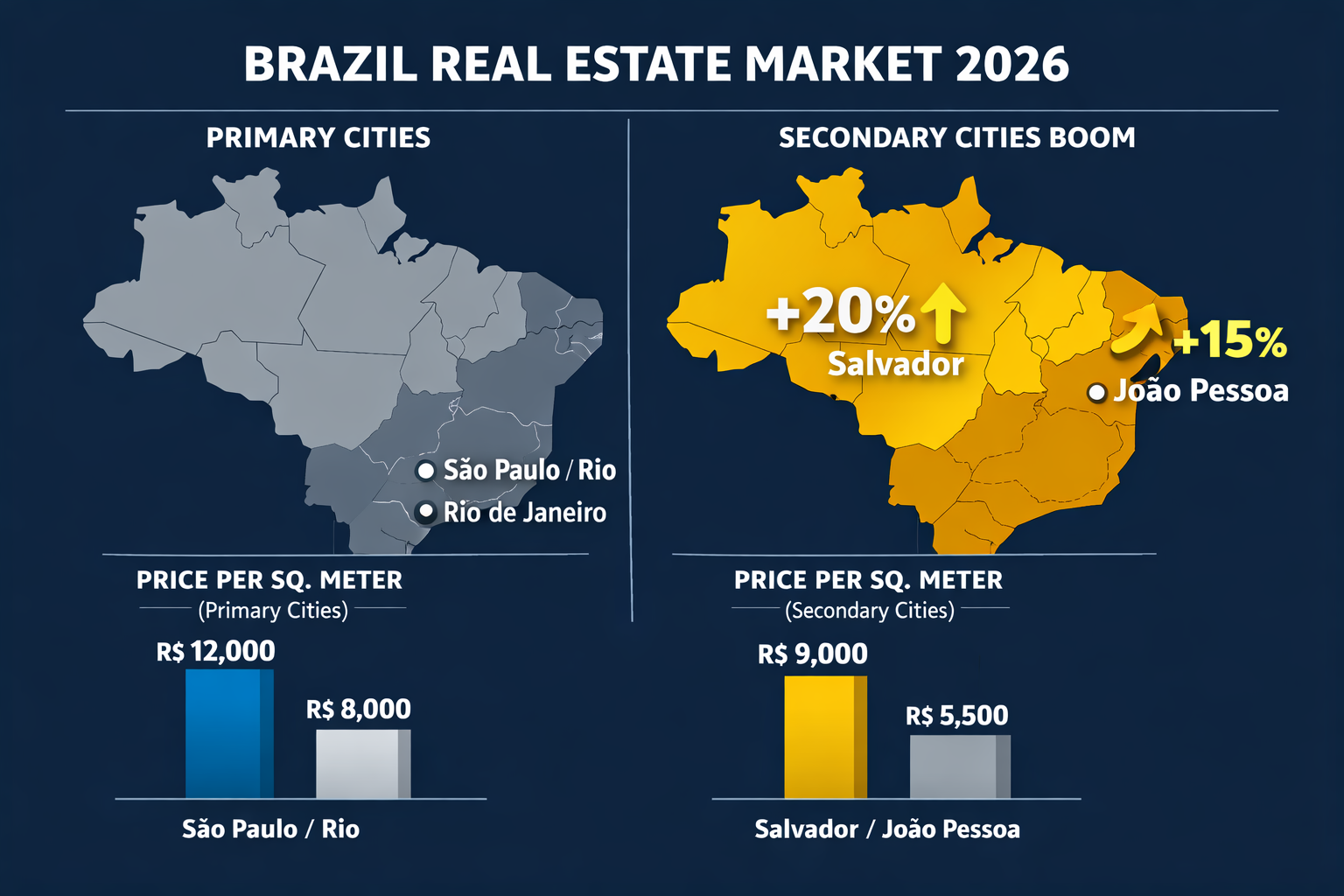

While São Paulo and Rio de Janeiro dominate headlines, Salvador’s residential market posted price growth exceeding 20% in recent periods — a figure that quietly outpaces Brazil’s two most-watched metros and signals a structural shift in where real estate value is being created. The Salvador and João Pessoa price surges 2026: developer entry tactics in secondary city booms story is not a temporary blip. It reflects converging forces: federal subsidy expansion, declining interest rates, zoning reform, and a new generation of affordability-driven buyers who cannot access primary-city markets. Developers who understand how to enter these secondary cities early — and execute correctly — stand to capture outsized returns before competition intensifies.

