Brazil’s new sanitation framework has unlocked more than R$ 700 billion in projected private investment — and the neighborhoods that receive coverage first are already seeing formal housing absorption rates climb by double digits. For developers, land buyers, and long-term investors, understanding where concession wins land on the map is no longer optional. It is the primary variable in any credible site-selection model.

This article breaks down exactly how Sanitation Concessions in Brazil: The 2026 Development Playbook for Housing-Linked Growth Corridors connects infrastructure timelines to real estate opportunity — and why timing land acquisition to concession milestones is the single most underrated strategy in the Brazilian property market today.

Key Takeaways 📌

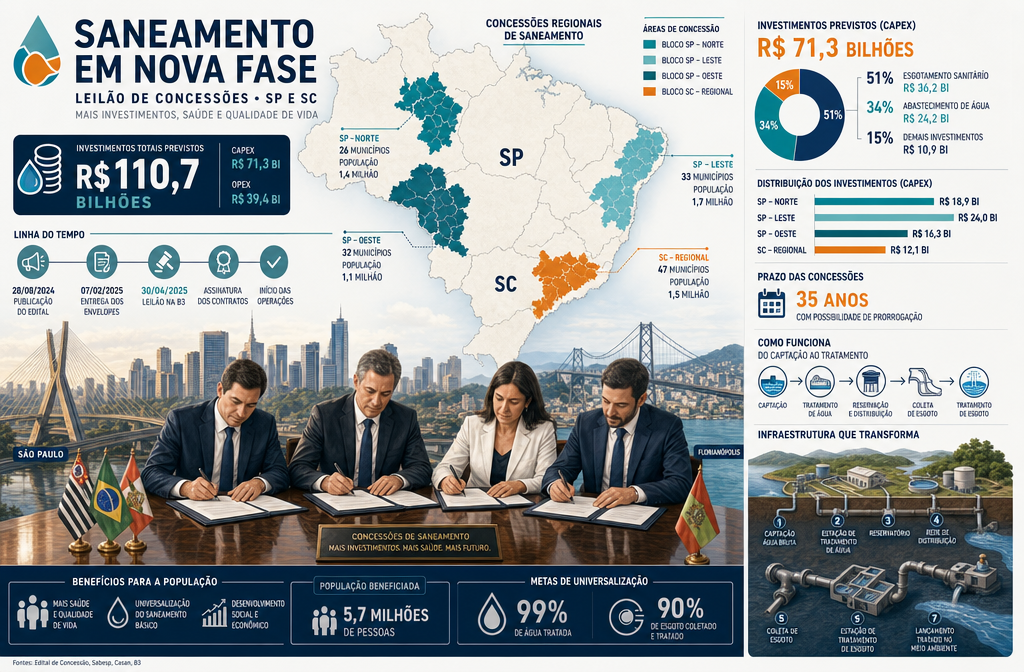

- Brazil’s 2020 Legal Framework for Sanitation (Lei nº 14.026) opened the door to mass privatization of water and sewage services, creating a wave of concession auctions that continues through 2026 and beyond.

- Sanitation coverage directly precedes formal housing growth — areas gaining new sewage and water services see faster regulatory approval, higher land values, and stronger buyer demand.

- Timing land acquisition to concession award dates — not service delivery dates — captures the maximum appreciation window.

- Coastal and mid-sized cities such as those in Santa Catarina are among the highest-leverage markets where infrastructure gaps are closing fastest.

- Investors who align with housing developers already operating in concession corridors reduce execution risk and benefit from institutional-grade due diligence.

Why Sanitation Is the Real Engine Behind Brazilian Real Estate Growth

For decades, Brazil’s housing market operated with a structural ceiling: vast swaths of urban and peri-urban land simply could not support formal residential development because basic water and sewage infrastructure did not exist. According to the National Sanitation Information System (SNIS), as recently as 2022, approximately 35% of Brazilian households lacked access to treated sewage collection. That gap was not a social statistic — it was a hard boundary on where formal real estate markets could function.

The passage of Lei nº 14.026/2020, Brazil’s new legal framework for basic sanitation, changed the calculus entirely. The law:

- Ended the automatic renewal of state-run sanitation contracts

- Required competitive bidding for all new concessions

- Set universal coverage targets for water (99%) and sewage (90%) by 2033

- Opened the sector to private operators with long-term concession contracts (typically 30–35 years)

The result has been a cascade of auctions. Aegea Saneamento, BRK Ambiental, Iguá Saneamento, and international players have competed aggressively for concessions covering millions of connections. Each auction win is, in effect, a government-backed commitment to extend infrastructure into previously underserved areas — and that commitment is what transforms raw land into developable real estate.

💡 Pull Quote: “A concession award is not just a utility contract. It is a zoning event in disguise — one that redraws the map of where housing can legally and economically scale.”