Brazil’s residential real estate market reached USD 106.97 billion in 2026 and is projected to grow at a 5.33% CAGR to reach USD 138.70 billion by 2031 [1]. Geographic diversification is emerging as one of the most powerful drivers of that growth, and Northeast cities like Salvador and João Pessoa are at its center.

Key Takeaways 📌

- Salvador’s residential prices have surged 20%+, outpacing São Paulo and Rio de Janeiro, driven by affordability migration and infrastructure investment.

- João Pessoa is a designated priority zone for urban zoning reform enabling vertical densification, adding measurable momentum to its construction pipeline [1].

- Minha Casa Minha Vida (MCMV) subsidies are delivering a +2.1% CAGR impact on Brazil’s Northeast real estate market, making small apartments the highest-velocity product segment [1].

- Declining Selic rates are unlocking middle-income buyers previously priced out, expanding the addressable market for developers entering secondary cities [1].

- Joint ventures between regional and national developers — such as the Moura Dubeux/Direcional partnership — are proving the most effective entry model in these markets [3].

Why Secondary Cities Are Outrunning Brazil’s Primary Markets in 2026

The conventional wisdom in Brazilian real estate held that São Paulo and Rio de Janeiro were the only markets worth serious developer attention. That assumption is now costly to maintain.

Salvador, the capital of Bahia and Brazil’s third-largest city by population, has seen residential price appreciation accelerate sharply. Several structural factors explain this:

The Affordability Migration Effect

As São Paulo’s average price per square meter climbs beyond the reach of middle-income households, buyers and renters are actively relocating — or choosing never to move to primary cities in the first place. Salvador and João Pessoa offer dramatically lower entry prices, warmer climates, and improving urban infrastructure. This is not speculative demand; it is real household formation happening in real time.

“The buyers are already there. The question is whether developers arrive before or after the price discovery is complete.”

Novo PAC Infrastructure as a Catalyst

Brazil’s Novo PAC (Programa de Aceleração do Crescimento) has directed significant infrastructure spending toward the Northeast. Improved road networks, sanitation upgrades, and port expansions in Salvador directly increase land values in surrounding neighborhoods. Infrastructure investment has historically been one of the most reliable leading indicators of residential price appreciation — and developers who position land acquisition ahead of project completion capture the full value curve.

For context on how infrastructure spending shapes regional real estate dynamics, the KPMG infrastructure analysis of Brazil highlights the Northeast as a long-term beneficiary of federal capital allocation [2].

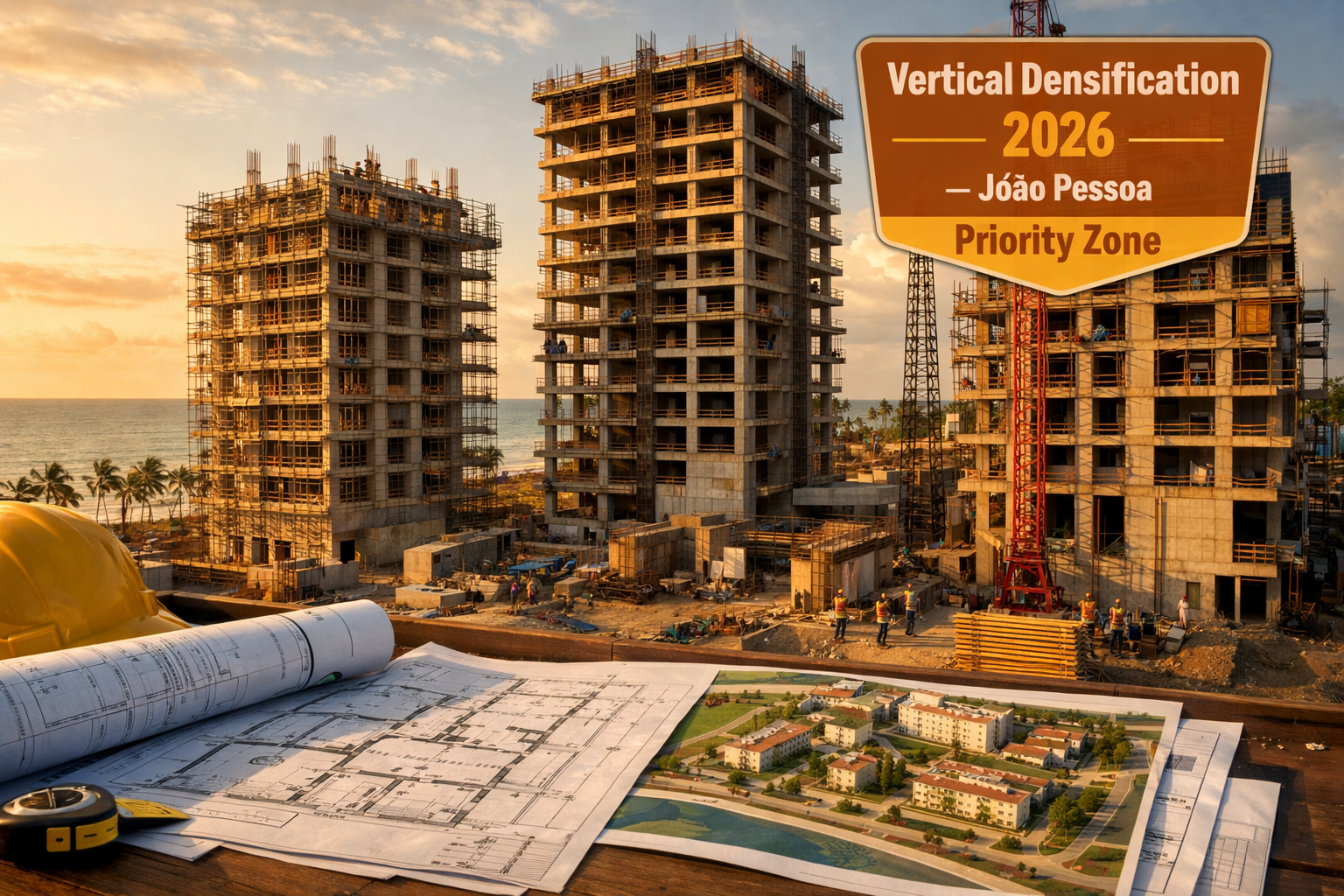

João Pessoa: A Zoning Reform Hotspot

João Pessoa’s vertical densification story is particularly compelling. The city demonstrated significant vertical residential growth by 2024, with households in vertical dwellings reaching notably high levels — a clear signal of active construction activity in a market that was previously dominated by low-rise housing [1].

Critically, urban zoning reform enabling vertical residential densification is contributing +0.9% to market CAGR forecasts, with João Pessoa identified as a priority zone alongside São Paulo’s transit corridors [1]. This regulatory tailwind is not widely priced into land values yet, creating a window for developers to acquire sites at pre-reform prices.

Explore how similar densification dynamics have played out in other Brazilian coastal markets by reviewing best places to invest in Brazil for high returns.

Developer Entry Tactics: What Works in Secondary City Booms

Understanding why Salvador and João Pessoa are surging is only half the equation. The more actionable question is: how should developers structure their entry to maximize returns while managing execution risk?

Tactic 1: Lead with Small-Format, Affordability-Positioned Product 🏢

The demand profile in secondary cities is not for luxury towers. It is for compact, well-designed studios and one-bedroom units that qualify for federal subsidy programs and appeal to first-time buyers and young professionals.

Minha Casa Minha Vida (MCMV) is the dominant demand driver. The program’s accelerated subsidies are delivering a +2.1% CAGR impact on Brazil’s Northeast real estate market over the medium term (2–4 years) [1]. Developers who build product within MCMV income brackets access a buyer pool that is:

- Pre-qualified through federal subsidy mechanisms

- Less sensitive to short-term interest rate fluctuations

- Highly motivated by homeownership as a first purchase

This is not a niche strategy. It is the highest-velocity segment in these markets right now.

| Product Type | MCMV Eligibility | Demand Velocity | Margin Profile |

|---|---|---|---|

| Studio (25–35m²) | ✅ High | Very High | Moderate-High |

| 1-Bedroom (40–55m²) | ✅ High | High | Moderate-High |

| 2-Bedroom (60–75m²) | ✅ Partial | Moderate | Moderate |

| Luxury 3+ Bedroom | ❌ No | Low | Variable |

For developers interested in understanding how compact unit formats perform across different Brazilian coastal markets, the advantages of investing in studios in Florianópolis provides a useful comparative framework.