The Concession-to-Coverage Timeline Investors Must Know

Understanding the lag between concession award and actual service delivery is critical for investment timing:

| Phase | Typical Duration | Investor Action |

|---|---|---|

| Concession auction announced | 6–12 months pre-award | Begin land scouting in target zones |

| Concession awarded | Award date | Prioritize land acquisition |

| Initial infrastructure rollout | Years 1–3 post-award | Secure permits, begin pre-sales |

| Full coverage in target zones | Years 3–7 post-award | Scale development, exit or hold |

| Mature market absorption | Years 7+ | Stabilized asset performance |

The award date is the most powerful signal. Land prices in concession corridors typically move within 6–18 months of a public award announcement — well before a single pipe is laid. Developers who wait for operational proof leave significant appreciation on the table.

How Infrastructure Gaps Closing First Creates Neighborhood-Level Opportunity

Not all areas within a concession zone receive coverage simultaneously. Private operators prioritize zones where investment recovery is fastest — typically areas with higher population density, existing partial infrastructure, or proximity to anchor developments. This creates a sequenced rollout pattern that sophisticated investors can map and exploit.

The Three-Zone Framework for Concession Corridors

Zone 1 — Immediate Coverage (Years 1–2): Dense urban cores and established neighborhoods within the concession area. These zones see the least dramatic land value change because formal housing already existed. However, they benefit from service quality improvements that drive rental yield increases and reduce maintenance costs for existing assets.

Zone 2 — Expansion Corridors (Years 2–5): ⭐ This is the highest-leverage zone for housing-linked investment. These are peri-urban areas adjacent to existing coverage, where land is still priced at “unserviced” levels but concession timelines make development viable within a typical construction cycle. Formal housing absorption in these corridors consistently outperforms city averages once coverage is confirmed.

Zone 3 — Greenfield Frontiers (Years 5–10): Outlying areas with the lowest current land costs but the longest wait for service delivery. Suitable for patient capital or land banking strategies, but not for near-term development plays.

Why Formal Housing Markets Respond So Strongly

When sanitation coverage arrives in a neighborhood, several compounding forces activate simultaneously:

- Regulatory unlocking: Municipal governments can issue building permits for formal residential projects. Without sewage infrastructure, permits are often blocked or require costly independent solutions.

- Mortgage eligibility: Brazil’s housing finance system (SFH) and programs like Minha Casa Minha Vida require connection to public sanitation networks for financed purchases. Coverage = buyer pool expansion.

- Land value re-rating: Appraisers and banks re-rate land values upward when serviced status changes, improving LTV ratios for developers.

- Demographic pull: Families actively relocate toward serviced areas, creating organic demand that precedes formal marketing campaigns.

For investors exploring the best places to invest in Brazilian property, understanding which cities are in active concession rollout phases is now a prerequisite for any serious due diligence process.

The 2026 Development Playbook: Applying Sanitation Concessions in Brazil to Real Investment Decisions

Sanitation Concessions in Brazil: The 2026 Development Playbook for Housing-Linked Growth Corridors is not a theoretical framework — it is a practical operating model that leading developers are already executing. Here is how the playbook breaks down across key decision points.

Step 1: Map Active Concession Zones Before Competitors Do

The Brazilian government’s National Sanitation Information System (SNIS) and FUNASA publish concession data, but the most actionable intelligence comes from cross-referencing:

- ANATEL and state regulatory agency (ARSESP, AGERSA, etc.) filings for concession contract terms

- Municipal master plans (Planos Diretores) that identify planned expansion zones

- Developer land bank announcements from publicly listed companies (Cyrela, MRV, Direcional) as leading indicators

Cities in Santa Catarina, for example, have seen accelerated concession activity paired with some of Brazil’s strongest housing demand fundamentals. The real estate market in Greater Florianópolis exemplifies how infrastructure investment and housing demand reinforce each other in a high-growth coastal corridor.

Step 2: Sequence Land Acquisition to Concession Milestones

The optimal acquisition window is between concession announcement and first-year operational milestones. This window typically offers:

- ✅ Confirmed infrastructure commitment (reducing execution risk)

- ✅ Land still priced at pre-service levels (capturing appreciation upside)

- ✅ Sufficient lead time to complete permitting before coverage arrives

Acquiring after service delivery is confirmed captures less upside and competes with a broader buyer pool. Acquiring before announcement is highest-risk unless proprietary intelligence on concession pipeline is available.

Step 3: Align Product Type to Absorption Dynamics

Different housing products perform differently in concession corridor timelines:

| Product Type | Best Zone | Key Driver |

|---|---|---|

| Affordable housing (Minha Casa Minha Vida) | Zone 2 | Mortgage eligibility unlocked by coverage |

| Mid-market condominiums | Zone 1–2 boundary | Quality upgrade demand from existing residents |

| Studios and compact units | Zone 1 urban core | Rental yield improvement from service quality |

| Greenfield master-planned communities | Zone 2–3 boundary | Long-term land appreciation + first-mover positioning |

Developers building in areas where sanitation is being actively extended — such as those investing in studios in Florianópolis — are already benefiting from the convergence of infrastructure improvement and strong rental demand in coastal urban markets.