Tactic 2: Exploit the Selic Rate Window ⏱️

Declining Selic rates are adding a +1.4% CAGR impact to Brazil’s residential real estate market by enhancing mortgage affordability for middle-income buyers who were previously priced out [1]. This is a time-sensitive opportunity.

The mechanism is straightforward: lower benchmark rates reduce mortgage costs, expanding the pool of qualified buyers. For developers in secondary cities, this means:

- Pre-launch sales velocity increases as financing becomes accessible

- Off-plan (na planta) pricing strategies become more effective because buyers can lock in today’s prices with confidence in future financing

- Land acquisition costs remain relatively low before the full impact of rate cuts feeds through to seller expectations

Developers who launch projects in 2026 — while rates are declining but before the full price discovery cycle completes — capture the maximum spread between land cost and sale price. Understanding why buying off-plan can amplify investment returns is essential for communicating value to buyers in these markets.

Tactic 3: Joint Ventures as the Optimal Entry Structure 🤝

Entering an unfamiliar secondary market alone carries significant execution risk. The most successful developers are using joint venture structures to combine local knowledge with national capital and operational scale.

The clearest example: Moura Dubeux Engenharia signed a joint venture partnership with Direcional, combining Moura Dubeux’s deep expertise in Brazil’s Northeast market with Direcional’s specialization in popular-priced housing and construction efficiency [3]. This structure is replicable and represents a template for external developers seeking Northeast exposure.

Key advantages of the JV model in secondary cities:

- ✅ Local partner brings land relationships and permitting knowledge

- ✅ National partner brings capital, construction systems, and sales infrastructure

- ✅ Risk is distributed across the development cycle

- ✅ Local regulatory relationships reduce approval timelines

- ✅ Combined brand credibility supports pre-launch sales velocity

Tactic 4: Prioritize Markets with Strong Land Titling and Permitting Capacity

Not all secondary cities are equally executable. Secondary city execution advantages are concentrating in areas with the strongest land titling, permitting, and service capacity [1]. Salvador and João Pessoa both score relatively well on these metrics compared to smaller Northeast municipalities — which is part of why they are attracting institutional developer attention.

Before committing to land acquisition, developers should conduct:

- Title chain verification — informal land tenure remains a risk in parts of the Northeast

- Municipal permitting timeline assessment — delays of 12–18 months can destroy project economics

- Infrastructure connectivity review — proximity to Novo PAC projects increases both demand and land value

- Utility service capacity confirmation — water, sewage, and electrical capacity constraints affect build costs

For a broader view of how real estate market dynamics are evolving across Brazilian cities, the Quadragon real estate news and insights hub provides ongoing market coverage.

Risk Factors and How to Mitigate Them

No market surge is without risk. Developers entering Salvador and João Pessoa in 2026 should actively manage the following:

🔴 Policy Dependency Risk

MCMV subsidy levels are subject to federal budget decisions. A reduction in program funding would directly impact demand velocity for affordability-positioned product. Mitigation: Design product that remains financeable at market rates even without subsidy, treating MCMV as an accelerant rather than a dependency.

🔴 Construction Cost Inflation

Brazil’s construction input costs have been volatile. Northeast markets may face supply chain constraints for certain materials. Mitigation: Lock in construction contracts early, use standardized building systems, and partner with contractors who have established Northeast supply chains.

🔴 Oversupply in Specific Micro-Markets

Price surges attract competing developers. Certain neighborhoods within Salvador and João Pessoa could see supply concentration. Mitigation: Conduct granular sub-market analysis at the neighborhood level, not just the city level. Focus on areas with demonstrated absorption velocity.

🔴 Digital and Financial Inclusion Gaps

Parts of the Northeast population face barriers to digital financial services that can complicate mortgage origination [4]. Mitigation: Partner with banks and fintechs that have established Northeast distribution and experience with first-time buyer onboarding.

For developers who are also exploring innovative financing structures, cryptocurrency and real estate development as a new investment frontier offers perspective on emerging capital structures.

The Competitive Window: How Long Does It Last?

The Salvador and João Pessoa price surges 2026: developer entry tactics in secondary city booms opportunity is real — but it is not indefinite. Secondary city booms follow a predictable cycle:

- Early discovery phase (current): Price appreciation begins, few institutional developers present, land costs low

- Validation phase (12–24 months out): Major developers announce projects, land prices rise, competition increases

- Saturation phase (36–60 months out): Supply catches up with demand, margins compress, execution quality becomes the differentiator

Salvador and João Pessoa are in Phase 1 transitioning to Phase 2 in 2026. The window for acquiring land at pre-boom prices and launching product before competitive saturation is measured in months, not years.

Developers who have successfully navigated similar regional boom cycles — such as those who entered Florianópolis’s growth corridor early — understand the importance of moving decisively during the discovery phase. The growth of the Ingleses region in Florianópolis illustrates how early-mover advantage compounds over a development cycle.

The UNDP’s 2025 Brazil signals report underscores that Northeast Brazil’s urban development trajectory is being shaped by demographic growth, climate adaptation investment, and federal social program expansion — all of which support sustained residential demand beyond the current surge cycle [5].

Conclusion: Actionable Next Steps for Developers in 2026

The data is unambiguous. Salvador and João Pessoa are delivering price appreciation that outpaces Brazil’s primary markets, supported by federal subsidies, zoning reform, declining rates, and real demographic demand. The Salvador and João Pessoa price surges 2026: developer entry tactics in secondary city booms playbook is clear for developers willing to act with discipline.

Immediate action steps:

- 🗺️ Commission a sub-market land study in both cities, focusing on neighborhoods within 2km of Novo PAC infrastructure projects and public transit nodes.

- 🤝 Identify local JV partners with established permitting relationships and land pipelines in Salvador and João Pessoa.

- 🏢 Design for MCMV eligibility from day one — build studio and one-bedroom product that qualifies for subsidy brackets without sacrificing design quality.

- ⏱️ Move on land acquisition in Q3–Q4 2026 — before the validation phase fully reprices land to reflect the surge.

- 📊 Model scenarios with and without MCMV subsidy to ensure project viability under policy change conditions.

- 🔍 Conduct title and permitting due diligence before any land commitment, using local legal counsel with Northeast expertise [7].

The secondary city boom in Brazil’s Northeast is not speculative. It is structural. Developers who enter with the right product, the right partners, and the right timing will find that Salvador and João Pessoa offer something increasingly rare in Brazilian real estate: genuine first-mover advantage at scale.

To explore current development projects and understand how leading developers are structuring their portfolios in high-growth Brazilian markets, visit the Quadragon developments portfolio.

References

[1] Residential Real Estate Market In Brazil – https://www.mordorintelligence.com/industry-reports/residential-real-estate-market-in-brazil

[2] Infrastructure Opportunities In Brazil – https://assets.kpmg.com/content/dam/kpmg/us/pdf/2017/08/infrastructure-opportunities-in-brazil.pdf

[3] 78f1e2e8 C943 Ceff 9f0b Ed8da2730b42 – https://api.mziq.com/mzfilemanager/v2/d/0b55ea34-4419-4e98-859b-742720701ad7/78f1e2e8-c943-ceff-9f0b-ed8da2730b42?origin=2

[4] Characterizing The Afro Brazilian Digital Inclusion Gap And Assessing Investment Opportunities – https://publications.iadb.org/publications/english/document/Characterizing-the-Afro-Brazilian-Digital-Inclusion-Gap-and-Assessing-Investment-Opportunities.pdf

[5] Undp Brazil Signals Spotlight 2025 En – https://www.undp.org/sites/g/files/zskgke326/files/2026-01/undp_brazil_signals_spotlight_2025_en.pdf

[7] Guide Brazil New – https://www.lexmundi.com/media/hyih2ale/guide_brazil_new.pdf