Step 4: Use Pre-Sales Timing as a Risk Management Tool

One of the most powerful tools in the playbook is launching pre-sales after concession award but before full coverage delivery. This approach:

- Captures buyer enthusiasm driven by confirmed infrastructure commitment

- Allows developers to maximize gains from off-plan purchases by pricing ahead of the service delivery curve

- Reduces carrying costs by funding construction through pre-sale deposits

Buyers who purchase in this window — between concession award and service delivery — historically capture the strongest appreciation relative to entry price.

Step 5: Monitor Execution Progress Through Construction Milestones

Infrastructure concessions and housing development share a common risk: execution delays. Savvy investors track both the concession operator’s rollout milestones and the developer’s construction progress as parallel indicators of value realization.

Projects like Tramonto in the Florianópolis region demonstrate how accelerated construction timelines — with foundations completed ahead of schedule — signal developer execution quality that compounds the infrastructure-driven appreciation thesis.

Regional Focus: Why Coastal Mid-Sized Cities Are the Highest-Leverage Plays in 2026

Brazil’s largest metros — São Paulo, Rio de Janeiro, Belo Horizonte — have mature sanitation infrastructure and correspondingly mature (read: expensive) real estate markets. The highest-leverage opportunities in Sanitation Concessions in Brazil: The 2026 Development Playbook for Housing-Linked Growth Corridors are concentrated in coastal mid-sized cities where three conditions converge:

- Active concession rollout closing infrastructure gaps in expansion corridors

- Strong organic housing demand driven by migration, tourism, and remote work trends

- Land prices still at pre-infrastructure levels in key zones

Santa Catarina’s coastal cities — particularly in the greater Florianópolis metropolitan area — check all three boxes. The growth of the Ingleses region in Florianópolis illustrates how infrastructure investment, quality-of-life improvements, and property appreciation reinforce each other in a high-demand coastal corridor.

Key Metrics to Watch in 2026

- Concession coverage expansion rate: How many new connections per year is the operator committing to in the contract?

- Municipal permit issuance trends: Rising permit volumes in previously restricted zones confirm coverage is enabling development.

- Formal housing absorption rates: Track units sold vs. launched in concession corridors vs. city average.

- Land price differential: Compare serviced vs. unserviced land prices within the same municipality to identify compression opportunities.

Risk Factors and How to Mitigate Them

No investment playbook is complete without an honest assessment of risks:

⚠️ Concession operator default or renegotiation: Private operators have occasionally sought contract renegotiations when investment requirements proved more costly than modeled. Mitigation: Focus on concessions won by well-capitalized operators with proven track records.

⚠️ Rollout delays: Infrastructure construction faces the same delays as any large civil works program. Mitigation: Build buffer into development timelines; do not plan pre-sales launches contingent on specific infrastructure delivery dates.

⚠️ Regulatory changes: Brazil’s regulatory environment can shift with political cycles. Mitigation: Prioritize municipalities with strong independent regulatory agencies and stable municipal governance.

⚠️ Demand misreading: Not all areas receiving sanitation coverage will see equivalent housing demand. Mitigation: Validate demand fundamentals (employment, migration trends, income levels) independently of infrastructure thesis.

For investors tracking the latest developments in Brazilian real estate markets, staying current through reliable market news and analysis is essential for adjusting strategy as concession rollouts evolve.

Conclusion: Actionable Next Steps for 2026

The convergence of Brazil’s sanitation privatization wave and its structural housing deficit creates one of the most compelling infrastructure-linked real estate opportunities in the emerging market universe. The playbook is clear:

✅ Action 1: Build a concession monitoring system. Track SNIS data, state regulatory filings, and operator press releases to identify which municipalities are in active rollout phases.

✅ Action 2: Prioritize Zone 2 acquisition targets — peri-urban expansion corridors where land is still priced below post-service levels but concession timelines are confirmed.

✅ Action 3: Align with developers who are already operating in concession corridors and have demonstrated execution quality. Their land banks and pre-sales pipelines are the fastest path to exposure.

✅ Action 4: Use the concession award date — not service delivery — as your primary acquisition trigger. The appreciation window opens at award and narrows as coverage approaches.

✅ Action 5: Diversify across product types and zones within a single concession corridor to balance near-term yield with long-term appreciation.

Brazil’s sanitation transformation is not a background story. It is the primary driver reshaping which neighborhoods become viable housing markets in 2026 and beyond. Investors who treat concession maps as investment maps will be the ones capturing the outsized returns that this infrastructure cycle is generating.